This article first appeared in Capital, The Edge Malaysia Weekly on February 17, 2025 - February 23, 2025

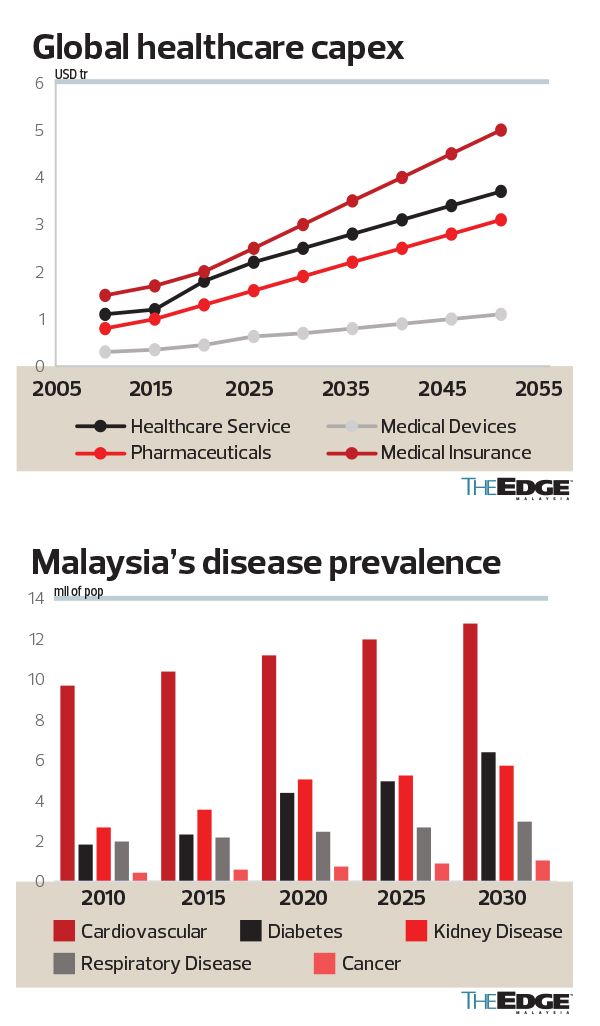

Healthcare Sector

POSITIVE

MIDF RESEARCH (FEB 10): We maintain our optimism on the sector despite the anticipated changes and updates to existing policies and programmes for the private sector. The US’ withdrawal from World Health Organization is expected to place China as the next major funder of the organisation, opening opportunities for our regional and local healthcare players to leverage pharmaceuticals and medical device trades, advanced research and development, and Chinese medical tourists.

The prevalence of human metapneumovirus (hMPV), while still below 1% in Malaysia, signals the need for more development of vaccines in preparation for any future endemics. The country’s call for a reduced dependency on vaccine imports while developing and manufacturing local vaccines is timely, and hMPV could be the right catalyst to further improve our pharmaceutical sector.

The government is expected to continue seeking a sustainable system for both patients and providers, by improving three key drivers: sustainable medical workforce; affordable and comprehensive payment system for patients; and long-term positive cost management.

Private hospitals are expected to remain resilient on the back of surging inpatient visits and in-house treatments from both domestic patients and medical tourists. The increased demand for inpatient treatments is anticipated to persist in the near term, fuelled by the continuous affordability of healthcare services and the safety of the country for foreigners and locals alike.

Our top pick is KPJ Healthcare Bhd (KL:KPJ). We maintain a “buy” call for KPJ with a revised target price of RM2.75. The new target price is derived from pegging a new PER of 31 times to EPS 2025 of 8.7 sen. The increase in PER from 29 times is taking into consideration the robust medical tourism and expansion plans for KPJ coming into 2025, coupled with the expectation of a stable financial performance moving forward.

We like KPJ for its strong financial performance. The group has shown consistent revenue growth, with a significant surge in net income. Additionally, KPJ boasts the largest network of private hospitals in Malaysia (over 29 hospitals), with the opportunity to expand its bed capacity and services (about 5,000 beds by 2028).

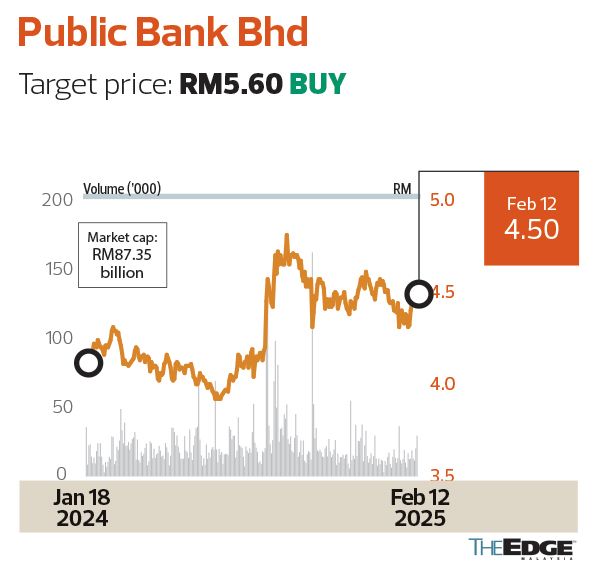

Public Bank Bhd

Target price: RM5.60 BUY

CIMB SECURITIES (FEB 10): Public Bank Bhd’s (KL:PBBANK) share price has been flattish in recent months, which we believe is likely related to concerns about share overhang issue arising from its restricted offer for sale scheme, which was first announced in October 2024. However, at the current share price level, dividend yield is now likely to exceed 5% from FY25, based on organic growth alone.

