This article first appeared in Capital, The Edge Malaysia Weekly on March 3, 2025 - March 9, 2025

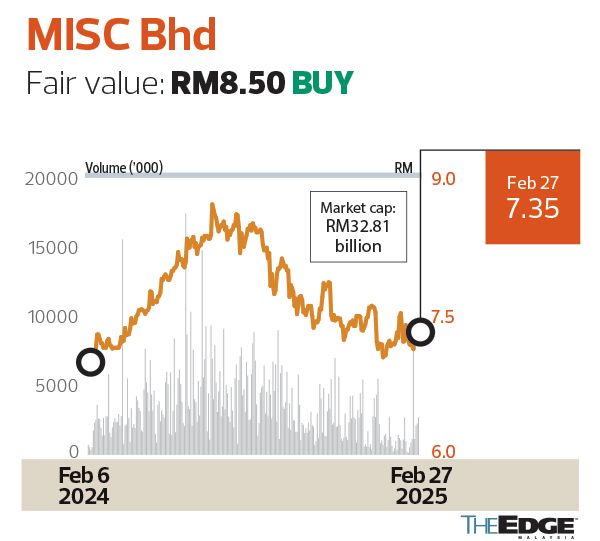

MISC Bhd

Fair value: RM8.50 BUY

AMINVESTMENT BANK RESEARCH (FEB 24): We maintain our “buy” call on MISC Bhd (KL:MISC). The group’s full-year FY24 core net profit (CNP) was slightly below our forecast but was within the street’s estimates. Though we acknowledge challenges in the gas segment over the next two years, we believe earnings have bottomed out. We see MISC as a key beneficiary of the upcoming floating, production, storage and offloading (FPSO) tender cycle and it is also primed for potential value unlocking opportunities after hitting first oil for the Marechal Duque du Caxias (MDdC) FPSO.

In line with management’s guidance of a soft outlook for the gas segment, we cut our earnings forecasts for FY25 and FY26 by 8% and 10% respectively. Hence, we lower our target price from RM8.80 to RM8.50, which implies a 2026 enterprise value over Ebitda of 11 times or at par to its 10-year average. The group reported a full year FY24 CNP of RM2.178 billion (-5% y-o-y) which came in within consensus expectations but was slightly below our forecast at -6.3%.

Management continues to guide for a continually soft outlook for the gas segment until 2026 due to the continued influx of new vessels and delays in the delivery of new LNG liquefaction capacity. For reference, term and spot rates for LNG carriers saw a further decline in December 2024 of up to 15% for the 160,000 and 179,000 cubic metre (CBM) segments and 40% for the 145,000 CBM segment — reaching a new low since 2023. As such, we model our assumptions for the same based on an average growth rate of nil/5%/15% for FY25/FY26/FY27 respectively. Notably, we expect to see a significant pick-up post-FY26 in demand (and correspondingly, charter rates), assuming management’s forecast of 12% CAGR for liquefaction capacity globally between 2024 and 2029 holds.

MISC updated that it is currently undertaking a detailed feasibility study on the potential share-based merger with Bumi Armada Bhd (KL:ARMADA). We see MISC as a potential beneficiary for the incoming tender cycle, particularly in Malaysia, owing to the recent delivery of the Mero 3 FPSO and the relationship with Petroliam Nasional Bhd. We believe the group will be able to cater to at least one new conversion award or two to three redeployments, which will carry an estimated capex of up to US$2 billion to US$2.5 billion collectively.

Skyworld Development Bhd

Target price: RM1.10 BUY

PHILIP CAPITAL (FEB 24): Skyworld Development Bhd’s (KL:SKYWLD) 9MFY25 revenue and core net profit declined 38% and 62% y-o-y, respectively. The weaker results were mainly attributable to a lower number of ongoing projects, coupled with delays in planned launches, including Sky Amanyi, Cheras (circa RM600 million gross development value), due to additional geotechnical evaluations. Overall, 9MFY25 came in below expectations at 64% of our previous FY25 estimates and 58% of the street’s forecasts. The variance to our forecast was due to delays in new launches and a higher effective tax rate.

We expect sequentially stronger 4QFY25 earnings, driven by higher progress billings from ongoing projects, coupled with the final milestone billings from the completion of EdgeWood and SkyVogue.

We trim our FY25/26 earnings by 13%-25% to account for the delayed launch for SkyAmanyi and higher effective tax rate. We raise our FY27 earnings forecast by 1% after incorporating a better progress recognition for SkyAmanyi. We maintain our revised net asset value-derived target price and “buy” call, as we continue to like SkyWorld’s robust project pipelines, driven by its recent RM13 billion venture into Penang’s affordable housing segment.

