Muazzam: We’re looking at [the Ar-Rahnu business] to be at least 5% of our total retail portfolio within the next few years. (Photo by Suhaimi Yusuf/The Edge)

This article first appeared in The Edge Malaysia Weekly on February 17, 2025 - February 23, 2025

BANK Islam Malaysia Bhd (KL:BIMB), the country’s largest standalone Islamic banking group, sees Islamic pawnbroking as a burgeoning area of growth and is moving swiftly to expand this high-yield business.

According to CEO Datuk Mohd Muazzam Mohamed, the group has been operating its Ar-Rahnu — or Islamic pawnbroking — business for many years via standalone outlets. Noticing growing demand for it, however, the group changed its business model, deciding instead to offer Ar-Rahnu through Bank Islam branches.

“Last year, we managed to put Ar-Rahnu service counters in about 50 of our branches and, this year, we’ll do another 50, and it will keep expanding. I think we’ll have about 100 of our 135 branches offering Ar-Rahnu by year’s end,” he tells The Edge in an interview.

Ar-Rahnu is a type of short-term financing that enables borrowers to receive funds by using their gold or gold jewellery as collateral.

“We saw it as an opportunity to provide financing to micro businesses as well. Some of them, when they need capital, pawn [their gold] to get cash to do business. Once their business generates money, they can redeem [the gold]. So, we saw that we were able to assist in that market.

“At the same time, from a financial perspective, the margins are good,” Muazzam says, when asked why Bank Islam was deepening its focus on Ar-Rahnu. The margins are better than those of personal financing, he adds without elaborating.

CGS International notes that the yield in Islamic pawnbroking is among the highest of all types of financing.

The research house says in a Jan 20 report: “We are positive on Bank Islam’s drive to grow its Ar-Rahnu financing given: (1) its high lending yield of more than 15% per year (based on management’s commentary that the yield is close to those of credit cards, which are 15% to 17%, and widely advertised rates of 1.5% to 2% per month for the pawnbroking industry); (2) minimal credit losses, as it is fully secured against gold/jewellery; and (3) sustained demand for this financing from lower-income borrowers.”

In the event of a default, Bank Islam can sell off the jewellery or gold within a short period of time. This compares favourably to the long foreclosure period for other types of impaired financing, especially house financing, CGS International notes.

According to Muazzam, the credit loss in Bank Islam’s Ar-Rahnu business is “almost zero”. “The risk in Ar-Rahnu is fake gold. There used to be such cases previously, but we improved over time, making sure we have proper valuers to determine the authenticity [of the gold], controlling safekeeping and so on.”

Credit loss is minimal in the event of a default — unless there is a sudden significant drop in gold price that extends for a long period of time, he points out.

For the nine months of the financial year ended Dec 31, 2024 (9MFY2024), Bank Islam’s Ar-Rahnu financing increased to RM193.94 million from RM162.21 million in the same period the year before. In FY2020, it stood at just RM5.48 million.

The business, though growing fast, accounts for a relatively small portion of Bank Islam’s financing portfolio. In 9MFY2024, it accounted for just 0.3% of the group’s total gross financing of RM68.46 billion. House financing (41% of total financing) and personal financing (31%) are still its biggest businesses.

Given that Bank Islam is still building up the Ar-Rahnu business, it will take several years before it grows in significance in the group’s financing portfolio. “We’re looking at it to be at least 5% of our total retail portfolio within the next few years,” Muazzam says. It was just 0.37% of the retail portfolio as at end-September last year.

Bank Islam’s focus on Ar-Rahnu is expected to help boost its net income margin (NIM) — the Islamic equivalent of net interest margin — over the long run.

“As the yield of Ar-Rahnu financing is one of the highest among all financing types, growing this segment will help improve Bank Islam’s overall NIM in the longer term. Nevertheless, Bank Islam will have to incur additional operating costs for the Ar-Rahnu business,” says CGS International, which has an “add” call on the bank’s stock. Profitability should increase over time as the business grows, it adds.