Notably, Public Bank recently acknowledged that its group Common Equity Tier 1 (CET1) ratio, at 14.3% in 3QFY24 (2QFY24: 14.5%), is high and very conservative, further hinting that there is scope to take it down further to 13%. This implies extra capital of RM3.4 billion or RM0.18 per share that may be released, if the bank rightsizes its group CET1 ratio to 13%.

We believe there is ample room for Public Bank to raise its dividend payout ratio to at least 60% (FY23: 55.5%) on a sustainable basis. We currently assume a dividend payout ratio of 58% for FY25, 58.2% for FY26, and 58.3% for FY27.

We maintain a “buy” call and our target price for FY25 is maintained at RM5.60.

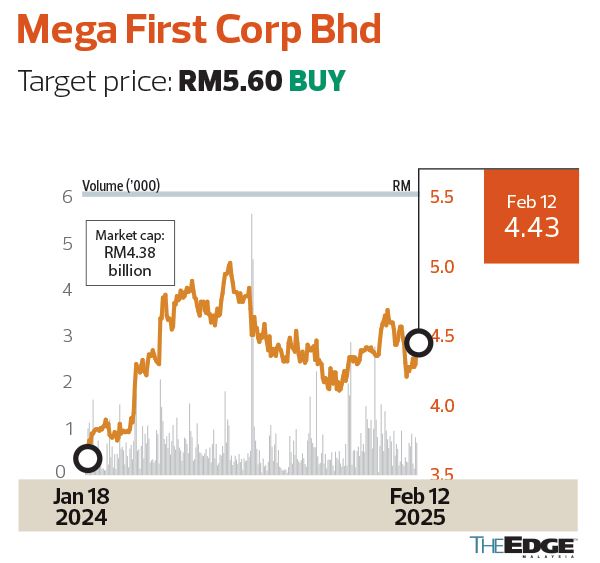

Mega First Corp Bhd

Target price: RM5.60 BUY

MAYBANK INVESTMENT BANK (FEB 10): With Mega First Corp Bhd’s (KL:MFCB) share price having corrected by about 7% year to date, we believe investors have yet to appreciate the potential accretion from Don Sahong’s revised concession terms. We reiterate “buy” with a higher target price of RM5.60 (+17%), as we incorporate the revised concession terms. There remains ample balance sheet headroom for new projects in our view.

The revised concession to incorporate the fifth turbine takes effect on Jan 1 and extends the concession tenure by more than four years. Despite a slight initial reduction in tariff (to six US cents per kWh), the upfront payment of the royalty (US$82.5 million for 2,140 GWh of annual generation, implied Internal Rate of Return of about 13%) both accretes and smoothens Don Sahong’s earnings profile over the concession tenure of 25 years in total.

Don Sahong has entered into its dry season (December to May). Despite various headlines on possible dryer-than-expected weather along the Mekong River, the water level at Don Sahong has so far remained similar to 2024 (Don Sahong’s availability was 79% in 1Q24), and comfortably above the historical minimum.

Kelington Group Bhd

Target price: RM4.12 BUY

RHB INVESTMENT BANK (FEB 10): Reiterate “buy” and RM4.12 target price, 20% upside and 2% FY25 yield. We see a strong start to the year for Kelington Group Bhd (KL:KGB) with a tender book at over RM2 billion, continuing strong off-takes at its liquid carbon dioxide plant and robust growth of its ultra-high purity (UHP) segment. Order wins in FY24 should surpass FY23, with FY25 likely to be another formidable year. Stock valuation is undemanding at 20 times FY25 EPS, supported by strong earnings execution, balance sheet strength and return on equity of over 30%.

We see a seasonally stronger 4Q24 with FY24 Patami likely up 20%-30% y-o-y to a record high. Management’s focus on profitability alongside the shift in product mix (higher-margin UHP jobs and the ramp-up in the industrial gas business) should see net profit margin improving to 8%-9% in FY24 compared with 6.5% in FY23. With a healthy order book estimated at more than RM1 billion at end-December 2024 and more than RM2 billion in tender book, 2025 is shaping up to be another stellar year.

Save by subscribing to us for your print and/or digital copy.

P/S: The Edge is also available on Apple's App Store and Android's Google Play.

- Gas pipeline blaze: MIDF flags potential RM18m impact to Petronas Gas

- Gas pipeline blaze: Petronas Gas, Gas Malaysia’s shares open marginally lower after trading halt

- T7 Global drops to two-year low, triggers short-selling halt after deputy chairman's departure

- Digital banks in Malaysia urged to re-examine strategies to better serve B40 segment

- Yinson's shares slip, analysts tell investors to look past underwhelming results

- CIMB, Bank Islam, Etiqa to assist Putra Heights fire incident victims

- China curtails more renewables as record additions stress grid

- US tariffs expected to affect Asia Pacific economic growth – S&P Global

- SC Annual Report 2024: SC swings to RM20.7 mil operating surplus, recovering from largest deficit in a decade in 2023

- SC Annual Report 2024: Malaysia’s capital market outperforms regional peers, funds raised hit RM138.9 bil in 2024