(Photo by Low Yen Yeing/The Edge)

This article first appeared in The Edge Malaysia Weekly on February 17, 2025 - February 23, 2025

PERMODALAN Nasional Bhd (PNB), one of the largest fund managers in the country, is feeling the effects of lower voluntary savings among Malaysians.

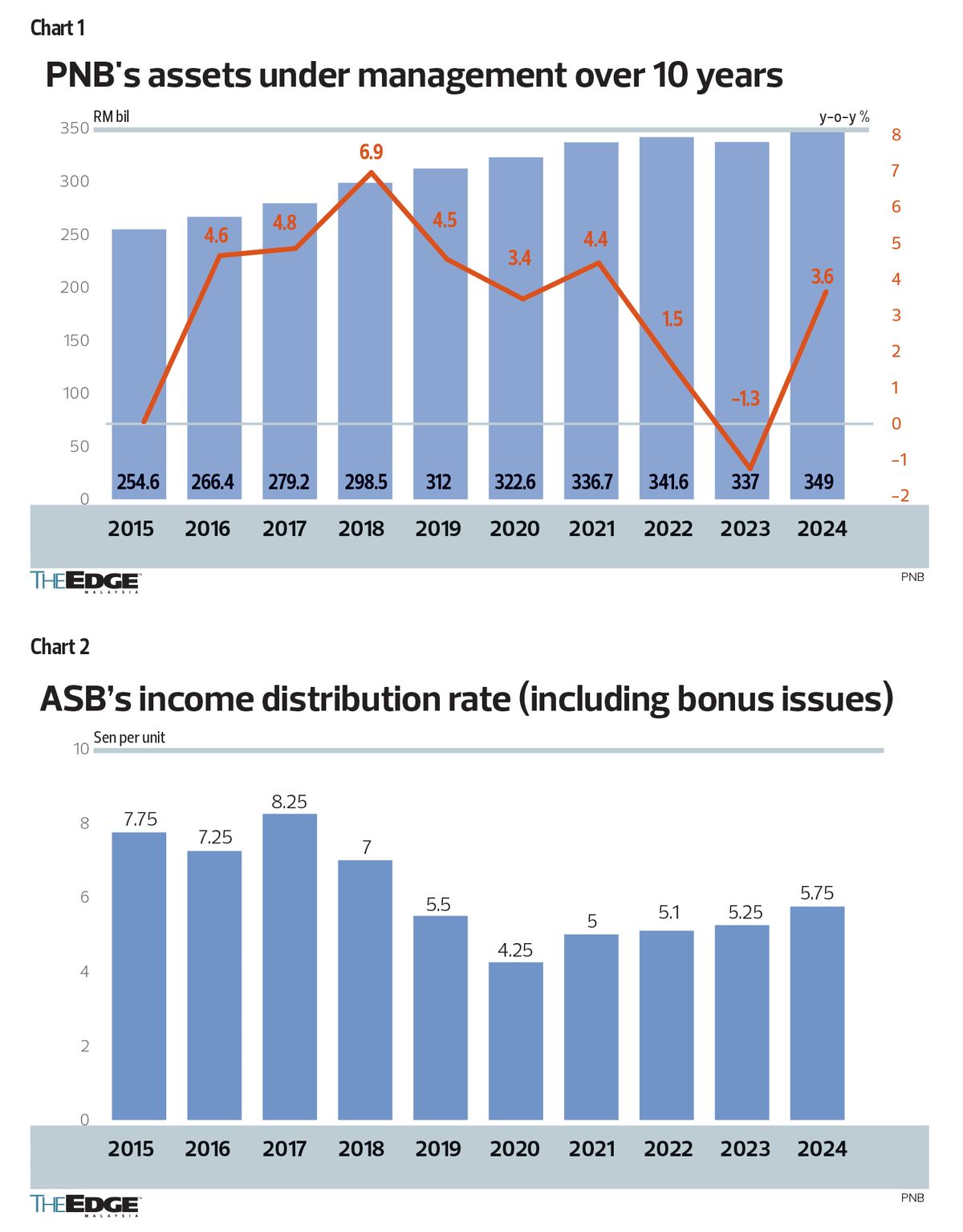

This has been identified as one of the factors behind the stagnating growth in the government-linked investment company’s (GLIC) assets under management (AUM), which stood at RM349 billion last year, presenting a key challenge to PNB’s president and group chief executive Datuk Abdul Rahman Ahmad.