Stabilising margins

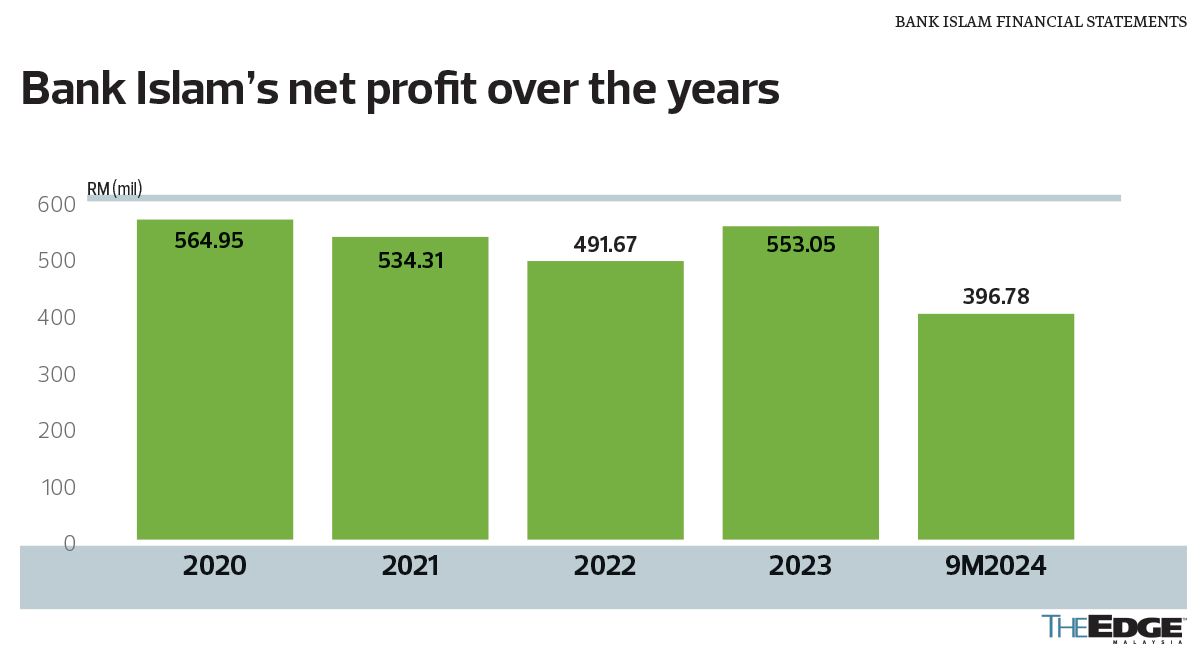

In 9MFY2024, Bank Islam’s net profit grew 0.5% year on year to RM396.78 million. The group will announce its full-year earnings by the end of this month.

CGS International sees its net profit coming in at RM566.1 million for the full year compared with RM553.1 million in FY2023.

There will be much interest in how Bank Islam’s NIM fared in the final quarter, given the seasonally strong competition for deposits in the industry towards the end of the year. Like most lenders, the bank has focused on managing funding costs better over the last two years amid NIM compression, as a result of higher deposit costs.

To its credit, its NIM in 9MFY2024 improved by four basis points to 2.15%, from 2.11% in the same period a year earlier. NIM is seen stabilising this year, Muazzam says.

To prop up income, the group, like many other lenders, is seeking to grow fee-based income by continuing to focus strongly on its wealth management business this year.

“We’ll convert more branches into Premier Wealth Centres. We aim to have six centres by the end of 2025. Bank Islam has always been strong in the mass market segment, and we want to grow the high-net-worth segment more; so, investments are required to serve those customers better,” says Muazzam. The group will broaden its wealth product portfolio, including by onboarding more partners in this space.

Bank Islam guided analysts that financing growth in FY2024 would come in around 4%, owing to high corporate repayments, as some corporates refinanced their bank loans with fixed-income securities to take advantage of lower interest rates in the bond market. This development is unlikely, however, to recur this year.

Muazzam tells The Edge that the group is targeting financing growth of 7% to 8% in FY2025. It is aiming for a net return on equity (ROE) of 8%. As at 9MFY2024, net ROE was 7%.

Meanwhile, Bank Negara Malaysia’s proposed abolishment of the “Rule of 78” financing method on personal financing is expected to have only a minimal impact on Bank Islam, he says, as a substantial portion of its personal financing is on floating rates. The Rule of 78 method is used by lenders to calculate a loan’s interest for the entire loan term based on the original principal. A borrower thus gets no interest savings even if the loan is paid off earlier than scheduled.

Interestingly, there was “good growth” in its personal financing disbursement last December, which was also the month civil servants received a salary hike, Muazzam says.

The group has no plan to undertake mergers and acquisitions and will focus entirely on growing organically, he adds.

Bloomberg data shows that of the nine analysts that track the stock, five have a “hold” call on the stock, three have a “buy” and one, a “sell”. The average 12-month target price was RM2.74. The stock closed at RM2.52 on Feb 13, giving the lender a market value of RM5.72 billion.

Save by subscribing to us for your print and/or digital copy.

P/S: The Edge is also available on Apple's App Store and Android's Google Play.

- Anwar receives courtesy visit from tech giant Oracle, discusses AI and digital innovation

- Singapore man accused of Nvidia chip fraud wields global connections

- Stocks extend drop, dollar falls on tariff woes

- Trump’s manufacturing dreams clash with business owners’ reality

- Chinese tea chain Chagee launches US IPO defying stock slump

- Margma makes urgent appeal for affordable alternative gas supply amid disruption

- China's Xi to visit Southeast Asia as trade conflict with US widens

- Several districts in Selangor hit by flash flood

- Chinese tea chain Chagee launches US IPO defying stock slump

- Country Garden secures key bondholder group support for offshore debt overhaul