The plantation sector could outperform on the back of higher average CPO selling prices in the final quarter of 2024. (Photo by SD Guthrie Annual Report)

This article first appeared in Capital, The Edge Malaysia Weekly on February 24, 2025 - March 2, 2025

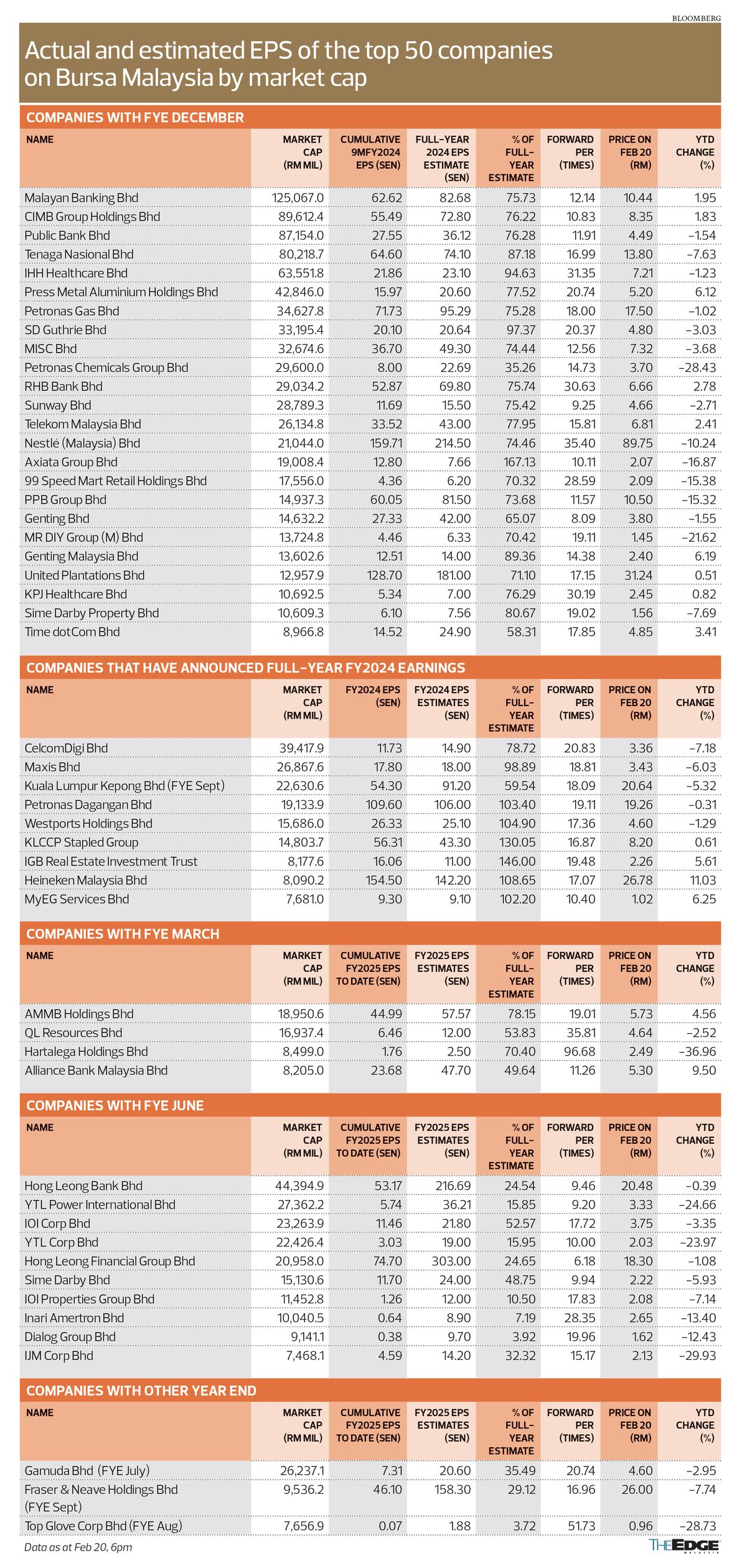

THE financial results reporting season for the quarter ended Dec 31, 2024, is already underway. And looking at Bloomberg data, it is likely that the large capitalisation companies on Bursa Malaysia whose financial year ends on Dec 31 are set to meet or exceed analysts’ earnings expectations.

