This article first appeared in Capital, The Edge Malaysia Weekly on February 24, 2025 - March 2, 2025

Oil and gas sector

NEUTRAL

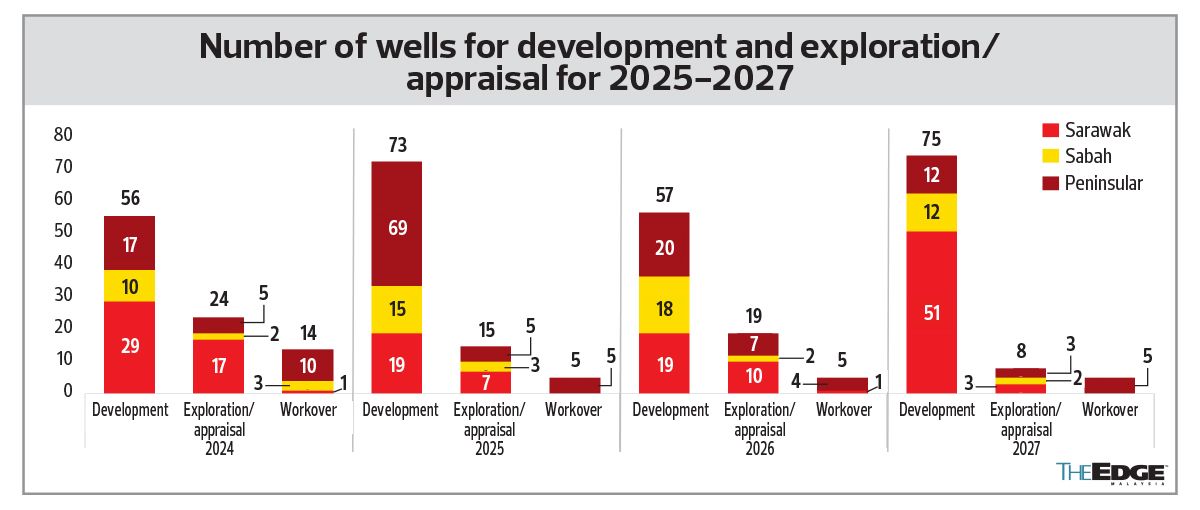

AMINVESTMENT BANK RESEARCH (FEB 17): Petroliam Nasional Bhd (Petronas) released its annual Activity Outlook 2025-2027, which appears to lay out a better-than-expected programme in the near term. We expect this will provide temporary reprieve to sector valuations for service providers after the heavy selldown since 3Q2024.

Nevertheless, we maintain our “neutral” call on the sector as sectoral risks continue to be an overhang and earnings come off from a strong base effect.

Though not in full, we note positive revisions in critical areas, particularly: (a) floating structures; and (b) decommissioning — in line with the higher exploration/appraisal and development activities and the number of ageing wells in Malaysia. We see new contract plays from within this space and potential winners in MISC Bhd (KL:MISC) and Dayang Enterprise Holdings Bhd (KL:DAYANG), premised on their respective competitive advantage including relationships with key stakeholders and existing position as the leading players in the region.

Meanwhile, we believe the focus for segments that have seen significant contract awards — especially maintenance, construction and modification (MCM)/hook-up and commissioning (HUC) — will be execution. With 2025 seeing another year of carry-over work, we gather the market expects a year of peak earnings. Companies under our coverage that had exceeded our estimated order book wins include Dayang (RM4 billion versus RM3.5 billion target) and Deleum Bhd (KL:DELEUM) (RM1 billion versus RM500 million target).

Offshore support vessel (OSV) requirements for production appear steady in the medium term, while drilling will see minor fluctuations until 2027. Despite the latter’s mixed outlook, the supply gap remains large, in our view, and will put continued constraints on charter rates in the near term. Within this space, we favour Keyfield International Bhd (KL:KEYFIELD) over its peers due to its favourable mix and ability to expand its fleet size. Notably, Petronas sees further pressure in the <80 metric ton anchor handling tug supply (AHTS) vessel space — presenting a case for increasing the vessel age limit, which would benefit select players including Dayang, Marine & General Bhd (KL:M&G) and Alam Maritim Resources Bhd (KL:ALAM).

