Hong Kong Finance Secretary Paul Chan.

(Feb 26): The Hong Kong government will shrink its workforce and accelerate a plan for economic integration with China, as the city seeks new growth drivers to combat geopolitical uncertainty and a property downturn.

Financial Secretary Paul Chan on Wednesday laid out a blueprint to trim regular spending, including by cutting 10,000 civil servant jobs and freezing government workers’ pay. But he vowed to boost support for the Northern Metropolis, a mega infrastructure project aiming to create a cross-border tech hub.

“Strictly containing public expenditure is a must,” Chan said in his annual budget speech, citing external headwinds to trade and investment. The reduction of the civil service, to be carried out over two years, is equivalent to more than 5% of the current 173,000 employees.

Policymakers are trying to balance the government’s books while finding ways to buffer the economy against the fallout from President Donald Trump’s trade war and elevated interest rates.

In a boost to the sluggish real estate market, Chan lowered the stamp duty for more cheap homes, to cover those valued up to HK$4 million (US$514,740 or RM2.3 million). The previous ceiling was HK$3 million.

The announcement boosted shares of developers, with those of China Overseas Land & Investment gaining as much as 8.4% and Sun Hung Kai Properties up as much as 3.1%. The Hang Seng Index rose as much as 4.1% to a three-year high.

Chan also pledged to invest HK$1 billion in an AI research center to drive innovation, and to set up a HK$10 billion fund to invest in emerging industries. The sums pale in comparison with global efforts elsewhere, showing fiscal pressures are limiting the government’s options.

“The budget shows there is no short term fix to Hong Kong’s economic issues and its budget deficit and thus it is hunkering down,” said Gary Tan, a portfolio manager at Allspring Global Investments.

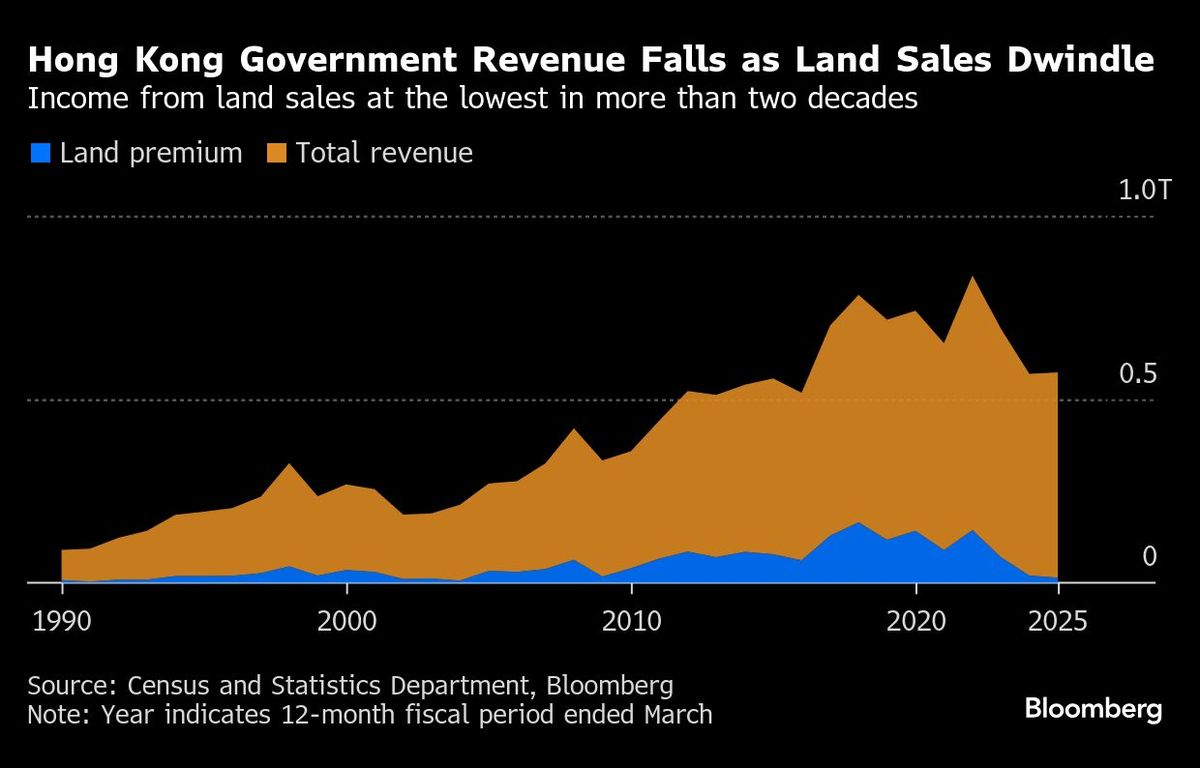

The government will seek to cut regular spending by 7% over the next three years, as falling land sales continue to hurt a key source of tax revenue. Revenue from land premium — the money developers pay to use land — is estimated to fall to HK$13.5 billion for the current fiscal year, the lowest in more than two decades.