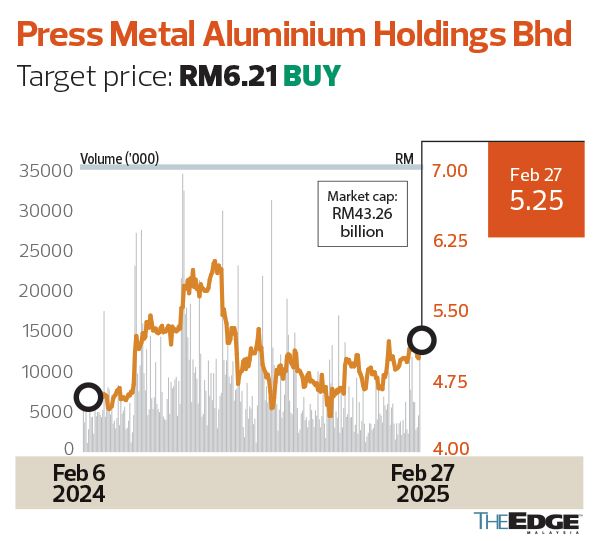

Press Metal Aluminium Holdings Bhd

Target price: RM6.21 BUY

HONG LEONG INVESTMENT BANK RESEARCH (FEB 27): Press Metal Aluminium Holdings Bhd (KL:PMETAL) recorded 4Q24 core earnings of RM445.7 million (+8% q-o-q, +36% y-o-y), lifting FY24’s sum to RM1.789 billion (+44% y-o-y). The results were within our (102%) and consensus (103%) expectations.

Following a record year in FY24, we expect the group to register further earnings growth in FY25 on the back of easing alumina prices moving into 2025 and increased PT Bintan’s alumina capacity of 1mtpa from mid-2025. Bloomberg Intelligence forecasts alumina price to drop to circa US$490-US$500 per tonne in FY25 due to capacity recovery from Gladstone refinery and imminent bauxite export resumption from the Guinea and Juruti region of Brazil, coupled with accelerating alumina output growth from China, India and Indonesia.

Meanwhile, PT Bintan’s associate contribution should remain elevated in the coming years as its alumina production capacity of 2mtpa is slated to grow by 1mtpa in mid-2025 and another 1mtpa in 2H26, tentatively, which we have not imputed into our forecasts pending clearer guidance from management on the commissioning timeline. We maintain our “buy” call and target price on the stock, based on -0.5 standard deviation of its five-year historical mean PER of 25 times on FY25 forecast earnings.

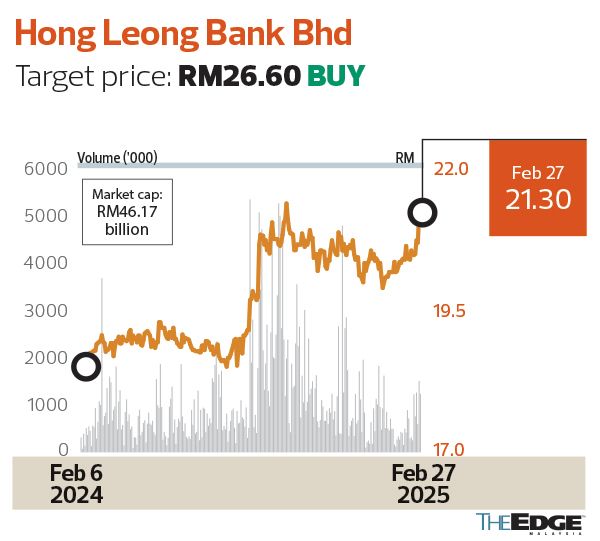

Hong Leong Bank Bhd

Target price: RM26.60 BUY

RHB RESEARCH (FEB 27): Hong Leong Bank Bhd’s (HLBB) (KL:HLBANK) 1HFY25 results were in line with expectations. The home operations once again put up a strong showing, further reducing the group’s reliance on associate Bank of Chengdu. Management appears to be keen on accelerating dividend payouts — though incremental yields (+0.1-0.4 percentage points) are not substantial, this now adds a capital management dimension to our thesis on the counter, that is, solid fundamentals and attractive valuations.

Net profit for 2QFY25 of RM1.15 billion (+5% y-o-y, +5% q-o-q) brought the 1HFY25 figure to RM2.24 billion (+6% y-o-y), forming 51% and 50% of our and the street’s full-year forecasts respectively.

HLBB anticipates a 50bp uplift to capital ratios from the full implementation of new Basel regulations — this would raise the CET-1 ratio to the mid-13% level. As such, management appeared more optimistic on dividends and said it could lift its payout ratios to 40% as soon as FY27.

Commensurate with that, the group’s 1HFY25 interim DPS of 28 sen (1HFY 24:25 sen) implied a slight y-o-y payout expansion to 26% from 24%. We raised DPS estimates to roughly match the new guidance. Our target price remains the same.

Save by subscribing to us for your print and/or digital copy.

P/S: The Edge is also available on Apple's App Store and Android's Google Play.

- Mr DIY founder Tan Yu Yeh relinquishes vice chairman post, to serve as adviser

- 50,000 Malaysian jobs at risk, business chamber warns as it calls for urgent US tariff mitigation council

- Malaysia refutes 47% US import tariff claim, takes measures to prioritise well-being of businesses and people

- Trump hits China tariff retaliation, says policy will remain

- China retaliation on US farm goods hits soybeans, bolstering Brazil

- ‘Worst-case scenario’ for tech wipes $1.4 trillion from Nasdaq

- Anwar says impact of latest US tariff on nation's economy still being assessed

- Tok Mat, Rubio discuss bilateral relations, Asean-US Special Summit date

- US solar’s hoarding habit will help blunt sting from Trump tariffs

- Wall Street rout drags Nasdaq near bear market