This article first appeared in Capital, The Edge Malaysia Weekly on March 3, 2025 - March 9, 2025

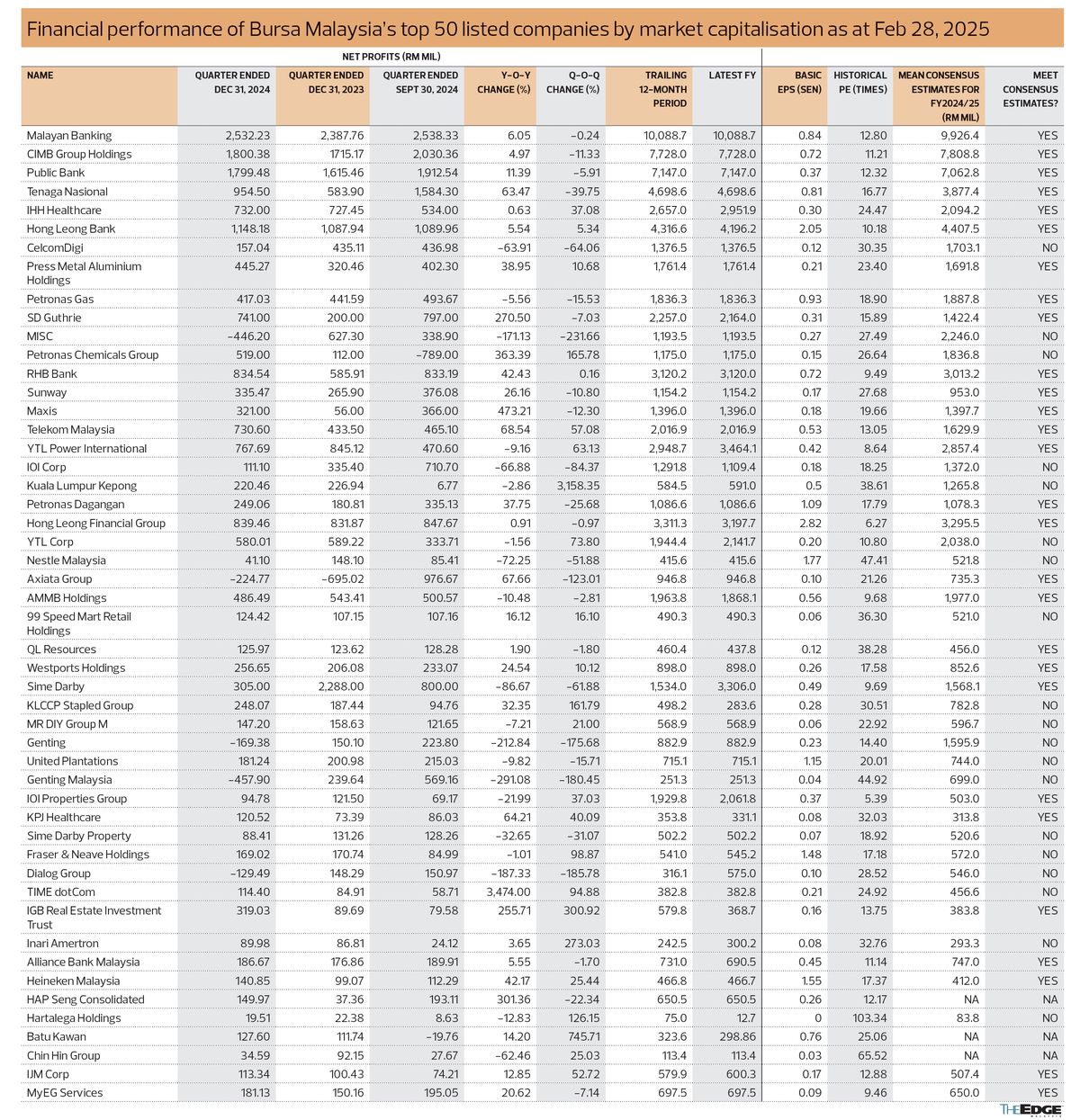

THE financial results of companies listed on the Main Market of Bursa Malaysia for the quarter ended Dec 31, 2024 (4Q2024), were largely underwhelming, as more companies underperformed analysts’ expectations than those that outperformed.

As such, there could be some downside risks to market earnings and analysts’ forecasts for the benchmark index FTSE Bursa Malaysia KLCI’s year-end targets.

“Based on stocks we tracked, the results are underwhelming, with the ratio of underperformers at 30% against outperformers at 18%, with the rest in line with expectations,” says Ivy Ng Lee Fang, head of Malaysia research at CIMB Securities Sdn Bhd.

Ng’s overview is shared by Vincent Khoo, managing director, strategy, at UOB Kay Hian, who says there was a fairly wide range of disappointments in the recently concluded results season.

Other analysts and heads of research say, however, that the results were generally within their expectations. Nevertheless, the definition of “within expectations” could differ from one research house to another.

“The 4Q2024 results season comes with the expectation that some of the forex and logistics cost-related pressures would ebb. Pressures are not fully passed through in areas such as consumer, although there were green shoots of improvement, especially for export sales.

