This article first appeared in The Edge Malaysia Weekly on February 17, 2025 - February 23, 2025

APART from sweating their existing assets, real estate investment trust (REIT) players have been actively undertaking inorganic growth to expand the value of their portfolios. Analysts expect the healthy deal pipeline to continue as firms pursue their own business strategies, with the retail and hospitality segments being of particular interest given Visit Malaysia Year 2026 is less than 11 months away.

Despite the current weak market sentiment, REITs have demonstrated their defensive nature, being the only sector to record a positive return since the start of the year, albeit a modest 1.3% gain.

An analyst who declined to be named observes that the sector has seen more transactions in the recent months following the global economic recovery and reopening of borders. These acquisitions are within the respective companies’ guidance and market expectations.

“So far, investors are quite comfortable with the asset yield from these acquisitions. However, it is still dependent on the REITs’ ability to source for earnings-accretive acquisitions,” he tells The Edge.

“We see that businesses have recovered, with more industrial output. So businesses, including retailers, are trying to expand, and they are asking for more space in the retail malls. For the manufacturing segment, industrial players are expanding further into the factory and warehouse space.”

While acquisitions are likely to continue, he believes industrial asset acquisitions may not be as aggressive as before as the prices of industrial assets have gone up a fair bit.

“If you look at the trend, the asset yield has been coming off a little bit for industrial assets … Acquisitions in this segment may not be so frequent this year, but we don’t discount [the possibility] that industrial REIT players will still continue to expand their portfolio.”

Nonetheless, he foresees sustained momentum for retail assets.

“Demand for retail assets is still quite strong. In terms of supply, we don’t foresee a lot of retail malls coming in this and next year in particular. Overall, retail business is still quite healthy and we expect it to be quite stable,” he adds.

RHB Research analyst Loong Kok Wen says the local business environment — with a stable interest rate outlook, better economic growth and political stability — remains conducive for REITs to pursue inorganic growth.

“Although the Trump administration will add some uncertainty to the market, I think the local interest rate direction will likely be stable,” she says.

As US inflation beat expectations in January, this could diminish chances of the US Federal Reserve cutting interest rates anytime soon.

Loong says Visit Malaysia Year 2026 will be another catalyst, benefiting the retail and hospitality segments. The industrial segment is also seen as a bright spot as businesses have been relocating their production base to Southeast Asia in recent years as a result of the US-China trade war.

“The availability of resources in Malaysia has [made it] a good destination for all these industrial players, though the yields for industrial properties have come down as valuations are getting higher.

“There are still opportunities as long as the REIT players see growth potential, with the ability to squeeze better value after the asset acquisition,” she adds.

Looking ahead, the first analyst is more bullish on REITs with exposure to the retail and hospitality segments because tourist arrivals are expected to remain robust in 2025 and 2026. He has “buy” calls on both Sunway REIT (KL:SUNREIT) and Pavilion REIT (KL:PAVREIT).

In a Feb 13 note, Kenanga Research analyst Chris Tong maintained his “outperform” call on Pavilion REIT with a target price of RM1.63, although its FY2025 earnings forecast has been trimmed by 6% to adjust for lower contributions arising from a more competitive landscape.

“Pavilion REIT’s FY2024 results disappointed despite a full-year net profit growth of 9%, driven largely by contribution from new asset Pavilion Bukit Jalil and positive rental reversions. Property income growth from Pavilion KL fell below our expectations, coupled with higher operating expenses incurred during the year,” Tong says.

Pavilion REIT’s net property income was flat year on year at RM134.86 million in 4QFY2024, but rose 14% y-o-y to RM522.77 million for FY2024.

It is worth noting that Tong recently downgraded his REIT sector call to “neutral” from “overweight” after the share price of some big-cap stocks such as KLCC Stapled Group (KL:KLCC) and Sunway REIT gained 3% to 12% over the past three months.

For the industrial segment, he cautions about the new incoming supply of assets, which could exert pressure on rentals and future rental reversion rates.

Loong is of the view that the retail REIT segment will be supported by resilient domestic spending, albeit with inflationary pressure, while the industrial segment will continue to be in a good position to reap the benefits of rising foreign direct investments into the country.

Loong’s top picks for the sector are Axis REIT (KL:AXREIT) and Sunway REIT. Axis REIT is a proxy for the stable industrial segment, while Sunway REIT has solid growth prospects from its diversified portfolio, as well as upside from its active acquisition strategy and asset enhancement initiatives.