“It has become an uphill challenge to get Malaysians to save and invest. This has put pressure on PNB’s ability to grow its AUM because we rely purely on voluntary savings. All investment funds need to grow their funds in a measured manner in order to deliver sustainable returns,” Abdul Rahman tells The Edge in a recent interview.

Abdul Rahman is no stranger to PNB, having held the same positions at the GLIC between 2016 and 2019 before stepping into the role of group CEO at CIMB Group Holdings Bhd (KL:CIMB) in 2020. He returned to PNB in mid-2024.

Abdul Rahman remarks during the interview that one of the main differences he observed between his first stint and the current one is the slowdown in the voluntary savings rate among Malaysians — a trend that became apparent after the pandemic.

“We probably have taken it for granted before this because of our unique nature where bumiputeras and non-bumiputeras basically invest in PNB [without much persuasion] and that has underpinned the growth of PNB over so many years. Now, we really have to strengthen promoting financial literacy and, more importantly, to serve our customers better, persuade them to save money with PNB,” he says.

Over the last 10 years, PNB’s AUM have grown at an average rate of 5% year on year (y-o-y). They slowed considerably after 2020 and even experienced a 1.3% y-o-y contraction in 2023 (see Chart 1).

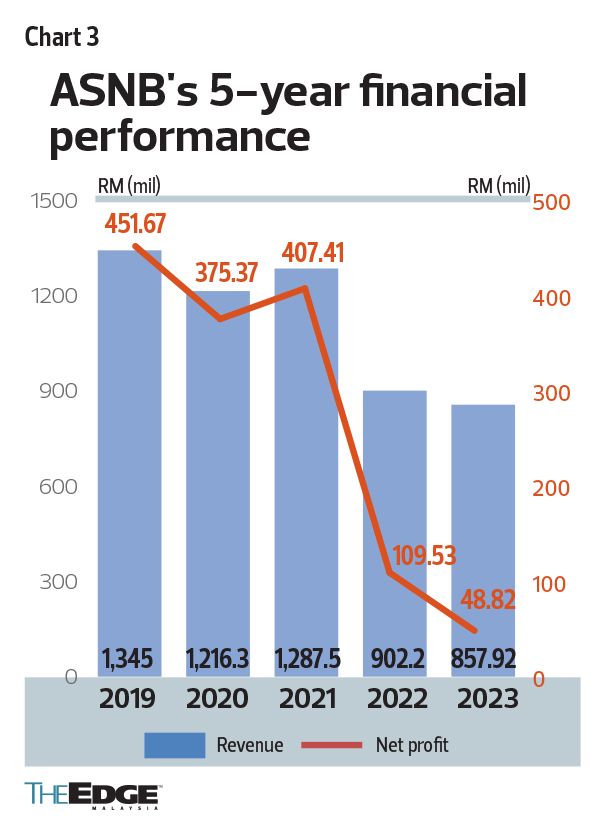

This slowdown in AUM growth impacted the revenue and net profit of Amanah Saham Nasional Bhd (ASNB), the manager of the funds and a wholly-owned subsidiary of PNB. ASNB’s revenue is made up of the fees it charges on the 18 funds it manages, including PNB’s proprietary fund, to cover the cost of operating and distributing the funds.

Revenue fell to RM857.92 million in 2023 from RM1.35 billion in 2019 while net profit declined in tandem to RM48.82 million from RM451.68 million over this period.

“During the challenging times, ASNB would give a discount on the management fee that it charges the funds and that’s the reason the profit of ASNB has been stagnant. But 2024 was a much stronger year in terms of fund growth and performance of the funds. So, the performance of ASNB in 2024 improved considerably from 2023, which you will see when the accounts are published,” explains Abdul Rahman.

PNB’s 2024 annual report is expected to be published in the middle of this year.