The declined income drove Hong Kong’s budget into the red for a third year, with the deficit for the 12 months ending March expected to reach US$87.2 billion, much more than original estimates.

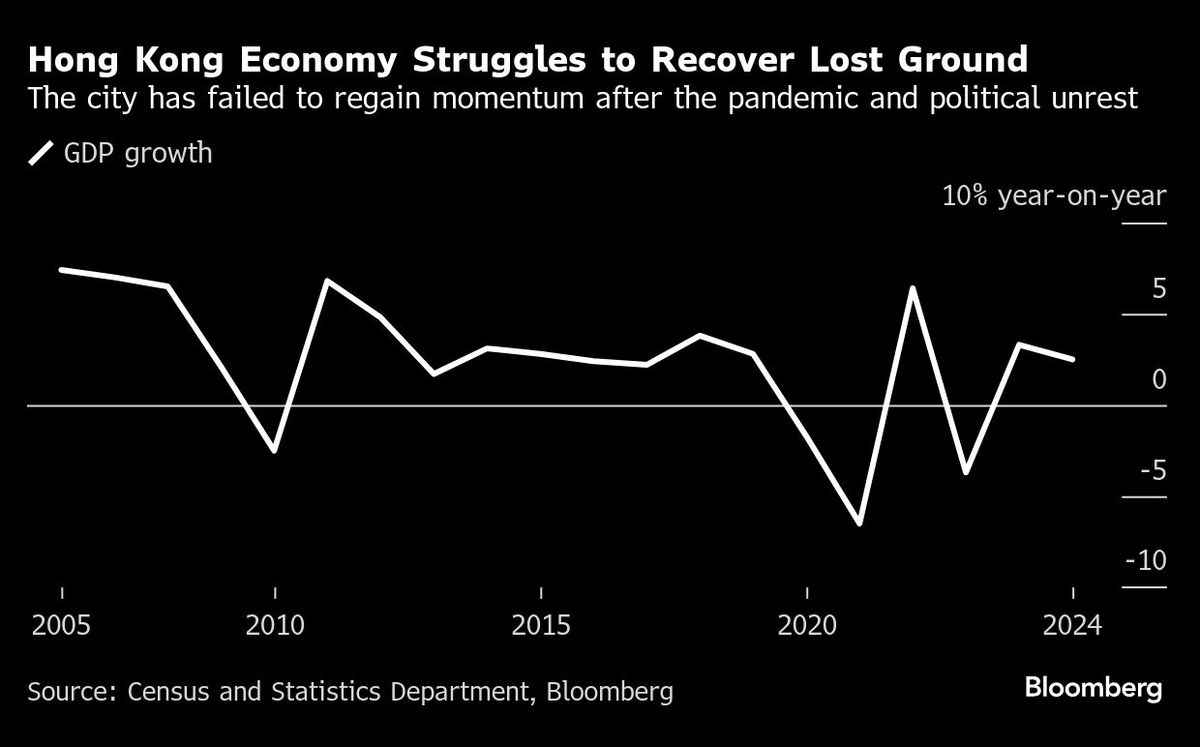

The city’s sluggish property market has been one of the biggest drags on the economy, with prices nearing their lowest levels since 2016 in recent months. Consumer spending also remains constrained, with the total value of retail sales plummeting for 10 straight months through December, the longest streak since the pandemic.

The government forecasts gross domestic product to expand 2% to 3% in 2025, compared with a 2.5% pace last year.

Seeking to find new revenue sources, the government said it will explore regulating basketball betting. This could potentially turn a portion of as much as HK$90 billion in illegal gambling turnover into tax income. Legal betting on horse races and football matches each added nearly HK$13 billion to the government coffer last year.

“The government appears to be counting on stabilisation in housing and stock markets after years of declines to buoy consumer confidence and improve the fiscal position. Rising US-China tensions and reduced room for local interest rates to decline suggest headwinds to a recovery remain strong,” said Bloomberg Economics.

Authorities will also raise a tax for departing air passengers to HK$200 from HK$120 and study raising tunnel tolls and traffic fines, Chan said. Transport subsidies for elderly people will also be capped.

Calling the Northern Metropolis an investment in the future, Chan said the government will issue more bonds to fund the project. Authorities have proposed new rail links, housing properties and a university for the town, with land tender for pilot sites to start later this year.

Uploaded by Magessan Varatharaja

- Xi's showdown with Li Ka-shing threatens China’s pro-business push

- Tan Kean Soon steps down as T7 Global executive deputy chairman, board says no operational impact

- Company auditor loses RM1.29m to investment scam

- Volvo Car brings back Samuelsson as CEO to steer turnaround

- Perak emerges as Malaysia's No 1 sweet corn producer