“From a broader perspective, large KLCI index component sectors such as banks, planters and telecommunication companies have generally met or exceeded expectations,” says Peter Kong, head of research at Kenanga Investment Bank Bhd.

Based on an analysis of the performance of the top 50 companies ranked by market capitalisation, 32 companies managed to meet analysts’ consensus expectations of annual net profit for their respective current financial years of either FY2024 or FY2025.

(For companies whose financial year end falls on a date other than Dec 31, their net profits are assessed on a trailing 12-month basis.)

Banks and plantations largely outperformed

All the banks and financial institutions in the top 50 market capitalisation ranks met consensus expectations for their latest quarterly and annualised net profit.

Affin Bank Bhd (KL:AFFIN) leads the pack, with its net profit of RM509.7 million for FY2024 being 108.3% of consensus estimates.

“Banks and plantations have a higher ratio of companies that outperformed during the quarter so far. For plantations, it is a case of strong crude palm oil (CPO) and palm kernel (PK) prices in 4Q.

“For banks, the outperformance came from better-than-expected non-interest income and low loan loss provision. We also noted higher than expected dividends from players in these two sectors,” says Ng of CIMB Research.

Giants Malayan Banking Bhd (KL:MAYBANK) and Public Bank Bhd (KL:PBBANK) both managed to exceed analysts’ estimates for their respective FY2024 net profit, with the former achieving a net profit that is 1.6% higher than consensus expectations.

“Maybank’s FY2024 net earnings of RM10.1 billion made up 103% of our forecast and 102% of consensus estimates,” says Kenanga Research in a report following the bank’s results announcement.

The research firm highlights, however, that the largest bank in Malaysia fell short in its non-domestic portfolio, resulting in a loan growth of 5.3% year on year (y-o-y) to RM674.97 billion, compared with its target of between 7% and 8%.

However, its Malaysian loan book, which grew 8.2%, still outperformed the industry’s 5.5%, Kenanga Research adds.

Maybank had introduced a more conservative loan growth target of between 5% and 6% y-o-y for the current FY ending Dec 31, 2025. This is a result of a pivot by the group towards more margin retention initiatives, a strategy that Kenanga Research notes other banks have already deployed.

“That said, we believe the group would still be able to outpace its competitors on the domestic front, thanks to its stronger brand equity and scale to deploy more wholesale funding where needed.”

The research firm has an “outperform” call on Maybank with a target price (TP) of RM12 per share.

Meanwhile, Hong Leong Bank Bhd’s (KL:HLBANK) trailing 12-month net profit of RM4.32 billion is 97.9% of analysts’ estimates for its FY ending June 30, 2025. In the FY ended June 30, 2024, it posted a net profit of RM4.2 billion. Its IHFY2025 earnings made up 50.8% of consensus estimates.

RHB Research says the group’s net profit of RM2.24 billion for the 6MFY2025 period ended Dec 31, 2024, was in line with its expectations, as home operations once again gave a strong showing, further reducing Hong Leong Bank’s reliance on associate Bank of Chengdu.

RHB Research notes that Hong Leong Bank’s management is keen on accelerating dividend payouts now, which adds a capital management dimension to its thesis on the counter — solid fundamentals and attractive valuations.

“Our TP is kept at RM26.60 and is based on an unchanged Gordon growth model (GGM)-derived price-to-book value of 1.3 times, just under the long-term mean P/BV. The sole change to our GGM model was to book value per share, where we now assume a lower CY2025F figure of RM20.05 (from RM20.09) in line with our raised dividend per share estimates.

“At circa 1 time P/BV (near -1.5SD or standard deviation from the long-term mean), Hong Leong Bank looks supremely undervalued especially when compared to its forward return on equities of 11% to 12%,” note the RHB Research analysts.

Among the planters, SD Guthrie Bhd (KL:SDG) and Genting Plantations Bhd (KL:GENP) exceeded analysts’ expectations in FY2024. The former’s net profit of RM2.16 billion for FY2024 was 152.4% of consensus estimates.

Meanwhile, Genting Plantations’ FY2024 net profit of RM323.1 million was 13.9% higher than consensus estimates.

“[SD Guthrie’s] 4Q2024 core net profit of RM510 million (+45% q-o-q; +141.7% y-o-y) took FY2024’s sum to RM1.49 billion (+49% y-o-y).

“The results exceeded our expectations, accounting for 113.5% of our estimate, primarily due to higher-than-expected realised palm product prices and performance at the downstream segment, and lower-than-expected finance cost,” Hong Leong Investment Bank Research says in a note.

Genting Plantations also ended its FY2024 strongly with a headline net profit of RM112 million, which was 77% higher y-o-y, despite a few one-off costs, namely impairment losses on plasma receivables and biodiesel plant, as well as unrealised forex losses.

However, IOI Corp Bhd (KL:IOI) had a disappointing second quarter ended Dec 31, 2024 (2QFY2025), as its headline net profit fell 67% y-o-y to RM111 million, due to unrealised forex losses on foreign currency debt and fair value loss on derivative financial instruments (FI).

