This article first appeared in Wealth, The Edge Malaysia Weekly on February 24, 2025 - March 2, 2025

Momentum is shifting for Malaysia’s private investment scene after more than 20 years of lacklustre performance.

Economists believe the country may be on the cusp of an economic expansion phase, bolstered by private investments. This is partly reflected in the steadily rising foreign and domestic direct investments. There is optimism that such a trend will continue at least in the short to medium term.

Private investment was once the leading contributor to the nation’s economic development before the 1997/98 Asian financial crisis (AFC), but its share of Malaysia’s gross domestic product (GDP) has faltered since. At the same time, private consumption and household debt, as a share to Malaysia’s GDP, continue to rise, indicating such a growth model may be unsustainable.

According to data provided by the Malaysian Investment Development Authority (Mida) annual reports, approved private investment in the manufacturing, service and primary sectors has been expanding steadily after the Covid-19 pandemic.

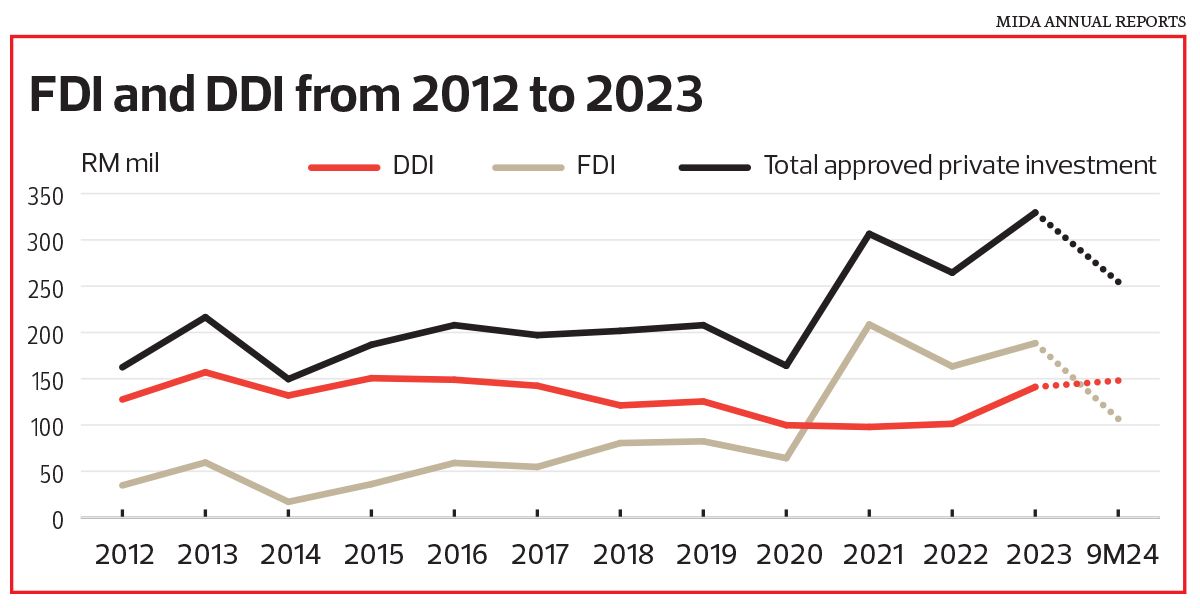

Approved private investment was at RM164 billion in 2020 at the height of the pandemic, 21% lower than a year earlier. But the figure almost doubled the next year, coming in at about RM307 billion, and rose to a multiyear high of RM329.5 billion in 2023.

As at the third quarter of 2024 (3Q2024), approved private investment was at RM255 billion, seemingly on track to rival or surpass last year’s figure. Astute Fund Management Bhd CEO Clement Chew expects the figure to hit approximately RM340 billion in 2024.

It is worth noting that from 2012 to 2020, domestic direct investment (DDI) far exceeded foreign direct investment (FDI). But the situation turned around from 2021 to 2023.

Sunway University Business School professor of economics Dr Yeah Kim Leng says FDI has contributed hugely to rising private investment as a share of GDP, showing that Malaysia is indeed a beneficiary of the ongoing and intensifying trade war between the US and China.

“The high share of FDI, compared to the tepid domestic investment, has been particularly pronounced since 2021, coinciding with the post-pandemic recovery.

“The surge in foreign investment also reflects the ongoing supply chain reconfiguration arising from the continuing US-China trade tension and technological disputes, with Malaysia a beneficiary of reshoring and new investments [pouring in] from both the US and Chinese firms,” he says.

