KUALA LUMPUR (Feb 21): Kossan Rubber Industries Bhd (KL:KOSSAN) is not fully out of the woods, analysts said, as the glove manufacturer wades through a glut of supply and faces intensifying competition from Chinese rivals.

The latest earnings report was weaker than expected, but investors may have taken into account the negative outlook following the recent sharp selldown of Kossan shares. At least three analysts upgraded the stock following Thursday’s results announcement and briefing.

Investors should look beyond the shortfall as well as the upcoming weakness in the first three months of 2025 before inventories of Kossan's US customers deplete by May and "start to drive volume growth," RHB Investment Bank said in upgrading the stock to ‘buy’ from ‘neutral’.

Shares of Kossan have plunged more than 20% this week, ahead of the earnings announcement, a casualty of weaker-than-expected results posted on Tuesday by its larger peer Hartalega Holdings Bhd (KL:HARTA).

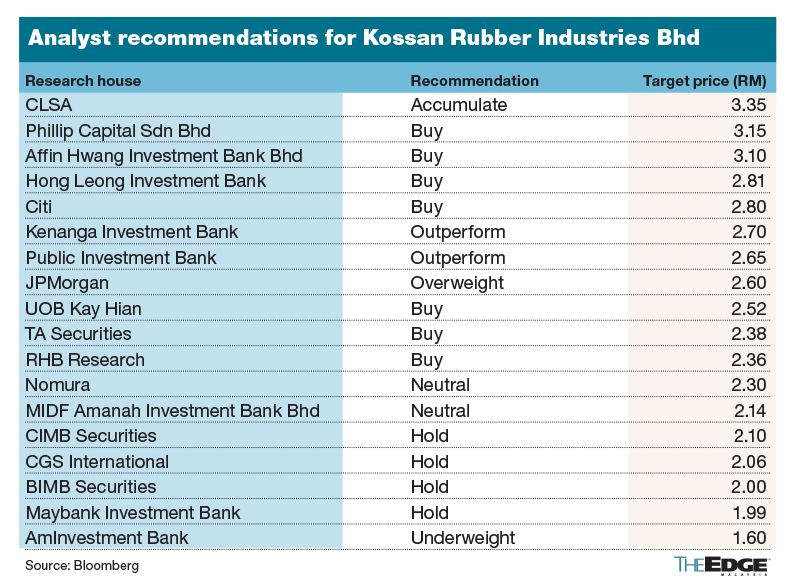

UOB Kay Hian also upgraded Kossan to ‘buy’, while BIMB Securities lifted the stock to ‘hold’ from ‘sell’. Following the rating changes, Kossan now has 11 ‘buy’, six ‘hold’, and one sell calls from research houses.

The average target price is RM2.53, according to Bloomberg, suggesting a potential return of up to 28% from its last price in the next 12 months.

“On top of the recovery thesis, we believe Kossan has potential rerating prospects, considering its more favourable financial profile” compared to Hartalega, said Hong Leong Investment Bank, which maintained its ‘buy’ call.

BIMB Securities, however, cautioned that orders could still decline, as demand returns to normal levels, while competition is also expected to intensify, as Chinese players rapidly set up production facilities outside China to bypass tariffs.

“This intensifying competition makes further organic growth and a cost-plus pricing strategy increasingly difficult,” the house warned. “Overall, the rubber glove industry’s recovery to pre-Covid levels remains constrained by structural hurdles and an oversupply market.”

Kossan reported on Thursday that its net profit jumped more than 30 times to RM27.7 million in the fourth quarter ended Dec 31, 2024 (4QFY2024) in the absence of a one-off impairment. For FY2024, the company saw a ninefold increase in net profit to RM120.03 million.

Shares of Kossan paused for Friday's midday trading break at RM1.96, valuing the company at RM5 billion.

- Sapura Resources sues ex-MD Datuk Shahriman and others for over RM3 mil in damages

- Chin Hin, HeiTech Padu, MyEG, MSM, Ranhill, Toyo Ventures, YNH Property

- Anwar receives courtesy visit from tech giant Oracle, discusses AI and digital innovation

- Singapore man accused of Nvidia chip fraud wields global connections

- Stocks extend drop, dollar falls on tariff woes