This article first appeared in Forum, The Edge Malaysia Weekly on February 17, 2025 - February 23, 2025

President Donald Trump has since his first presidential term cultivated an image of unpredictability — a quality he proudly touts as a strategic advantage. This penchant for sudden policy shifts is not only emblematic of his style but also a source of persistent uncertainty that domestic and global policymakers will have to deal with over the next four years.

For those at the US Federal Reserve, this volatility poses a formidable challenge. Thus, rather than wait for a definitive signal from an administration that can change direction on a dime, the Fed should adopt a more proactive stance than in the past. Inaction now risks leaving the central bank unprepared, while timely moves could provide critical flexibility if economic conditions deteriorate.

A cornerstone of Trump’s second-term agenda has been import tariffs. While it is a policy tool often framed as protecting American industries, it carries unpredictable and consequential risks for the US and global economy alike. Yet, beyond debates on trade flows and export competitiveness lies an equally consequential chain reaction. Tariffs can also trigger a chain reaction that can stoke inflation, disrupt the delicate balance of US monetary policy and send shock waves through global financial markets.

As the adage goes, uncertainty is never good for business. For economists and policymakers, unpredictable shifts complicate both forecasting and the formulation of effective policy responses. The recent delay in implementing planned tariffs on Canadian and Mexican imports — just days after their initial announcement — illustrates that even when concrete measures are rolled out, the underlying uncertainties persist. Trump’s habit of announcing sweeping changes and then abruptly modifying them forces market participants and policymakers into a constant state of flux.