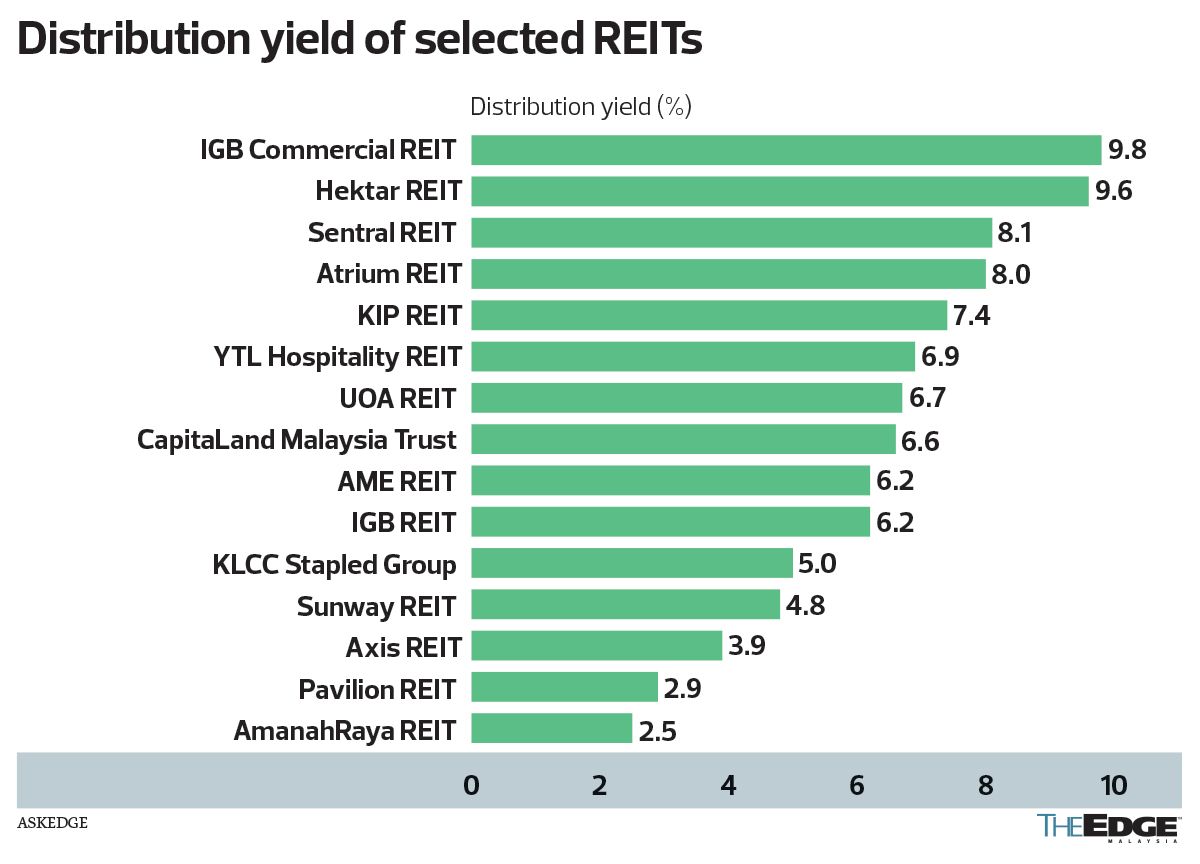

Most Bursa Malaysia-listed REITs offer distribution yields of above 5%, based on dividends that have gone ex in the past 12 months. AskEdge data shows that IGB Commercial REIT (KL:IGBCR) has the highest distribution yield of 9.8%, followed by Hektar REIT (KL:HEKTAR), Sentral REIT (KL:SENTRAL) and Atrium REIT (KL:ATRIUM) at 9.6%, 8.1% and 8% respectively.