HSBC economist for Asean Yun Liu says Malaysia is seeing a “renaissance” in both DDI and FDI in recent years.

“This is mostly evident in strong FDI inflows, reflecting Malaysia’s rising significance in the global supply chain post-pandemic, especially its positioning in the global tech supply chain. Since the intensification of trade tensions, Chinese FDI has expanded in Malaysia’s manufacturing sector, with a large part concentrated in green [renewable energy] sectors,” she says.

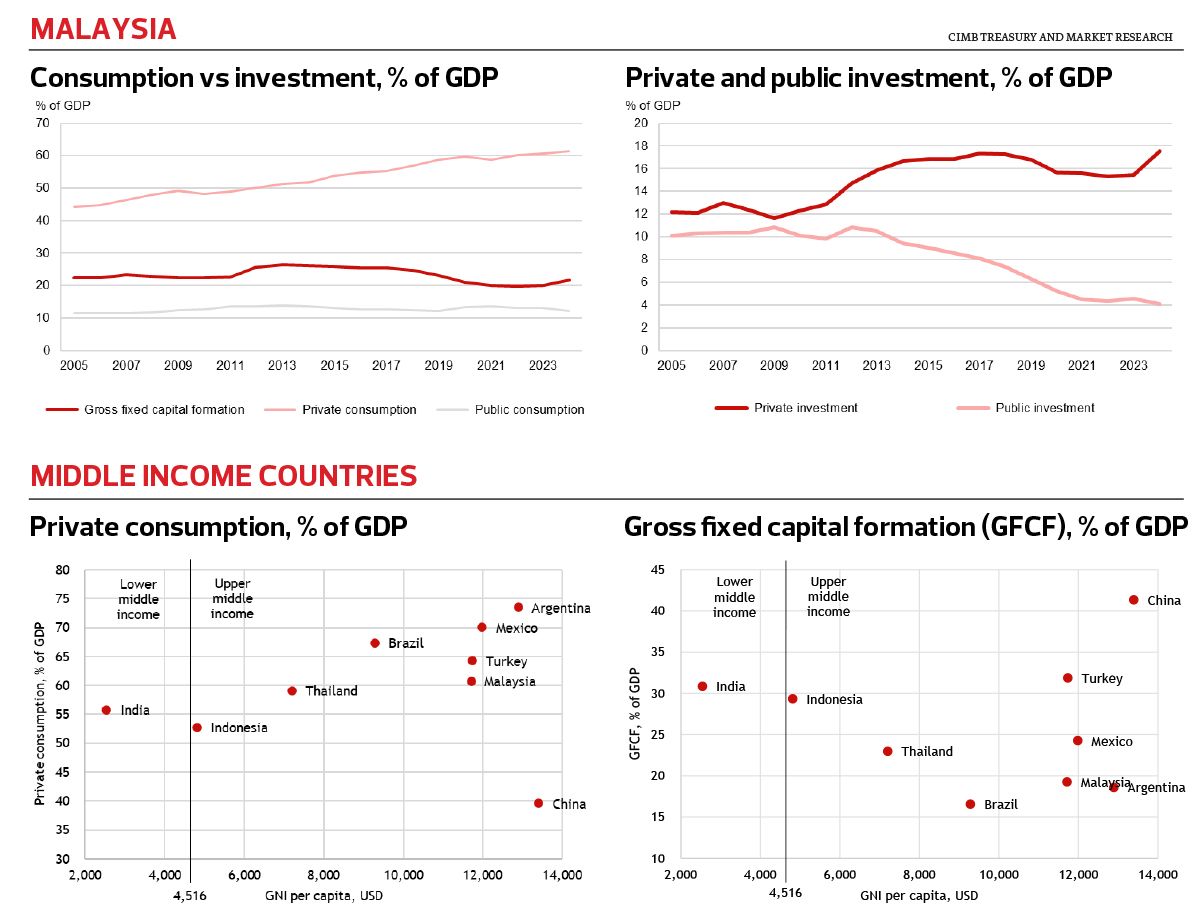

However, economists point out that gross fixed capital formation (GFCF), instead of figures provided by Mida, is used by the government to calculate the private investment contribution to the country’s GDP. It paints a more accurate picture of how much capital has been invested in the economy.

The key differences between the two are “timing” and “realisation”, says Woon Khai Jhek, head of the economic research department and senior economist at RAM Rating Services Bhd.