So far, of the 69 companies with a market capitalisation of RM5 billion and above (as at Feb 19), 18 of them had already achieved about 75% or more of analysts’ earnings estimates for FY2024 by 9MFY2024 ended Sept 30, according to Bloomberg data. (These 18 companies exclude those that have already announced their full-year FY2024 financial results.)

Notably, IHH Healthcare Bhd (KL:IHH) and SD Guthrie Bhd (KL:SDG) are two of the companies whose cumulative nine-month results made up 90% or more of the analysts’ full-year earnings estimates. IHH’s 9MFY2024 earnings per share totalled 21.86 sen, while analysts’ average full-year EPS estimate stood at 23.1 sen.

Last year was a good one for the hospital operator, which saw a significant pickup in its operations across various locations due to sustained demand, more patients requiring acute care and price adjustments to counter inflation. Revenue per inpatient admission was higher across the board, while inpatient admission also grew during the year.

IHH completed the acquisition of Island Hospital in Penang in November last year. The 600-bed facility is expected to generate RM200 million in synergies for the healthcare group over the next five years.

As for agribusiness giant SD Guthrie, its 9MFY2024 EPS amounted to 20.1 sen, just 2.6% shy of analysts’ average forecast EPS of 20.64 sen. However, it is worth noting that its EPS for 9MFY2024 is lower than the 24 sen for 9MFY2023.

Analysts say SD Guthrie could see a higher net profit quarter on quarter in 4QFY2024 as a result of the higher average selling price of crude palm oil (CPO) and better output. Furthermore, it is set to recognise more land disposal gains in the quarter ended Dec 31, 2024.

In the final quarter of 2024, spot CPO prices tracked by the Malaysian Palm Oil Board rose 17.39% to end the year at RM4,920 per tonne. The average for the quarter stood at RM4,840 per tonne compared with RM3,999 in the previous quarter and RM3,678 in 4Q2023.

Of the large-cap companies with a Dec 31 financial year end, 14 of them were 25% to 50% short of analysts’ full-year earnings estimates as at 9MFY2024. Two companies that achieved slightly more than half of analysts’ full-year earnings estimates by 9MFY2024 are ViTrox Corp Bhd (KL:VITROX) and Time dotCom Bhd (KL:TIMECOM).

Like many of its peers in the automated test equipment market, ViTrox has been in a bind with slowing demand for its automated inspection boards (AIB). Its cumulative earnings for 9MFY2024 amounted to 3.58 sen, or 55% of analysts’ earnings estimate of 6.5 sen for FY2024. The company was also hit by foreign exchange losses in the third quarter as the ringgit strengthened against the US dollar.

CIMB Securities said in its Oct 25, 2024, report that while it expected an increase in AIB demand to boost sales volume in 4QFY2024, the amount is unlikely to fully compensate for the shortfall in 1HFY2024. It added that the strengthening ringgit against the US dollar will weigh on ViTrox’s FY2024 earnings.

The research house subsequently revised downwards its earnings forecast for ViTrox by 9% to 6.1 sen from 6.8 sen previously. Its estimate is close to analysts’ average EPS estimate of 6.5 sen.

ViTrox’s share price closed at RM3.64 last Thursday, down 9.23% year to date.

With its 9MFY2024 EPS of 14.52 sen, Time dotCom is still 42% shy of analysts’ average full-year EPS estimate of 24.9 sen. Its earnings have slowly declined in the last three quarters, from 5.99 sen per share in 1QFY2024 to 5.36 sen in 2QFY2024 and 3.18 sen in 3QFY2024.

Time dotCom’s share price closed at RM4.85 last Thursday, up 3.41% year to date.

One large-cap company that could struggle to meet analysts’ average full-year earnings estimate is Petronas Chemicals Group Bhd (KL:PCHEM), having hit only 35% of analysts’ full-year expectations by 9MFY2024.

Notably, PetChem in 3QFY2024 incurred a net loss for the first time since its listing more than 10 years ago. It registered a net loss of RM789 million, with an unrealised foreign exchange (forex) loss of RM1.1 billion during the quarter, without which it would have made an estimated net profit of RM352 million. The group’s earnings were affected by the sharp depreciation in the US dollar, mainly due to its investment in Pengerang Petrochemical Co Sdn Bhd (PPC).

There was also a larger-than-expected interest expense incurred at PPC, which dragged the 9MFY2024 net profit to RM656 million, or eight sen per share, from RM1.58 billion, or 20 sen per share, for 9MFY2023.