Abdul Rahman observes that there has been a generational consumption shift, where the propensity to consume today is higher than the propensity to save. Having said that, he does not discount the fact that the inflationary environment in recent years has also affected Malaysians’ saving habit.

“We need to tackle the issue of low income and I think the government is doing the right thing in talking about increasing income — this is extremely important. Malaysia has to migrate from a low-wage economy to a higher-wage one,” he adds.

RinggitPlus Malaysia’s Financial Literacy Survey 2024, based on responses from 3,385 participants aged 18 and above, found that 20% of Malaysians do not manage to save each month while 47% save RM500 or less per month.

It is worth noting that 53% of the respondents admitted to spending more than they earn. Also, 51% have not started investing.

Since it was formed in 1978 to achieve the objectives of the New Economic Policy, PNB has focused on contributing to the wealth of bumiputeras and all Malaysians, and uplifting the financial lives of Malaysians across generations.

It has six fixed-price funds, of which three are solely for bumiputeras and the remaining three are open to all Malaysians. The GLIC also has 11 variable-priced funds, of which two are for bumiputeras and the remaining are open to all Malaysians.

Its fixed-price funds, especially its flagship Amanah Saham Bumiputera (ASB) fund, are known to provide attractive returns to unitholders. The fixed-price funds are benchmarked against 12-month fixed deposit (FD) rates and have delivered annual income distribution of between 4.25 sen (in 2020) and 8.25 sen (in 2017) over the last decade.

“There’s no other country in the world that has this scheme whereby you can earn a higher return and still have your par value — meaning that your capital is not eroded and you have access (to it) virtually any time you want. So when we talk about returns, the challenge is how we maintain that and try to have a range above the benchmark FD rate that we aspire to deliver,” says Abdul Rahman.

However, since 2020, the income distribution per unit has been nearer the lower range of the last 10 years (see Chart 2).

Mandate to overcome AUM stagnancy

Helming PNB for the second time, Abdul Rahman says his mandate is to provide continuity of strategy and to execute it successfully.

Under the leadership of his predecessor, Ahmad Zulqarnain Onn (who left to head the Employees Provident Fund), PNB developed a strategic plan — LEAP 6 — which Abdul Rahman says he has “refined” and is effectively following through with.

The three-year plan is focused on growing PNB’s AUM to RM400 billion by 2027, through the execution of transformation across six key pillars, which are Sales & Distribution, Investment, PNB Company Transformation, Knowledge, Innovation and Sustainability.

“It’s not that we want to grow the AUM for the sake of having more funds, but if we can deliver RM400 billion by 2027, it means that we have been able to grow people’s savings as AUM are basically people’s savings,” he adds.

Abdul Rahman goes on to explain that under the first pillar, which focuses on voluntary savings, PNB is changing its approach from a passive stance to aggressively promoting financial literacy and promoting itself as an investment destination for Malaysians.

That said, while PNB is aware that this will raise its AUM, the bigger driver, according to Abdul Rahman, are the investment returns it offers, which form another pillar under LEAP 6.

He says one way to achieve better and sustainable returns for the funds, especially since a significant component of its AUM is in fixed-price funds, is through portfolio diversification.

“The asset diversification has to continue both in terms of geography and asset class. We need a diversified portfolio to deliver that [sustainable returns].”