Approved private investments represent commitments by companies to invest in Malaysia. These are forward-looking figures that indicate potential future investments, but do not reflect actual spending at the time of approval. Some may take months or years to materialise, while others might not proceed at all due to changing business conditions.

GFCF, on the other hand, is part of the country’s GDP calculation and measures actual investment spending on fixed assets — including buildings, machinery and equipment — within a given period. It reflects money that has already been spent and work that has been carried out, making it a more accurate measure of investment growth in the economy.

“Another distinction is that approved private investments [by Mida] do not account for infrastructure spending, which can be significant in driving economic activity. GFCF, however, captures this because it includes construction and capital formation activities,” says Woon.

In summary, Woon says Mida’s figures provide a good leading indicator of future investment trends, while GFCF gives a clearer picture of how much investment is actually taking place in the economy.

Socio-Economic Research Centre (SERC) executive director Lee Heng Guie explains that GFCF means acquisitions of fixed assets made not only by private businesses, but also the public sector, for new capital expenditure and existing capacity expansion to increase output.

Is a reversal happening?

Stripping out the private investment portion from the overall GFCF figure, Sunway University’s Yeah points out that Malaysian private investment share of GDP was at 21% and 32.6% in 1990 and 1997, respectively.

From 1998 to 2011, the number fell sharply to an annual average of 12%. It then inched up to 17.3% in 2017 and 2018, but slipped to an average of 15.8% between 2019 and 2023.

“In the first three quarters of 2024, private investment grew at 12.2% over the previous corresponding period and its share to GDP rose to 17.6%. The investment uptick portends the country’s favourable growth prospects, but the investment remains below potential level. Reaching a private investment share of 20% to 25% of GDP would signify an enduring strengthening of the country’s economic growth and resilience.

“Since private investment is volatile in nature, a sustained high single- or low double-digit increases over several years are needed to affirm an investment-led growth,” he says.

SERC’s Lee says Malaysia’s private investment as a share of total GDP had declined steeply during and after the AFC. Major events that contributed to the fall include the tech bubble burst in 2001, the outbreak of the Severe Acute Respiratory Syndrome (SARS) epidemic in 2003, and the 2008-09 global financial crisis.

Concurring with Yeah, he says private investment registered a spectacular performance in the first nine months of 2024.

“We expect a multiyear expansion of private investment in high-growth, high-value industries, such as technology, semiconductor, renewable energy, data centres, healthcare, chemical and real estate, as well as potential opportunities in the Johor-Singapore Special Economic Zone [JS-SEZ],” he says.

Heavy reliance on private consumption with rising debt level

Economists point out that post-AFC, Malaysia’s economic development has been increasingly driven by private consumption while private investment has taken a back seat. Household debt levels have risen in tandem in the last two decades.

With private investment back in the limelight, especially with capital flowing into high-growth, high-value sectors, it is laying the foundation for Malaysia to move up the value chain and become a high-income nation.

“[Private investment] leads to new products or services, capacity expansion or industrial upgrading that raises output, productivity and competitiveness, thereby contributing to higher income and employment,” says Yeah.

Investment-led growth, he says, can make Malaysia a more diversified economy and helps the nation move up the value chain and technology ladder. It is essential for the nation to transition into a modern and advanced economy through sustainable development.

Consumption-led growth, on the other hand, is sustainable only when income is rising, unemployment is low and consumer confidence is maintained. However, excessive debt-driven consumption growth is unsustainable and vulnerable to interest rates, employment and other economic shocks.

“Healthy levels of investment and consumption [that contribute to the country’s economic growth] are needed to achieve high and sustained growth,” Yeah adds.

Just how big has private consumption grown as a share of Malaysia’s GDP? Yeah says private consumption or household spending as a share of GDP increased steadily to 60.8% in 2023 from 41.1% in 1999.

He says Malaysia’s current private consumption share to GDP is higher than the average of 47.9% for upper middle-income nations and 58.7% of high-income countries.

Among Asean countries, only the Philippines has a higher private consumption share to GDP than Malaysia at 76.5%. Thailand comes after Malaysia at 57.7%.

The steadily rising role of private consumption in sustaining Malaysia’s economic growth can be attributed to population expansion, growing middle class with higher disposable income, steady labour market expansion, robust consumer credit lending and government assistance programmes, such as cash handouts, Yeah says.

Meanwhile, Lee points out that means Malaysian household income grew by 5.9% per annum to RM8,479 in 2022 from RM2,472 in 2000. But household debt levels went up quite substantially.

“Households went on a debt-fuelled spending spree with household debt-to-GDP rising from 63.9% in 2008 to as high as 89.1% in 2015,” says Lee.

