This article first appeared in The Edge Malaysia Weekly on February 24, 2025 - March 2, 2025

LOW-cost carrier Capital A Bhd’s (KL:CAPITALA) path to financial recovery is reaching a critical juncture. The aviation group, led by CEO Tan Sri Tony Fernandes, is racing to resolve its negative equity, finalise regulatory approvals for its restructuring and cut costs amid ongoing supply chain disruptions.

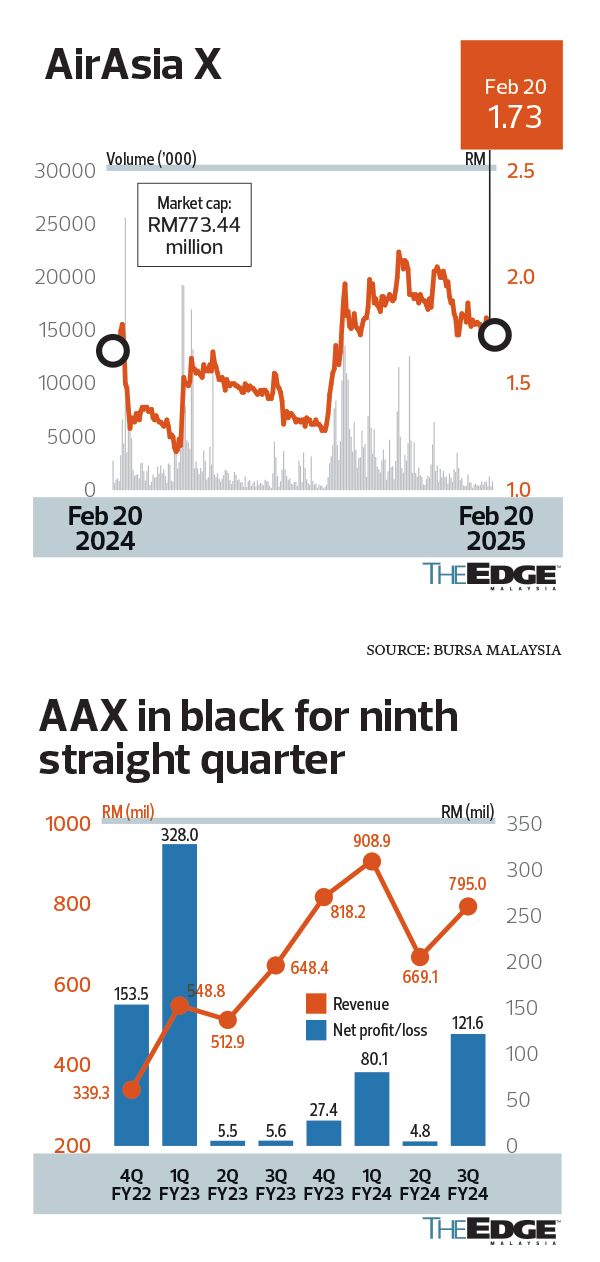

At the heart of this transformation is the long-awaited sale of Capital A’s short-haul airline business to its medium-haul affiliate AirAsia X Bhd (KL:AAX) in a RM6.8 billion share-and-debt deal — a move to address Capital A’s Practice Note 17 (PN17) status, which is crucial for its survival.

Following multiple extensions to complete the proposed disposal of AirAsia Aviation Group Ltd (AAAGL) and AirAsia Bhd (AAB) to AAX and a pending court ruling on Capital A’s capital reduction exercise, market watchers remain cautious about whether the PN17 exit will materialise as scheduled. Investors also took a cue from Malaysia Airlines Bhd’s underperformance last year; the airline had to resort to temporary capacity cuts in 4Q2024 due to a shortage of parts, a hold-up in aircraft delivery and workforce attrition. The national carrier is expected to book a loss for the financial year ended Dec 31, 2024.

“We’re almost there,” says Fernandes in an interview with The Edge, pointing to ongoing discussions with Bursa Malaysia and a court hearing set for late March.

“We are going to really relook at everything — our lease rates, cost structure, and so on. People really took advantage of us while we were [in bad shape]. But I’ve got my mojo back,” he adds. In April last year, the 60-year-old entrepreneur had agreed to put aside retirement plans for another five years, enabling him to continue to lead Capital A.