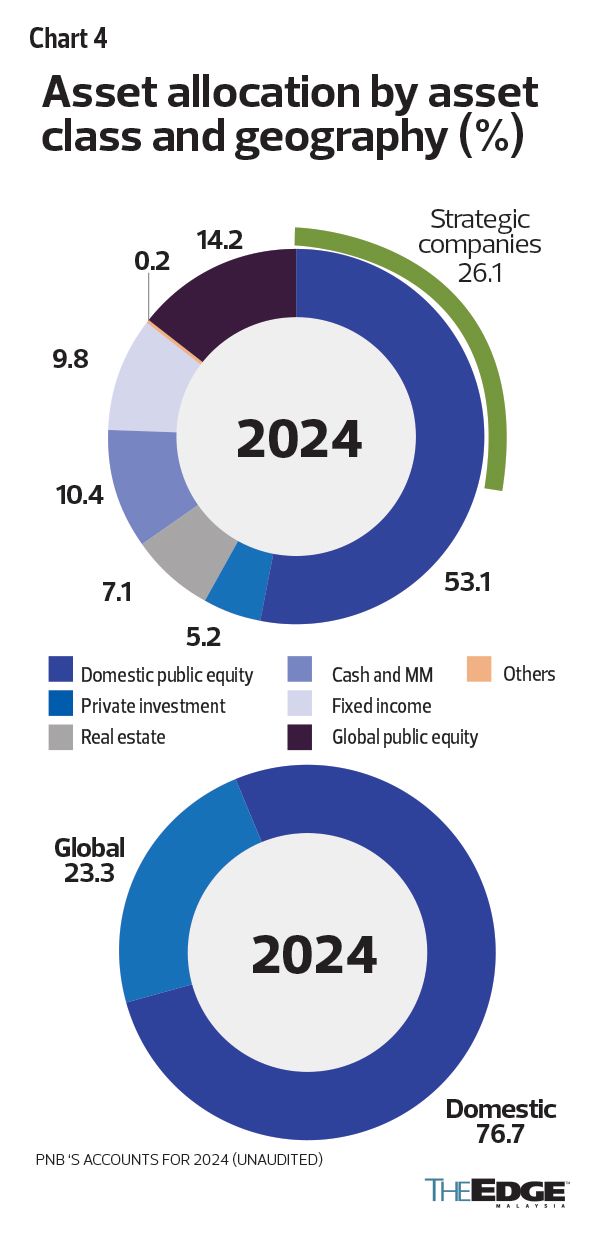

In the last decade, PNB has increased its global asset portfolio from under 2% of its AUM in 2016 to about 23.3% as at end-2024. Abdul Rahman credits the diversification strategy for this, saying the global asset portfolio has contributed to the fund and helped PNB weather the challenging years of the pandemic and post-pandemic.

PNB is looking to increase its global asset allocation to 30% by end-2027, which Abdul Rahman deems a “fair and reasonable target” and “within what the government feels is a fair diversification globally”.

“We need to be judicious in terms of understanding the importance of capital flows and keeping Malaysia’s currency strong and stable,” he says.

When asked if the government’s call last year to GLICs and government-linked companies (GLCs) to reduce their overseas investments and increase their domestic investments had affected PNB’s investment returns, Abdul Rahman says the fund has been less impacted by this because of its smaller proportion of global assets compared with other larger GLICs in Malaysia.

He highlights that PNB has been focused on bringing back the income portion of its foreign investments when there is any liquidity requirement and emphasises that the principal remains untouched.

Over half of PNB’s asset portfolio — specifically 53.1% of its AUM or RM185 billion — is invested in the local equity market. This translates into close to 10% of Bursa Malaysia’s total market capitalisation of about RM2 trillion.

The dominance of funds such as PNB as well as other GLICs in the local equity market often raises concern over whether these institutional funds are crowding out other investors, including retail investors when the stock market regulator is also trying to encourage more retail participation. Also, some say the support from GLICs reduces the volatility favoured by traders and foreign investors.

Abdul Rahman argues that the presence of GLICs in the local equity market makes it more stable compared with other markets in the region where volatility is pronounced because of the higher participation of retail and foreign investors.

Apart from the local equity market, PNB has 14.2% of its AUM in the global public equity market, 10.4% in cash and money markets, 9.8% in fixed income, 7.1% in real estate, 5.2% in private equity and 0.2% in others. (See also “PNB to make tough decisions on legacy assets” and “What went wrong at FashionValet” on Page 63.)

Malaysia’s ‘lost decade’

Another means of achieving better returns for its funds, says Abdul Rahman, is “to drive Corporate Malaysia” — particularly companies in which PNB has invested substantially — to deliver better shareholder value on a sustainable basis, given its large exposure to the local equity market.

“The share price returns of FBM KLCI on a three-year, five-year and 10-year basis, up to 2023, have been flat to negative. If taken from a total return perspective, dividend plus share price, it is a very small positive over the same periods. The bottom line is, anyone who had invested in the FBM KLCI up to 2023 would have seen a negative return. In theory, it would have been better for an investor to keep his money in fixed deposits,” he points out.

