KUALA LUMPUR (Feb 19): Maxis Bhd’s (KL:MAXIS) spending on 5G could weigh on its earnings, potentially dragging on dividend payouts ahead, analysts flagged, after the mobile network operator reported its 2024 results.

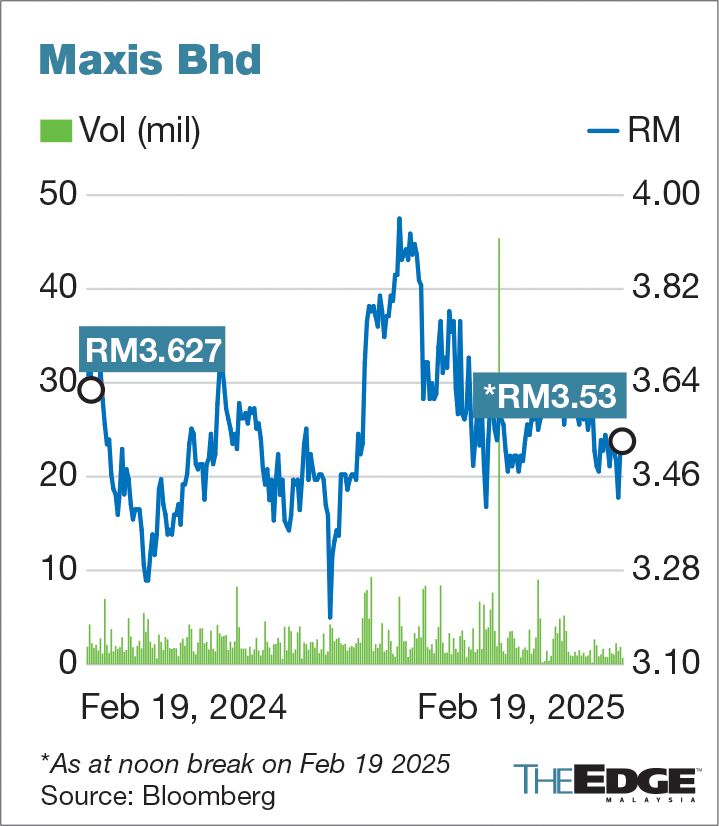

Investors are cautious, along with the majority of analysts, after core net profit for the financial year ended Dec 31, 2024 came in largely in line with consensus expectations. Shares of Maxis were trading in a tight range on Wednesday, and were last up 0.3% at RM3.53 at the midday trading break.

“Looking ahead, higher 5G access costs could weigh on earnings,” Kenanga Investment Bank said and kept its ‘market perform’ call. “This cost pressure could be a larger drag for Maxis compared to its main competitors, due to lower 5G traffic volumes from its significantly smaller subscriber base.”

Maxis has barely moved, down about 3% since the start of 2025. The telecommunications sector has been shaken up since November 2024 by news of U Mobile Sdn Bhd’s appointment to deploy Malaysia’s second 5G network over its larger peers.

Maxis, CelcomDigi Bhd (KL:CDB), and other mobile network operators will now have to devise product and services strategy, as well as contend with paying fees to access the 5G infrastructure by state-owned Digital Nasional Bhd.

There are now 13 ‘hold’, 10 ‘buy’ and one ‘sell’ calls out of 24 research houses covering Maxis. The average target price is RM3.98, according to Bloomberg, suggesting a potential return of up to 13% in the next 12 months from the last price.

Maxis’ 5G strategy may impact dividends, posing near-term uncertainty, Hong Leong Investment Bank flagged, even as the company’s “quality of service as differentiation” will drive leadership in data adoption.

On its part, Maxis is guiding for a “low single-digit growth” in service revenue and a “flat to low single-digit” increase in earnings before interest, tax, depreciation and amortisation (Ebitda). It also plans to keep capital expenditure under RM1 billion.

For CIMB Securities, Maxis’s earnings could be flat in the next two years, as rising 5G wholesale fees offset low single-digit service revenue growth.

However, the stock is still a ‘buy’, thanks to its attractive enterprise valuation at 10.8 times its operating free cash flow, which is below 11.4 times for CelcomDigi, the research house said in a note. Maxis' dividend yield will also be solid at 4.8%-5.1% in 2025-2027, the house added.

- Sapura Resources sues ex-MD Datuk Shahriman and others for over RM3 mil in damages

- Chin Hin, HeiTech Padu, MyEG, MSM, Ranhill, Toyo Ventures, YNH Property

- Anwar receives courtesy visit from tech giant Oracle, discusses AI and digital innovation

- Malaysia must brace for potential US pharmaceutical tariff, says Dzulkefly

- Sell-off accelerates on Wall Street, traders weigh risks as tariffs on China increased to 145%

- UK jobs market sees biggest jump in people looking for work since 2020, says survey

- Gold climbs to US$3,200 for first time as recession anxiety mounts

- Employers allowed to use levy collection to train new graduates — HR minister

- MORNING CALL: 11/4/25

- Rich Indonesians, wary of Prabowo’s policies, send wealth overseas