KUALA LUMPUR (March 7): Bermaz Auto Bhd (KL:BAUTO), which mainly assembles Mazda-branded vehicles, is expected to see a further decline in earnings over the coming quarters as it continues to lose market share to mounting competition from Chinese carmakers, according to BIMB Research.

The car distributor continues to see Mazda’s total vehicle sales fall 24% year-to-date in 2024 to 14,537 units, down from 19,124 units in 2023. In contrast, Chinese automaker Chery has rapidly expanded its market presence, selling 19,683 units within the same period, after entering the Malaysian market in July 2023 with 4,500 units sold in the second half of that year, BIMB Research noted in a report on Friday.

“Chery’s success, driven by superior powertrain offerings and competitive design within the same segment, accelerated the shift in consumer preference towards value-driven alternatives,” the research house said.

The Mazda CX-5, the brand’s best selling model in Malaysia, is priced between RM145,000 and RM195,000, slightly above the top-selling models from new entrants such as Chery and BYD. The price difference has contributed to Mazda’s declining competitiveness in the mass-market segment.

Given the weaker sales outlook, BIMB Research has slashed its earnings projections for Bermaz Auto by 20% for FY2025, 27% for FY2026, and 25% for FY2027, reflecting a more conservative revenue assumption, driven by an anticipated drop in sales volume.

“We anticipate the company to announce a lower dividend. On an annual basis, we estimate Bermaz Auto to pay a DPS (dividend per share) of nine sen in FY2026, which implies a dividend yield of 8% and a payout ratio of 72%,” it added.

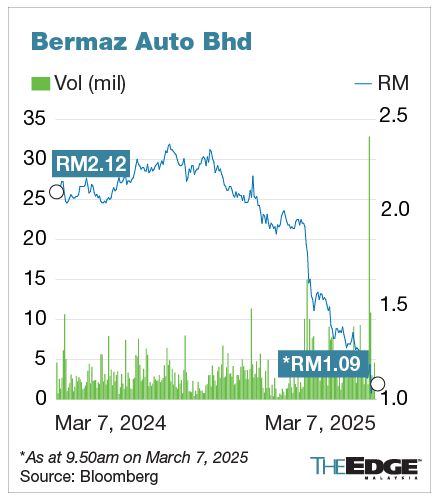

Shares of Bermaz Auto have plunged more than 30% since December, as investor sentiment remains cautious amid heightened competition. Several research houses have turned less optimistic on the stock, revising their target prices downward in recent weeks.

At the time of writing on Friday, Bermaz Auto’s shares were down one sen or 0.91% at RM1.09, giving the company a market capitalisation of RM1.28 billion.

Currently, the stock has eight “buy” calls, six “hold” calls, and one “sell” call among analysts. The consensus target price has dropped more than 25% since early December last year to RM1.89, according to Bloomberg data.

Still, BIMB Research believes Bermaz Auto’s multi-brand strategy, strong balance sheet, and transition towards electric vehicles, position it for sustainable growth in the long run.

For now, the research house maintains its “hold” rating on Bermaz Auto, with a target price of RM1.12. The stock is currently trading at a price-to-earnings (PE) ratio of 4.7 times — lower than peers such as MBM Resources Bhd (KL:MBMR) at 6.5 times, and Sime Darby Bhd (KL:SIME) at 9.5 times, based on AskEdge data.

- Malaysia secures zero-import duties with four-nation European bloc amid trade uncertainties

- Police seize over RM3.17b in assets, arrest eight linked to MBI Ponzi scheme

- Paramount's 70%-owned unit and 2 others sued over Taman U-Thant land deal

- China raises tariffs on US to 125%, says won’t go higher

- Google lays off hundreds of employees in Android, Pixel teams — report

- Janus Henderson fund manager says investors should cut exposure to stocks as recession looms

- Lagarde tells finance chiefs to let EU take lead on trade talks

- Dimon predicts Treasury market ‘kerfuffle’ where Fed steps in

- Wan Rosdy appointed National Entrepreneur and MSME Development Council Special Advisor

- Volvo Cars may take up to two years to expand US production to avoid tariffs, CEO tells daily DN