In fact, he terms the period from 2014 to 2023 as Malaysia’s “lost decade”.

“I think it is a real challenge for Corporate Malaysia or anybody who’s involved to actually overcome. We had a lost decade … Now we can debate the reasons behind that, and there are multiple reasons. And I’m not saying it’s easy [to address].”

This is where Abdul Rahman sees himself playing a role in his second stint at the GLIC: to steer Corporate Malaysia to perform better. In short, PNB could play the role of an activist investor.

“I believe boards and management in Corporate Malaysia do not spend enough time focusing on how they can deliver better returns on capital. This is something [on which] we will take the lead, particularly for our strategic companies, but it goes beyond that,” he reasons, adding that a better performance by Corporate Malaysia will help catalyse the economic growth of the country.

While Corporate Malaysia needs to “do better” in delivering better shareholder value, he is mindful that many local companies have done well. Although there are exceptions, generally, on the governance side, Corporate Malaysia has also improved from “the old days”.

“But I think the challenge now [is], how do we move not just from governance [but] to performance? I think this is a theme [in which] PNB will take the lead and will basically push,” Abdul Rahman explains, adding that this is also aligned with the Gear-Up initiative by the government to catalyse domestic investment.

PNB’s strategic companies are those in which it holds the majority or single largest stake. They include Malayan Banking Bhd (KL:MAYBANK), S P Setia Bhd (KL:SPSETIA), Duopharma Biotech Bhd (KL:DPHARMA) and Sime Darby Bhd (KL:SIME).

PNB considers companies in which it has a 10% equity interest, or above RM1 billion invested, as its core companies. They include Gamuda Bhd (KL:GAMUDA), Tenaga Nasional Bhd (KL:TENAGA) and CIMB Group.

What will PNB do to generate better value from its investee companies?

Datuk Rick Ramli, PNB’s deputy president and group chief executive who was also at the interview, says it will start by articulating the GLIC’s expectations of its investee companies. PNB typically engages with the companies’ board and explains what is expected of them. It also writes to boards where it does not have a board seat to explain its views of the company.

PNB has an escalation framework for when investee companies fail to perform, which could involve questioning the board at the AGM, private engagement dialogues or even voting against the board. The final step in the framework is to divest the stake as the last resort.

What about Sapura and Velesto?

Among its strategic investee companies, oil and gas (O&G) companies Sapura Energy Bhd (KL:SAPNRG) and Velesto Energy Bhd (KL:VELESTO), in which PNB has 44.13% and 40.5% stakes respectively, came under the spotlight in 2017 and 2018 because of their massive recapitalisation exercises to resolve their debt issues. Both were casualties of the meltdown in crude oil prices between 2014 and 2016.

Velesto undertook a recapitalisation exercise in 2017 and made a cash call. PNB stepped in, spending RM800 million on the rights issue of ordinary shares on top of the subscription for preference shares.

As for Sapura, which undertook a recapitalisation exercise in 2018 and proposed a rights issue of shares and Islamic redeemable convertible preference shares (RCPS-i) to raise RM4 billion, PNB came to its rescue by forking out RM2.68 billion for the rights issue.

Velesto has turned the corner, successfully paring down its debt and reporting a net profit of RM152.55 million for the cumulative nine months ended Sept 30, 2024 (9MFY2024).

Meanwhile, Sapura recently secured approval-in-principle from at least 75% of its financiers for the proposed restructuring of its multi-currency financing facilities.

“What is important, for Sapura in particular, is that it looks like it will survive. I think that’s probably the part that was uncertain when the capitalisation exercise took place. We fully recognised that they needed to now move to the phase of shareholder value recovery after they complete the restructuring. The good news is that I think they can once it’s all completed. It will take time,” says Abdul Rahman.

Would PNB consider injecting more capital into Sapura in the future?

“There is a need for them to actually do so, but the view is that we have done the first part of the capitalisation exercise. For prudence, we have a single company investment limit that varies from company to company. We are constrained on that and we don’t want to exceed our investment guard rails on an investment in a company, but we will be very supportive of any exercise that the company wants to undertake if they require more capital,” he says.