Notably, the jack-up rig segment saw the biggest downward revision, exceeding our expectations. We expect a lower marketed utilisation rate of about 70%, which will inevitably put further downward pressure on charter rates. Investors are likely to focus on execution for geographic diversification by key players such as Velesto Energy Bhd (KL:VELESTO).

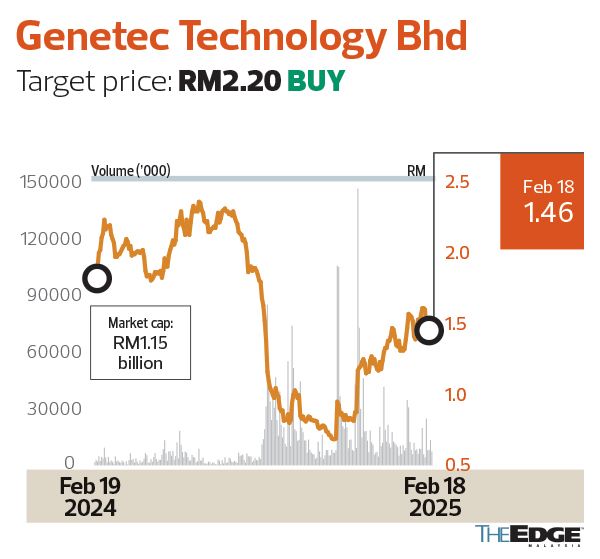

Genetec Technology Bhd

Target price: RM2.20 BUY

CIMB SECURITIES (FEB 17): Genetec’s (KL:GENETEC) growth momentum accelerates with over RM100 million in new orders from a new segment for its US customer. We are positive on this development as it marks the group’s successful expansion beyond battery cells and pack assembly. Backed by a robust RM300 million order backlog and a RM300 million tender book, we expect Genetec to add RM680 million in new orders in FY2025–26 (versus RM575 million in FY2023–24).

Beyond automotive and electric vehicles, Genetec is actively pursuing diversification into the semiconductor industry. The company is currently working on a proof-of-concept automation line for wafer deposition equipment for a US-based front-end semiconductor production equipment customer. This project, with potential delivery in 2H2025, could mark Genetec’s first foray into front-end semiconductor automation.

We see strong long-term opportunities in this space, especially as Genetec’s prospective customer plans to double its Singapore manufacturing capacity in the coming years. This expansion presents a compelling avenue for Genetec to establish a foothold in the front-end semiconductor segment, in our view.

We raise our EPS projections by 2% to 16%, upgrade our target price to RM2.20 (based on a higher 21 times PER), and reiterate our “buy” call, driven by a stronger order pipeline and earnings diversification.

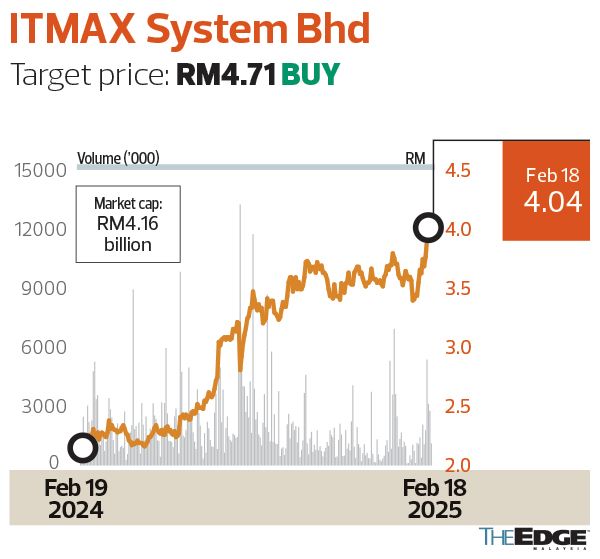

ITMAX System Bhd

Target price: RM4.71 BUY

HONG LEONG INVESTMENT BANK RESEARCH (FEB 17): ITMAX (KL:ITMAX) is expanding rapidly across key regions, securing major contracts in Kuala Lumpur, Johor and Penang while advancing its technology. In Kuala Lumpur, it has doubled its CCTV coverage to 10,000 units and is well positioned for future contracts. In Johor, the group has secured RM373.2 million in smart-city contracts and now manages 60,000 outdoor parking bays. In Penang, ITMAX won its second contract to upgrade 513 CCTVs, gaining a foothold in the state’s smart-city transformation. To stay ahead, it is developing a vision language model (VLM) to enhance its platform with artificial intelligence (AI)-driven insights.