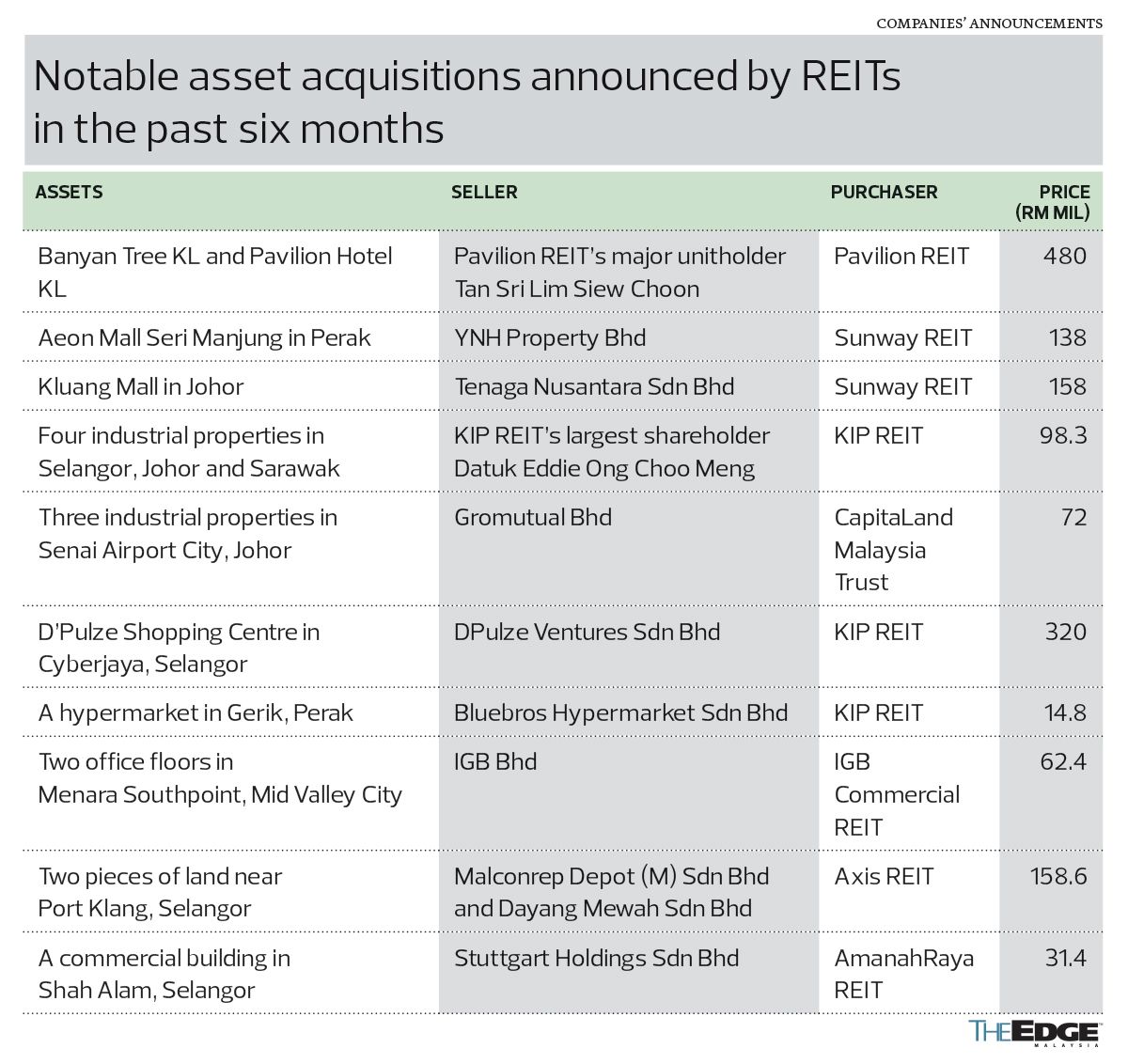

Notable deals in the REIT sector in recent months include Pavilion REIT’s proposal to acquire two hotels, Banyan Tree KL and Pavilion Hotel KL, for RM140 million and RM340 million respectively. The sellers are Lumayan Indah Sdn Bhd and Harmoni Perkasa Sdn Bhd, which are indirectly wholly owned by Pavilion REIT’s major unitholder Tan Sri Lim Siew Choon. As such, the deals are deemed related-party transactions.

Pavilion REIT is planning to fund the two acquisitions via a private placement that could raise up to RM552 million.

Following the completion of the purchase of Kluang Mall in Johor for RM158 million, which is expected to provide an initial net property income yield of 7%, Sunway REIT recently announced that it is acquiring AEON Mall Seri Manjung in Perak from YNH Property Bhd (KL:YNHPROP) for RM138 million.

The two-storey shopping centre will then be leased to supermarket chain operator AEON Co (M) Bhd (KL:AEON). The lease will last for another 13 years until Dec 3, 2037.The initial net property income yield is estimated to be 6.5%, with a higher 7% average yield over AEON’s remaining tenure on its lease.

Late last year, KIP REIT (KL:KIPREIT) completed the RM320 million acquisition of D’Pulze Shopping Centre in Cyberjaya, Selangor. In order to achieve RM2 billion of assets under management from about RM1.5 billion currently, the REIT is aiming to aquire more retail and industrial assets.

Meanwhile, CapitaLand Malaysia Trust (KL:CLMT) is making its second foray into the industrial sector in Johor with the purchase of three industrial properties in Senai Airport City for RM72 million. This will, in turn, significantly increase the proportion of logistics and industrial assets to 7.9%, from 2.8%, of its total portfolio under management.

Axis REIT, which spent RM719.4 million to acquire eight new assets last year, remains on the lookout for acquisition targets, particularly industrial properties.

Nonetheless, not all proposed deals materialised. AmanahRaya REIT (KL:ARREIT), for example, scrapped its plan to sell the Contraves building in Cyberjaya for RM42.5 million due to a failed condition precedent. It said the purchaser, 4X Software Sdn Bhd, was unable to fulfil the stipulated condition precedent within the agreed timeline.

Save by subscribing to us for your print and/or digital copy.

P/S: The Edge is also available on Apple's App Store and Android's Google Play.

- Mr DIY founder Tan Yu Yeh relinquishes vice chairman post, to serve as adviser

- 50,000 Malaysian jobs at risk, business chamber warns as it calls for urgent US tariff mitigation council

- Malaysia refutes 47% US import tariff claim, takes measures to prioritise well-being of businesses and people

- Trump hits China tariff retaliation, says policy will remain

- China retaliation on US farm goods hits soybeans, bolstering Brazil

- ‘Worst-case scenario’ for tech wipes $1.4 trillion from Nasdaq

- Anwar says impact of latest US tariff on nation's economy still being assessed

- Tok Mat, Rubio discuss bilateral relations, Asean-US Special Summit date

- US solar’s hoarding habit will help blunt sting from Trump tariffs

- Wall Street rout drags Nasdaq near bear market