Rick says PNB also does a top-down assessment of its portfolio, adding that the O&G investments in its overall portfolio currently are higher than they should be.

“We are over-indexed in terms of O&G and to deliver on future returns that we would like to we will need to look at new growth areas that we are underweight on in our portfolio,” he says, pointing out that PNB is fairly underweight on healthcare, energy transition, electrical and electronics and technology in general.

Malaysia’s third investment cycle boost for the market

PNB forecasts that the Malaysian economy will grow 4.5% this year, on sustained foreign direct investment (FDI) inflows. Hanizan Hood, its chief investment officer, says the amount of approved FDIs that has been converted into actual investments in recent years, on top of policies that focus on structural reforms, will have a strong multiplier effect on the economy.

“We call the conversion of approved FDIs into actual investment as the third investment up cycle. The approved FDI conversions in the last few years were over 80% and that’s real money going into the real economy. It will trickle down to construction companies, banks, the manufacturing sector, semiconductor companies and it is across the board,” she says.

The first investment up cycle driven by FDI was in the 1980s to 1990s, when gross domestic product growth averaged 8% and the economy shifted structurally from agriculture to manufacturing. The second up cycle from 2010 to 2014 was domestic-centric, driven by the Economic Transformation Programme, Government Transformation Programme, Strategic Reform Initiatives and the 10th Malaysia Plan.

The third investment cycle will be driven by the various blueprints, namely the National Energy Transition Roadmap, Johor-Singapore Special Economic Zone and National Semiconductor Strategy, among others.

If the conversion into actual investments is properly carried through, Hanizan says, it could translate into an improvement in corporate earnings and an upward re-rating of the local stock market, which is trading at a price-earnings ratio of 14 times, below its long-term average.

However, Hanizan is also cognisant of the external factors, such as the potential tariff war between the US and other nations, that could result in short-term volatility.

“Unfortunately, we started the year with the market coming off because of these very reasons, but I think that’s not something that the market did not factor in,” she says, adding that people are taking a wait-and-see attitude.

That said, PNB believes the third investment up cycle is taking place, paving the way for stronger corporate earnings growth if corporations are able to leverage it.

Making tough decisions on legacy assets

Seated in a boardroom on the 92nd floor of Merdeka 118 — where on a clear day one can see the dome and minarets of the Sultan Salahuddin Abdul Aziz Shah Mosque in Shah Alam — Datuk Rick Ramli, Permodalan Nasional Bhd’s (PNB) deputy president and group chief executive, says the office market in Kuala Lumpur can be classified into two segments: high-quality buildings in good locations and older buildings in poor locations.

PNB is the owner of Menara Merdeka 118, the tallest building in Malaysia and the second tallest in the world. The skyscraper has added 1.7 million sq ft of net lettable area in office space to Kuala Lumpur, which has been experiencing an oversupply in the office segment for some time now.

Commenting on PNB’s real estate portfolio, which currently accounts for 7.1% of its total asset allocation, Rick says while office real estate was “very attractive” once, it is less so now. Nevertheless, he says office space should be “de-averaged”.

“There are good office spaces and bad office spaces. Good ones are those that have good sustainability credentials and good amenities while bad office buildings are those that are underappreciated and over time decline in capital value,” he explains.

While the oversupply of office space is still a prevalent issue in the Klang Valley, the demand for Grade A offices remains strong. It is worth noting that gross rent psf for Merdeka 118 is reported to be between RM10.50 and RM12.50.

Merdeka 118 has secured a pre-committed occupancy rate of 70%. As for the remaining 30%, the search is on for the right tenants, says PNB’s president and group chief executive Datuk Abdul Rahman Ahmad.

Malayan Banking Bhd (KL:MAYBANK), in which PNB holds a 37.1% stake, is one of the tenants of the mega skyscraper and is expected to relocate to the 678.9m LEED-certified Platinum tower in 2026.

According to CBRE | WTW’s Real Estate Market Outlook 2025 report, the completion of Merdeka 118, Pavilion Damansara Heights Corporate Tower 1, Menara Felcra and ATWATER Corporate Towers in 2024 put the total office supply in the Klang Valley at 125.5 million sq ft. Of this, 72% is in Kuala Lumpur.