“Adjusted for forex loss, 2QFY2025 core net profit of RM301 million (-3% y-o-y, -9% q-o-q) brought 1HFY2025 to RM633 million (+6% y-o-y), which met 48%/49% of our/consensus full-year estimates,” says Maybank Investment Bank (IB) Research on Feb 25.

Apart from the forex losses, IOI Corp’s downstream business also suffered, as it went into the red in the latest quarter, posting a loss before interest and tax of RM89 million, hurt by fair value loss on derivative financial instruments.

“Within this division, we understand the oleo subsegment’s 2Q earnings contribution mitigated the weaker refinery subsegment. Positively, its downstream associates recorded a higher y-o-y contribution of RM28 million (+48% y-o-y, -48% q-o-q) in 2QFY2025,” states Maybank IB Research.

Technology, oil and gas disappoint

As seen with IOI Corp, many companies were affected by the sudden collapse of the US dollar in the final quarter of 2024, which resulted in substantial forex losses, especially for companies in the technology sector.

“Rubber gloves, technology, consumer and oil and gas players posted weaker than expected results. This is due to weaker than expected sales due to competition and softer global demand,” says CIMB Research’s Ng.

Inari Amertron Bhd (KL:INARI) saw its net profit for the second quarter ended Dec 31, 2024 (2QFY2025), contracting by 34.4% y-o-y to RM61.6 million, as its profitability was impacted by a lower volume loading of products.

However, AmInvestment Bank notes in a Feb 24 report that the weak results in the first half were also due to the stronger ringgit, alongside soft demand for Inari’s products. Its 1HFY2025 net profit came in 23.5% lower y-o-y at RM131 million.

During the period, Inari’s unrealised forex losses stood at RM19.06 million, while its realised forex losses were RM5.8 million.

For oil and gas players, Petronas Chemicals Group Bhd (KL:PCHEM) and Dialog Group Bhd (KL:DIALOG) disappointed.

Petronas Chemicals recorded a core net loss of RM209.7 million in the fourth quarter ended Dec 31, 2024, bringing its FY2024 core earnings to RM1.18 billion, which was 34% lower y-o-y. The results were well below the mean consensus estimates of RM1.84 billion.

Meanwhile, Dialog reported a core net profit of RM23 million in the second quarter ended Dec 31, 2024, after excluding a RM91 million property, plant and equipment write-off for its malic acid plant in Gebeng, Kuantan, Pahang, and an impairment of investment for the food-grade recycled polyethylene terephthalate pellets (rPET) plant in Pajam, Negeri Sembilan, of RM44 million, as well as unrealised forex losses.

The results represented only 28% to 29% of AmInvestment’s and consensus forecasts due to losses from the engineering, procurement, construction and commissioning (EPCC) segment, resulting from higher costs during the commissioning stages and lower demand from the rPET venture.

“The group reported 2QFY2025 headline losses as management embarked on a kitchen sinking exercise. However, after accounting for impairments, core earnings were still a miss due to the EPCC and renewables business,” says AmInvestment Bank in a Feb 14 note.

However, the research firm is still positive on Dialog. The kitchen sinking exercise is deemed as timely, particularly with regard to the discontinuation of the malic acid plant, as spot prices had declined by 20% to 30% due to an oversupply situation in the region.

“In the near term, we expect to see positive news flows to support share price performance from the following commencement of operations from: (a) expansion of Morimatsu-Dialog fabrication facilities and 24,000 cu m renewable fuel tanks in Tanjung Langsat by 3QFY2025; and (b) new award for a biorefinery tank terminal in Pengerang,” the research firm notes.

While results in the quarter ended Dec 31, 2024 were largely underwhelming, higher than expected dividends and dividend commitments, especially from the banks and planters could mean that investors are likely to gravitate more towards blue-chip names or sector leaders, notwithstanding potentially higher valuations, says Kong of Kenanga Research.

“However, outside of the blue-chip stocks and sector leaders, there has not been material changes in outlook guidance for those companies that are seen as data centre or AI (artificial intelligence) beneficiaries either, although investors will still be watchful on policies from the US,” he says.

Save by subscribing to us for your print and/or digital copy.

P/S: The Edge is also available on Apple's App Store and Android's Google Play.

- China suppliers mock tariffs with Nike, Lululemon deals on TikTok

- Yellen says sell-off in Treasuries shows US confidence loss, not dysfunction

- Reach Energy, Cahaya Mata, Able Global, Pestec, Bina Puri, Jentayu Sustainables

- Malaysia declares state funeral for Tun Abdullah Ahmad Badawi

- Nvidia to produce AI servers worth up to US$500b in US over four years

- Tariff shock awaits China after trade surplus hits $103 billion

- US steps up probes into pharmaceutical, chip imports, setting stage for tariffs

- Trump again accuses Zelenskiy of starting war as talks grind on

- Asian stocks set for cautious day as US trade probes sow more anxiety

- South Korea unveils US$23 billion support package for chips amid US tariff uncertainty