According to data provided by Bank Negara Malaysia (Bank Negara), household debt-to-GDP was at multiyear high in 2020, at 93.2%, when the pandemic struck. It fell to 88.9% and 81% in 2021 and 2022, and rose to 84.2% in 2023.

Bank Negara’s Financial Stability Review in the first half of 2024 shows that household-debt-to-GDP stood at 83.8%, “broadly unchanged since December 2023 as household debt grew in line with the pace of economic activity”.

The report pointed out that household resilience continued to be supported by favourable economic and labour market conditions. Risks arising from buy now, pay later (BNPL) schemes, a relatively new form of payments that allows consumers to make staggered payments upon purchasing items, continue to be limited. BNPL exposure remains small at just over 0.1% of overall household debt.

Bank Negara said household financial assets expanded at a faster pace and remained adequate to cover more than two times of overall household debt, while household borrowings that may be at higher risk of default dropped to 4.4% of total household loans as compared with 4.8% in December 2023.

In an emailed response to Wealth, CIMB Treasury and Markets Research says both private consumption and investment are important drivers of economic growth.

“Nonetheless, investment generally has a greater multiplier effect than consumption. GFCF has the potential to lift long-term economic growth potential by expanding production capabilities, creating job opportunities, fostering productivity improvements and technological innovations. It is crucial, especially for developing economies, in their economic transformation journey and improving the standard of living.”

Maintaining momentum

Economists agree that it is imperative that the government continues to keep the ball rolling to attract more investments into Malaysia.

“For Malaysia in 2025, maintaining the private investment momentum achieved last year, while raising the income level [of the people] to make it more equitable to sustain private consumption [growth] are among the key policy imperatives,” says Yeah.

RAM’s Woon says the government should focus on creating a conducive investment environment and providing targeted policy support. It needs to provide investors and businesses with clear, consistent policies for them to make long-term investment decisions.

Reducing bureaucratic inefficiencies and ensuring regulatory transparency are crucial to attracting domestic and foreign investors. Continued investment in physical and digital infrastructures (including 5G rollout, industrial parks and efficient logistics) is equally important.

“Besides that, talent development and workforce readiness are also critical to ensure Malaysia remains an attractive investment destination. The expansion of training programmes, upskilling initiatives and industry-academic collaborations will help ensure Malaysia remains competitive,” he says.

Woon’s view is shared by both Yeah and Lee. The latter adds that continued economic reform will be essential to mitigate both internal and external risks.

“These include ongoing fiscal consolidation to rebuild fiscal buffers, contain debt levels and strengthen social protection framework, among others,” Lee says.

HSBC’s Yun says one thing worth keeping an eye on is the New Investment Incentive Framework (NIIF), expected to be unveiled in the first quarter of this year and implemented in the third quarter by the government.

“Malaysia needs a set of new incentives to lure FDI into high-tech sectors that produce high-value jobs,” she says.

The incentives, announced by the government in Budget 2025, will be backed by a RM1 billion strategic fund, designed to cultivate local talent and promote high-value activities in the electrical and electronics, and artificial intelligence sectors, according to news reports.

Minister of Investment, Trade and Industry Tengku Datuk Seri Zafrul Abdul Aziz says the government needs to rethink the incentives it can use to attract foreign investment into the country, with the 15% global minimum tax (GMT) on multinational corporations coming into effect next year.

With GMT in place, the government would no longer be able to offer zero tax rates and Malaysia would have to offer other incentives such as talent and green energy to attract foreign investments.

“Incentives also can’t be given out randomly. They have to be more targeted towards industries that can really add value to the country’s economy,” he adds.

Save by subscribing to us for your print and/or digital copy.

P/S: The Edge is also available on Apple's App Store and Android's Google Play.

- Appellate court upholds quashing of proposed RM86.77 mil fine against Grab, two others

- Affin Bank to distribute Bitcoin fund managed by Halogen Capital

- Malaysian shares dip as investors return from holiday with caution

- Private hospitals association reject calls for three-year costs freeze, regulation of pharmaceutical pricing

- Richest woman in Indonesia loses US$3.6b in just three days

- FBM KLCI down 0.66% to 1,517.66 on March 19, 2025

- Mah Sing tops out M Astra

- YTL Power aims to launch first Nvidia supercomputer as early as July, among first in Asia Pacific

- Foreign workers' EPF contribution a game changer to retain workforce and hire more local talent

- Dewan Negara passes Malaysian Media Council Bill