VLMs are advanced AI models capable of processing and understanding both images and text, enabling more intuitive interactions with visual data. This technology will allow users to engage with the platform through language queries, making it easier to extract meaningful insights from complex video data. By combining text and image analysis, the VLM will enhance the intelligence and responsiveness of ITMAX’s smart-city platform, providing valuable insights to improve safety and operational efficiency.

We opine that ITMAX deserves a premium valuation as it has unique direct exposure to the AI theme, especially at the application level. We believe that this home-grown smart city integrated system and solution provider is a compelling stock, given its multiyear growth potential on the back of solid order and tender books.

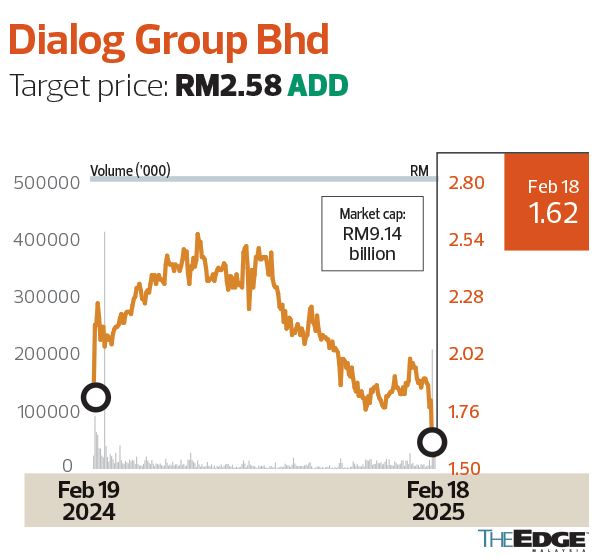

Dialog Group Bhd

Target price: RM2.58 ADD

CGS INTERNATIONAL RESEARCH (FEB 18): Dialog’s (KL:DIALOG) share price plunged 19% to an intraday low of RM1.47 on Feb 14, after it disclosed unexpected losses for its 2QFY2025 results.

In our interaction with investors, we noted that there were two camps with opposing views. One group thought that Dialog’s credibility with the market had been damaged by large engineering, procurement, construction and commissioning (EPCC) loss provisions and the unexpected write-off of its investments in the malic acid and recycled polyethylene terephthalate pellets (r-PET) plants in its 2QFY2025 results (since Dialog had previously guided that there would be no further EPCC losses after June 30, 2024) and that this may lead to a valuation derating.

Another group felt that while the losses and write-offs were regrettable, Dialog’s share price will eventually recover because the company’s quarterly earnings will return to the normal RM140 million to RM150 million run rate from 3QFY2025 onwards. We share the views of the latter group, because nothing will restore management credibility faster than actual results delivery.

Other potential rerating catalysts include: (1) new contracts in the pipeline that may add 20% to 30% to its tank terminal capacity by 2028, in our estimate; (2) ongoing upstream developments that may also more than double its current oil and gas output over the next three to five years; and (3) Dialog’s plans for the execution of three to four plant turnaround jobs scheduled for FY2026, which could accentuate the turnaround from a weak FY2025.

Save by subscribing to us for your print and/or digital copy.

P/S: The Edge is also available on Apple's App Store and Android's Google Play.

- Mr DIY founder Tan Yu Yeh relinquishes vice chairman post, to serve as adviser

- 50,000 Malaysian jobs at risk, business chamber warns as it calls for urgent US tariff mitigation council

- Malaysia refutes 47% US import tariff claim, takes measures to prioritise well-being of businesses and people

- Trump hits China tariff retaliation, says policy will remain

- China retaliation on US farm goods hits soybeans, bolstering Brazil

- ‘Worst-case scenario’ for tech wipes $1.4 trillion from Nasdaq

- Anwar says impact of latest US tariff on nation's economy still being assessed

- Tok Mat, Rubio discuss bilateral relations, Asean-US Special Summit date

- US solar’s hoarding habit will help blunt sting from Trump tariffs

- Wall Street rout drags Nasdaq near bear market