“I’m tired of people making assumptions — we are going to give a profit forecast for 2025 as most of the unknowns are gone,” Fernandes says. “This (2025) is the year where I’m very clear what Capital A is going to become.”

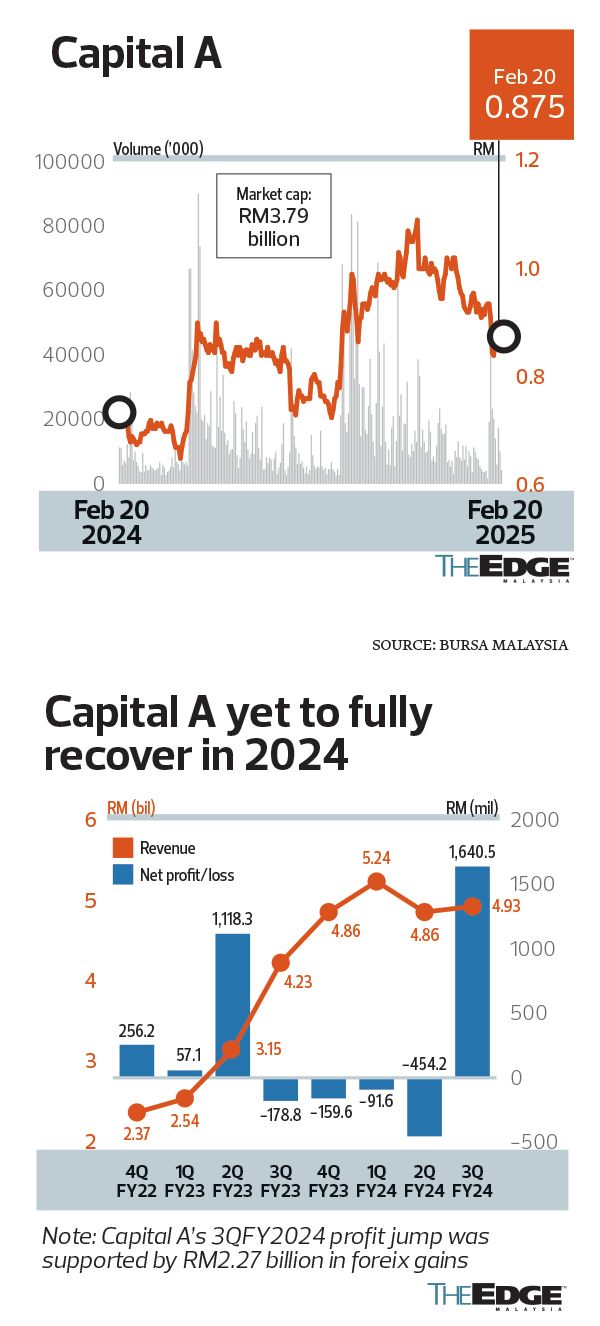

Capital A is en route to its second consecutive year of profitability after four years in the red from 2019 to 2022. It booked RM836.99 million in net profit in the financial year ended Dec 31, 2023 (FY2023), from a net loss of RM2.48 billion in FY2022.

It managed to post a net profit of RM1.09 billion for the cumulative nine months ended Sept 30, 2024 (9MFY2024), an 82% increase from RM600.63 million a year ago, in tandem with the upsurge in domestic and international travel. Revenue for 9MFY2024 grew 51.69% year on year to RM15.04 billion from RM9.91 billion. Its results for 4QFY2024 are set to be released on Feb 26.

Still, while regulatory hurdles remain, Capital A is simultaneously battling high operating and finance costs, which are burning through its available cash. The financial situation is compounded by fleet shortages and supply chain challenges.

The group was forced to ground around 90% of its fleet during the Covid-19 pandemic. It spent “at least RM1 billion” to bring its 25 grounded aircraft back into service in 2024. That works out to around RM40 million in start-up costs per plane, back-of-the-envelope calcuation shows. It operated an additional 17 aircraft in 4Q2024, compared with just eight planes in the first three quarters of 2024, its operating statistics show.

Today, it has another 14 planes that remain inactive, which is burning the group around US$4.9 million in leasing costs each month.