Rick says PNB’s real estate portfolio, once comprising mainly office space, has in the last eight years been diversified to include other segments, both domestic and global. Office space is now a minor segment, although exposure in it is still a little elevated. As at end-2023, office buildings accounted for 33% of PNB’s total real estate portfolio.

“Domestically, we own a lot of legacy assets. With these assets, we need to make a call on which are worth reinvesting in and upgrading. For example, we decided that it was worth upgrading our office blocks in Damansara Heights around Jalan Dungun as it is a good precinct.

“Then there are some sub-markets where we need to make a tough call on divestment if we think the asset is not worth reinvesting in because we will not be able to get economic returns on [it],” explains Rick.

Nevertheless, Abdul Rahman says the portion of low-quality buildings in PNB’s portfolio is relatively small.

“Quite a number of [buildings in] our portfolio, apart from the new building (Merdeka 118), are assets that we can enhance. PNB sold off some of its older buildings back in 2017 and 2018 and that has continued over time. We are rebalancing our portfolio.”

The government-linked investment company’s (GLIC) old headquarters at Jalan Tun Razak was refurbished and now has an occupancy rate of 77%.

Sapura Energy Bhd (KL:SAPNRG), in which PNB has a 40.55% stake, has relocated its offices to Menara PNB.

On Menara Maybank, Abdul Rahman says: “After Maybank moves out of Menara Maybank in early 2026, we will take over the leasing of the building for 10 years, meaning that we will become the asset manager of the building. Ultimately, the expectation is that we will help Maybank lease out the building at a certain rate. We will also try to see whether there is a market for a potential buyer over time.”

Maybank owns the 35-storey Menara Maybank at 100, Jalan Tun Perak, which was completed in 1988.

Abdul Rahman says PNB’s experience with Menara PNB has shown that there is a demand for buildings in great locations, adding that the team is working out the best strategy for Menara Maybank, which is not very far from Merdeka 118 on Jalan Hang Jebat.

At the present time, PNB’s real estate portfolio has a 59:41 allocation between global and domestic assets.

Rick points out that real estate is a cyclical sector and the cycles tend to differ by city because of the supply-demand dynamics. PNB’s strategy of diversifying overseas and across the sub sectors of the real estate market has given it a “healthy exposure across good trends”, he says.

Internationally, save for the UK, PNB’s investments in property is via global real estate funds.

“Real estate is very local. If you’re not in the local market with local access on the deal flow, you probably won’t get access to good investment opportunities, so we went (to these markets) mostly via funds. Although in markets like the UK, we continue to hold assets directly because it’s a fairly transparent market and we know the market well,” explains Rick.

The GLIC’s global real estate portfolio has generated a five-year average total return of over 8.1% and a yield of 5.1%, Abdul Rahman says. Meanwhile, the average yield on cost for the domestic core real estate portfolio has been around 7% over the last six years.

Nevertheless, Rick says PNB’s real estate portfolio is at the “high end” of its allocation.

“We don’t intend to substantially grow the real estate allocation. A lot of it will probably be in rebalancing and reinvesting, but if there’s anything that makes sense, I think we can look at it.”

Save by subscribing to us for your print and/or digital copy.

P/S: The Edge is also available on Apple's App Store and Android's Google Play.

- Mr DIY founder Tan Yu Yeh relinquishes vice chairman post, to serve as adviser

- 50,000 Malaysian jobs at risk, business chamber warns as it calls for urgent US tariff mitigation council

- Malaysia refutes 47% US import tariff claim, takes measures to prioritise well-being of businesses and people

- Trump hits China tariff retaliation, says policy will remain

- China retaliation on US farm goods hits soybeans, bolstering Brazil

- ‘Worst-case scenario’ for tech wipes $1.4 trillion from Nasdaq

- Anwar says impact of latest US tariff on nation's economy still being assessed

- Tok Mat, Rubio discuss bilateral relations, Asean-US Special Summit date

- US solar’s hoarding habit will help blunt sting from Trump tariffs

- Wall Street rout drags Nasdaq near bear market