KUALA LUMPUR (Feb 19): Analysts on Wednesday slashed Hartalega Holdings Bhd’s (KL:HARTA) earnings outlook on lower sales volume and average selling prices (ASPs), as well as shrinking margins after the glovemaker's third-quarter results (3QFY2025) missed expectations.

Hong Leong Investment Bank (HLIB) said it expects Hartalega to swing into the red due to weaker ASPs, sales volume and higher costs.

The research house cut its FY2025/FY2026/FY2027 forecasts by 81%/69%/38% respectively and kept a “hold” call on Hartalega, with a lower target price (TP) of RM2.66, based on a price-to-earnings multiple of 32 times on its 2026 earnings per share.

"Globally, we have revised our timeline for medical rubber glove demand-supply dynamics to reach an equilibrium in 2026 from 2025 previously (ie the global plant utilisation rate will hit ~85%)."

HLIB said this adjustment was due to Hartalega’s lower-than-expected sales volume guidance for 4QFY2025.

Going into 4QFY2025, Hartalega targets to deliver 6.0-6.3 billion pieces per month (-17% to -21% quarter-on-quarter; versus 7.6 billion pieces in 3QFY2025) mainly due to front-loading by US customers from Chinese manufacturers in 3QFY2025, before the US' tariff implementation on Jan 1, 2025.

However, HLIB said it believes there will be a rebound in sales volume q-o-q starting from 1QFY2026 onwards.

In terms of group blended ASP, Hartalega indicated that this would be lowered by about US$1-2 per 1,000 pieces q-o-q in 4QFY2025.

This decrease primarily reflects the pass-through of lower Nitrile Butadiene Rubber prices in 3QFY2025 (-7.2% q-o-q), though the higher minimum wage (+US$0.20/1,000 pieces, effective February 2025) has already been incorporated.

CIMB Securities slashed its earnings forecast for Hartalega by 36.6%–61.7%, downgrading it to a “hold” from “buy”, with a lower TP of RM2.70, as the stock lacks near-term catalysts.

CIMB cited Hartalega's guidance of weaker q-o-q sales volume as a "negative surprise". It noted that Hartalega's 4QFY2025 utilisation rate is forecasted to decline to 70%–75% (from 3QFY2025: 86%), owing to the impact of front-loading by US buyers before tariffs on China-imported gloves were increased to 50% (from 7.5%), effective Jan 1, 2025.

"Harta shared that it has also seen more competitive ASPs in non-US markets as more Chinese glovemakers shift their focus onto sales to non-US markets. We expect Harta’s sales volume to only improve towards 1QFY26, as we estimate that US buyers will fully utilise their front-loaded purchases by May 2025 at the earliest. "

While CIMB was positive on the impact of another step-up in US tariffs on China-imported gloves from Jan 1, 2026 (to 100%), it believes that competition in the US market will also increasingly heighten.

This especially with more non-Chinese glovemakers shifting their focus to sales to the US owing to rising competition from Chinese glovemakers in non-US markets (glove ASPs in US markets carry a 5%–10% premium vs non-US markets).

Impact of China's emergence in the glove market

HLIB, citing Hartalega, said Chinese manufacturers are set to add 30 billion pieces per annum of capacity in Southeast Asia, as they seek to recapture lost market share in the US market.

These additional supplies are expected to gradually come online by mid-2026.

"As now, we believe it is still too early to price in any potential oversupply risks associated with this ‘China + 1’ strategy. All in, we expect Hartalega to deliver losses in 4QFY25 and gradually improve in future quarters," said the research house.

In terms of capacity, Hartalega has ramped up 12 lines (five billion pieces/annum) in the more efficient NGC1.5 Plant 8 back in 2QFY2025; the group plans to add another 12 lines (Plant 9) by end-2025 in order to have more efficient lines and stay competitive in the market.

This expansion will bring Hartalega’s annual installed capacity from 32 billion pieces in FY2024 to 42 billion pieces by end-2025.

"We understand that in the event of weaker-than-expected demand, Hartalega may decommission those older lines in NGC1.0. As such, we conservatively expect the elevated ramp-up costs associated with the faster lines in Plant 8 and 9 will persist at least until end-2025."

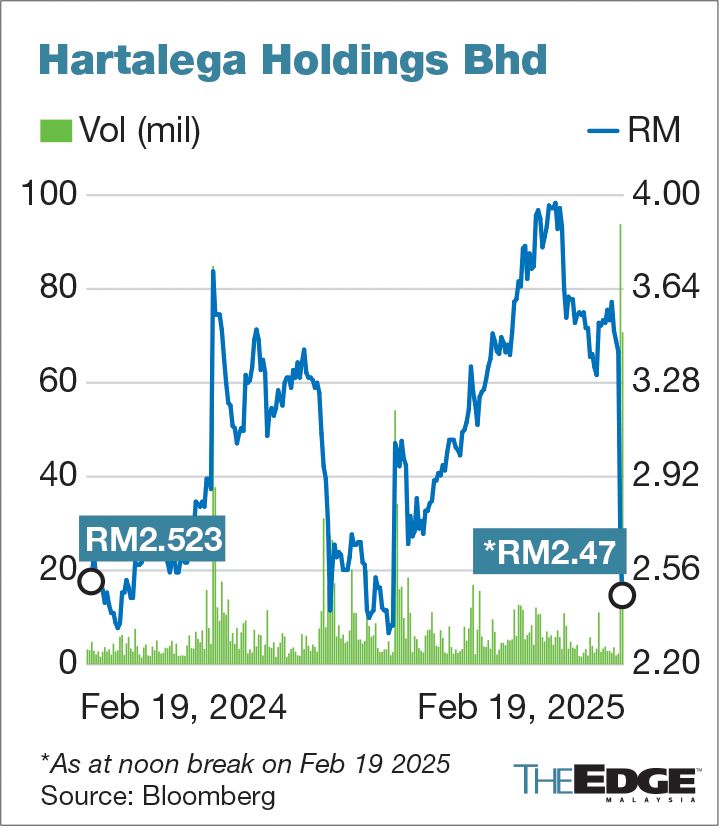

Intra-day short-selling (IDSS) in Hartalega was suspended on Tuesday after its share price fell to multiple-month lows, following the release of its third quarterly results.

HLIB noted that Hartalega’s 3QFY2025 core profit after tax and minority interests of RM25.0 million (vs - RM11.6 million in 2QFY2025, +RM3.6 million in 3QFY2024), brought 9MFY2025’s sum to RM57.2 million, which is in below the research house's (31%) and consensus’ (36%) full-year forecasts.

The counter emerged as the fifth most traded stock in early trading on Wednesday, as it rose over 1% or three sen to RM2.64, valuing the group at nearly RM9 billion.

- Sapura Resources sues ex-MD Datuk Shahriman and others for over RM3 mil in damages

- Chin Hin, HeiTech Padu, MyEG, MSM, Ranhill, Toyo Ventures, YNH Property

- Anwar receives courtesy visit from tech giant Oracle, discusses AI and digital innovation

- Singapore man accused of Nvidia chip fraud wields global connections

- Stocks extend drop, dollar falls on tariff woes