“If the average lease rate is US$350,000 per month, that’s US$4.9 million in monthly cash burn ... plus lost revenue and profit. That’s my top priority (to restart the remaining 14 planes),” Fernandes explains, underscoring the urgency of getting planes back into service.

April deadline for aviation business acquisition

The restructuring exercise will see a NewCo called AirAsia Group Bhd (AAGB) take over AAX’s listing status. Capital A will inject its AirAsia aviation businesses into AAGB in exchange for RM3 billion worth of AAGB shares, part of which will be distributed to Capital A’s shareholders, and RM3.8 billion in debt novation.

The cut-off date for Capital A and AAX’s aviation business sale and purchase agreement for the restructuring exercise has been extended twice, once in October last year and again in January to March 24.

According to Fernandes, the extension was partly to accommodate the court date to secure an order for its capital reduction exercise pursuant to the proposed distribution of AAGB shares.

An approval is also pending from Bursa for Capital A’s PN17 regularisation plan that was submitted on Dec 23, 2024. A site visit was held last week as part of the process, Fernandes says. “They have come back with three rounds of questions … we’re almost there in getting it (the regularisation plan) approved.”

The restructuring also hinges on AAX raising RM1 billion via private placement.

“We may look at getting a little bit more … the due diligence is being done by the new investor. I can confirm it is almost done,” Fernandes says, declining to disclose the investor’s identity (see sidebar).

Capital A’s proposed regularisation plan “will not result in a significant change in the business direction or policy”, according to its filing dated Oct 23, 2024. It requires two quarters of profit after the plan’s execution to facilitate Capital A’s PN17 exit.

“We’re almost there in agreeing the quarters [needed],” says Fernandes, who eyes April to complete the merger of the AirAsia short-haul brands with AAX, address Capital A’s negative equity position and complete AAGB’s listing status takeover from AAX.

Cost cutting continues in 2025

Apart from handling its PN17 status — which Fernandes described as having “distracted” the management until recently — the heavy work is now focused on restoring its fleet, optimising costs and boosting revenue both from its airlines business and non-aviation businesses like air cargo unit Teleport Everywhere Pte Ltd and its maintenance, repairs and overhaul (MRO) services unit Asia Digital Engineering Sdn Bhd (ADE).

The group is looking to bring 14 aircraft back to the skies this year, but engine sourcing has been one of its challenges.

While agreeing that such targets would depend on the suppliers, Fernandes says AirAsia is “making about US$200 million in claims [against the suppliers] for the losses we have incurred” due to the supply chain issues.

He adds that AirAsia has reached an agreement with CrowdStrike Holdings Inc to offset some of its losses suffered on flight cancellations in July 2024 after a flawed update from the US cybersecurity firm crashed Windows PCs all over the world. “We are happy with the solution,” he says, without elaborating.

The group is also reassessing its new aircraft deliveries. Initially planned for 11 new planes this year, Fernandes says Capital A is “not in a rush for new planes in 2025”, but is exploring options for its order book of over 360 new Airbus planes that will be delivered through to 2035.

At the same time, the focus is to address its costs and shrink its debt size, having resorted to the likes of mezzanine financing that has much higher interest charges.

“We’ve got about US$500 million of cash debt; all [of which are] quite expensive… Then we have some lessor debt of US$200 million. So that makes up to about US$700 million,” he says.

The group is now working towards paying off at least half of that debt and to refinance the others in local currencies for much more reasonable terms. “That will improve our earnings dramatically,” he says.

As at end-September 2024, Capital A had RM6.06 billion in borrowings, of which RM3.82 billion were in US dollars. Finance costs in 9MFY2024 alone totalled RM866.55 million.

At the same time, the group is expecting to complete its route optimisation by April, having identified the best routes for the best fares and returns.

“We were just putting up flights [after the reopening of Malaysia’s borders in April 2022]. [Since then,] markets have changed across China and India, and domestic and Asean routes are now much stronger. We have begun the optimisation process (to focus on profitable routes).”

‘Capital A’s non-aviation companies will aid AirAsia’

Upon completion of the restructuring, Capital A will own just 18.39% in the aviation business through AAGB. The bulk of its earnings will come from Teleport, ADE, its online travel agency AirAsia Move and branding unit Capital A International, which has already sourced branding fee income from the aviation business.