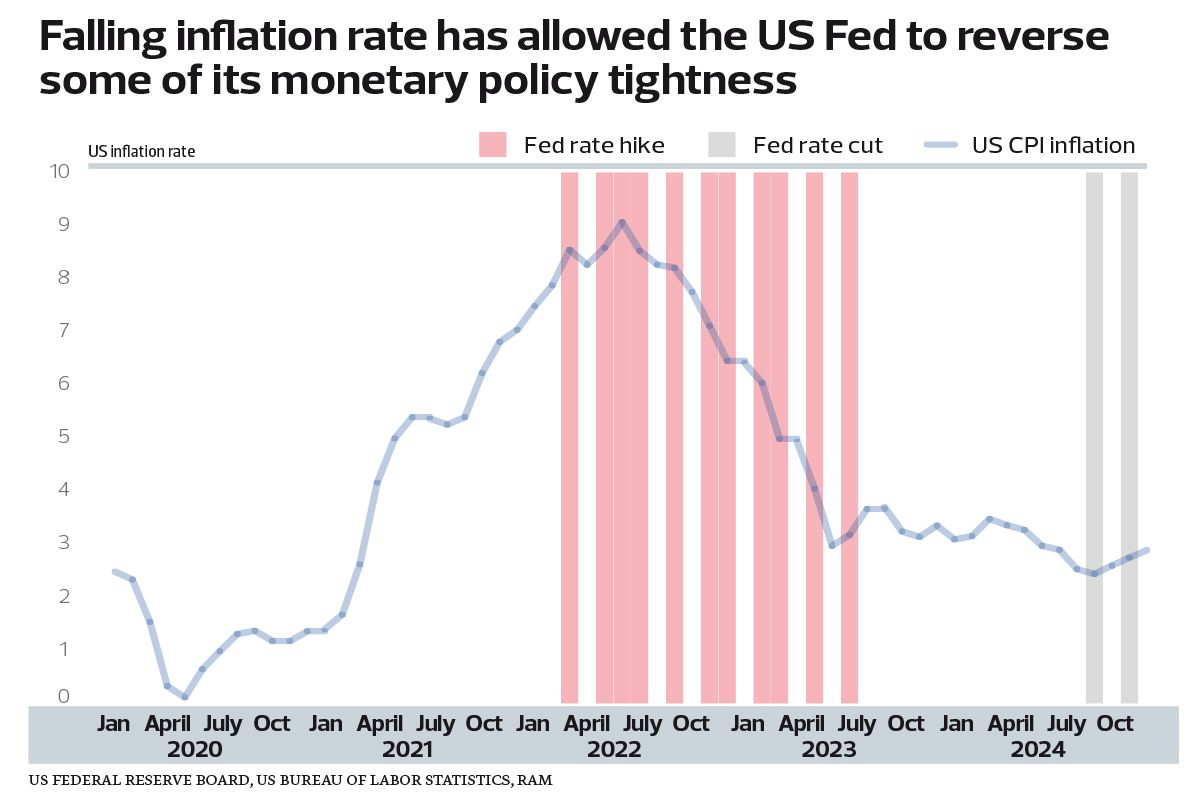

This uncertainty threatens the Fed’s ongoing efforts to combat inflation. After a series of aggressive interest rate hikes designed to rein in surging prices, US inflation had begun to moderate. The US inflation rate has fallen to an average of 3% in 2024, down from 4.1% one year ago and 8% two years ago. This allowed the Fed to begin normalising interest rates, with a cumulative 100 basis points’ (bps) worth of policy rate reduction last year.

However, the spectre of tariffs and the inflationary pressure they bring made the Fed increasingly cautious, prompting it to contemplate slowing down or even pausing in its current rate cut cycle. Tariffs essentially raise the cost of imported inputs, which inevitably will be passed on to consumers. Indeed, the Fed’s latest dot-plot projection released in December 2024 indicates only two 25bps cuts by the end of 2025, fewer than the four cuts from the previous projection in September 2024.

Admittedly, waiting for a more definitive policy signal might seem appealing or prudent, but delaying policy action comes with its own risks, especially given how erratic things have been in the past. A sluggish response, especially given concern surrounding a slowing US economy, could put the economy in a precarious position and might ultimately force its hand to enact a reactive, potentially disruptive policy adjustment later on.

A proactive approach — such as proceeding with the original plans of a modest rate cut now — could serve as a pre-emptive measure to shore up economic momentum. This “cut now, raise later” strategy will also allow the Fed to retain the flexibility to implement larger hikes in the future if inflation surges. Waiting for perfect clarity in Trump’s erratic policy signals may lead to missed opportunities and a suboptimal policy stance that could undermine long-term growth. Of course, there is a trade-off, as such pre-emptive cuts might introduce additional volatility in interest rates and financial markets. Yet, given the alternative, the risk of inaction has the potential to introduce a bigger cost to the economy in the longer run.

Another complicating factor is the potential influence of fiscal policy. While Trump’s proposed tax cuts act as a form of fiscal stimulus, his promise to trim federal spending through initiatives such as the Department of Government Efficiency could dampen economic support.

Ultimately, the challenge for the Fed in this Trump era is to strike a delicate balance between caution and decisiveness. While waiting for a stable policy environment might seem like a safer course, the risks of inaction, especially in the face of potential stagflation, are too high. The Fed is caught between a rock and a hard place, and its policy choices have far-reaching implications not only for the US economy but also for global markets. I certainly do not envy the Fed’s position.

For me, as a market observer, the path to sustainable economic growth must hinge on strengthening domestic fundamentals and pursuing smart, data-driven policies rather than relying on reactive measures to unpredictable political theatrics. The long game is not won by imposing tariffs that temporarily protect domestic industries, but by investing in robust infrastructure, a skilled workforce and an environment that naturally attracts investment and innovation. Only then can the Fed focus on steering the US economy towards enduring prosperity, as opposed to having to deal with the roller coaster of political uncertainty.

Woon Khai Jhek, CFA is a senior economist and head of the Economic Research Department at RAM Rating Services Bhd

Save by subscribing to us for your print and/or digital copy.

P/S: The Edge is also available on Apple's App Store and Android's Google Play.

- Malaysia hit with 24% US reciprocal tariff effective April 9

- Malaysia won’t retaliate, will negotiate with US on tariffs — Miti

- Apple production hubs, including Malaysia, hit by tariffs

- Glovemakers rebound as investors see competitive advantages

- Trump’s tariffs on Asean: Nothing to dread, everything to fear

- Tiny Australian outposts, including some with no people, targeted by Trump tariffs

- China detains three Filipinos for alleged spying as ties fray

- Trump signs order ending 'de minimis' duty-free treatment for low-value parcels from China

- Trump tariffs are ‘disaster’ for the world’s poorest countries

- Israel to formulate 'necessary steps' in response to US tariffs, finance minister says