AmInvestment Bank Research says it expects PetChem’s 4QFY2024 earnings results to be soft as it does not see a recovery in the prices of olefins and derivatives (O&D) and specialities anytime soon.

PetChem had lost 28.43% of its value year to date, based on its closing price of RM3.70 last Thursday.

Meanwhile, 17 companies with a market capitalisation of RM5 billion and above had already released their full-year earnings results for FY2024 at the time of writing, including one with a Sept 30 financial year end. Of these companies, 10 had exceeded analysts’ average full-year earnings estimates. Real estate investment trusts (REITs) saw the biggest difference when compared with analysts’ average full-year earnings estimates, according to Bloomberg data.

IGB REIT (KL:IGBREIT) reported earnings per unit (EPU) of 16.06 sen for FY2024, compared with the estimated 11 sen on Bloomberg, while Sunway REIT (KL:SUNREIT) reported an EPU of 15.02 sen for FY2024, compared with the average estimate of 10.3 sen on Bloomberg.

Kenanga Research has an “outperform” call on IGB REIT, saying that it continues to like the counter for its resilient portfolio, with its high occupancy rates and ability to cater to a wide range of income groups. The research house has a target price of RM2.20 for the REIT.

As for Sunway REIT, AmInvestment Research sees stronger distribution income in FY2025, underpinned by the full-year recognition of rent from assets that were recently acquired, which include six hypermarkets, an industrial property in Penang, Sunway 163 Mall in Mont’Kiara and Sunway Kluang Mall in Johor. The research house added that the reconfigured retail space at Sunway Pyramid Mall is expected to flow through to its revenue and net property income in FY2025.

AmInvestment Research has a “buy” call on Sunway REIT, with a fair value of RM2.11 per unit.

Notably, one company that has been highlighted by analysts for having exceeded expectations is My E.G. Services Bhd (KL:MYEG). The technology solutions provider recorded a net profit of RM697.55 million, or 9.3 sen per share, about 41% higher than its net profit of RM487.56 million, or 6.6 sen per share, a year earlier.

The company also beat analysts’ expectations of 9.1 sen per share for FY2024. This came on the back of contribution from its blockchain segment, which accounted for 45% of the group’s total revenue.

My E.G. has been reaping the fruits of its entry into the blockchain segment as its earnings in FY2024 were lifted by contributions from its Web3 application service on the Zetrix blockchain platform, digital ID registration and transactions, as well as the sale of Zetrix tokens.

Maybank Investment Bank Research highlighted that for the first time on record, My E.G. had disclosed in its 4Q earnings results its revenue from its concession-related services provided to the Road Transport Department and Immigration Department, which made up 24% and 16% of its quarterly revenue respectively. The research house is expecting the group’s blockchain-related business to breach the 50% mark in terms of revenue contribution by mid-2025 as it intensifies efforts to transition away from its bread-and-butter concession business.

“While the sale of Zetrix tokens will continue to be capped at one million units per quarter throughout FY2025, we expect ZTrade and ZCert to continue gaining traction amid the snowballing blockchain adoption trend in Malaysia, China and Asean,” says the research house, which has a “buy” call on the stock and a target price of RM1.70, pegged to an FY2026 PER of 20 times.

Last Thursday, My E.G. closed at RM1.02, up 6.25% year to date.

As the results reporting season heads into the last week of February, analysts note that the plantation sector could outperform on the back of higher average CPO selling prices in the final quarter of 2024. At the time of writing, none of the large-cap plantation stocks had announced their earnings for the October-December quarter.

Save by subscribing to us for your print and/or digital copy.

P/S: The Edge is also available on Apple's App Store and Android's Google Play.

- Mr DIY founder Tan Yu Yeh relinquishes vice chairman post, to serve as adviser

- 50,000 Malaysian jobs at risk, business chamber warns as it calls for urgent US tariff mitigation council

- Malaysia refutes 47% US import tariff claim, takes measures to prioritise well-being of businesses and people

- Trump hits China tariff retaliation, says policy will remain

- China retaliation on US farm goods hits soybeans, bolstering Brazil

- ‘Worst-case scenario’ for tech wipes $1.4 trillion from Nasdaq

- Anwar says impact of latest US tariff on nation's economy still being assessed

- Tok Mat, Rubio discuss bilateral relations, Asean-US Special Summit date

- US solar’s hoarding habit will help blunt sting from Trump tariffs

- Wall Street rout drags Nasdaq near bear market