“Ancillary income is fantastic upside for us,” says Fernandes. “The companies we’ve created at Capital A are only going to aid AirAsia.”

ADE, with 16 hangar lines and approval to service airlines within jurisdiction of eight Asean countries and Europe, focuses on narrow-body aircraft, reducing maintenance costs and turnaround times.

“Creating ADE is not asset stripping. If I have 250 planes and ADE is fixing the planes three days faster than in Singapore, that gives me 750 days of extra flying … my view is that we need at least 32 lines. It’s mostly AirAsia planes [being served presently]. We’re building four lines now.”

Teleport has expanded to 39 partners and increased belly space utilisation from 12% to 20%. As for AirAsia Move, the online travel agency (OTA) helps airlines to hold on to customers and the ancillary income otherwise lost to other booking platforms.

“AirAsia Move is the first OTA that’s giving airlines commission for hotel [booking] sales.

“Other airlines have tried splitting loyalty businesses or creating engineering units, but no one is as vertically integrated as us. My last goal is to maximise the synergy between Capital A and AirAsia,” says Fernandes.

He also points to other tailwinds including the privatisation of Malaysia Airports Holdings Bhd (MAHB) (KL:AIRPORT) by the Khazanah Nasional Bhd-led Gateway Development Alliance (GDA) consortium, and a maturing landscape where airlines in the region are clearer in the distinction between low-cost and full-service airlines.

“I’m very excited about GDA. We have a group of people who are talking to us, that are saying how can 1+1 equal three? They used a major word. They called us ‘customer’. We now have an airport [operator] that wants to win and knows that we’re an important part of them winning. That’s massive.”

Capital A has long had a tumultuous relationship with its landlord, MAHB. Both companies have clashed in the past over issues ranging from cost, facilities and service levels at Terminal 2 of Kuala Lumpur International Airport to differences over the passenger service charges.

Since touching a high of RM1.09 in November last year, shares of Capital A have fallen to close at 87.5 sen last Thursday, valuing the group at RM3.79 billion and at 6.8 times forward price-to earnings multiple, according to Bloomberg data. AAX shares, similarly, have retreated from its November high of RM2.12 and settled at RM1.73 on Thursday, valuing the group at RM773 million.

Under Capital A, its flagship airline AirAsia’s passenger count for 2024 (including Cambodia AirAsia that is nearing one year in operation), touched 85% of pre-pandemic levels. Long-haul carrier AAX also carried more passengers per flight, notwithstanding the smaller fleet size that capped passenger count at just 65% compared to pre-pandemic.

Analysts have yet to adjust their forecasts for Capital A and AAX, pending the 4QFY2024 financial results announcement this week. Of the 11 analysts covering Capital A’s stock, four have a “buy” call, six a “hold” rating and one a “sell” recommendation, with an average target price of RM1.09. AAX is similarly trading below consensus target price of RM2.58 between two analysts, at RM1.73 per share.

Indeed, much needs to be done to relieve itself from the pandemic drags. For example, Capital A’s trade and payables of RM4.64 billion is still double pre-pandemic’s RM2.03 billion, and similarly, advance sales stood at RM2.03 billion, compared with RM1.18 billion at end-2019.

Fernandes concludes that 2025 will still be a year of “rebuilding”. “The year 2024 was about forming the strategy, 2025 is about finishing off [the work] on cost structure, and in 2026, I really want [AirAsia] to be one of the world’s most profitable airlines.”

- Sapura Resources sues ex-MD Datuk Shahriman and others for over RM3 mil in damages

- Chin Hin, HeiTech Padu, MyEG, MSM, Ranhill, Toyo Ventures, YNH Property

- Anwar receives courtesy visit from tech giant Oracle, discusses AI and digital innovation

- Malaysia must brace for potential US pharmaceutical tariff, says Dzulkefly

- Sell-off accelerates on Wall Street, traders weigh risks as tariffs on China increased to 145%

- UK jobs market sees biggest jump in people looking for work since 2020, says survey

- Gold climbs to US$3,200 for first time as recession anxiety mounts

- Employers allowed to use levy collection to train new graduates — HR minister

- MORNING CALL: 11/4/25

- Rich Indonesians, wary of Prabowo’s policies, send wealth overseas