Photo by Sam Fong/The Edge

KUALA LUMPUR (Feb 13): CelcomDigi Bhd (KL:CDB) said on Thursday its net profit fell nearly 64% in the final quarter of 2024 from a year earlier, primarily due to higher depreciation and impairment charges.

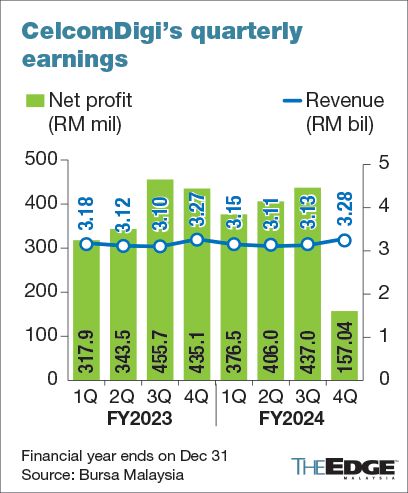

Net profit for the three months ended Dec 31, 2024, was RM157.04 million, down 63.9% year-on-year (y-o-y) from RM435.15 million in the same period in 2023, according to an exchange filing on Thursday.

The mobile network operator booked an impairment charge of RM217.2 million, while revenue for the quarter was barely higher at RM3.28 billion, a marginal 0.03% increase y-o-y.

The decline in earnings was mainly due to the impairment and accelerated depreciation charges of right-of-use (ROU) assets for network sites, following a reassessment of their useful life. This was partially offset by a reversal of tax over-provisions.

For the full financial year (FY2024), CelcomDigi reported a net profit of RM1.38 billion, down 11.3% from RM1.55 billion in FY2023. Annual revenue was unchanged at RM12.68 billion.

Service revenue — which excludes sales of devices and other income — fell 0.6% to RM10.79 billion in line with its revised full-year guidance. Earnings before interest and tax (EBIT) dropped 13.4% to RM2.33 billion, sharper than the company's guidance of a "single digit decrease".

CelcomDigi also slightly overshot its capital expenditure intensity guidance of around 15% - 18%, ending the year with spending of RM2.37 billion or 18.71% of revenue.

Total costs rose 5.7% y-o-y, primarily due to higher roaming traffic and device sales, along with increased lease line and fibre-related expenses to support traffic and home and fibre growth. Earnings before interest, tax, depreciation, and amortisation (EBITDA) margin fell to 45.7% from 48.5% in FY2023.

The company declared a fourth interim dividend of 3.7 sen per share, payable on March 27, 2025. This brings total dividends for FY2024 to 14.3 sen per share, up from 13.2 sen in FY2023.

As at end-FY2024, CelcomDigi’s total subscriber base stood at 20.39 million, a 0.8% decline y-o-y. The postpaid segment grew 1.3%, while prepaid revenue declined, impacted by a shift away from one-time SIM acquisitions and SIM consolidation post-merger.

The home and fibre segment saw strong growth, with revenue up 28.4% y-o-y and total subscribers reaching 209,000, up 78,000 from 2023.

Guides for modest growth in FY2025

For 2025, the company is guiding for “low single-digit growth” in service revenue — which excludes sales of device and other income — as well as “low to mid single-digit” EBIT growth.

The company remains focused on network integration and cost optimisation post-merger with 5G network implementation, regulatory developments and rising infrastructure costs as key challenges.

"Looking ahead, with a solid foundation in place, we continue to focus on strengthening market leadership across our lines of business, creating pathways for long-term profitable growth. We will focus on delivering more value to our customers through product innovation and digital value-added services," CelcomDigi chief executive officer Datuk Idham Nawawi said in a separate statement.

"We will drive operational excellence through cost structure optimisation and robust operating models to be one of the most efficient operators in the world. We continue to invest for the future as we bring innovation and new AI-driven capabilities to the market, while we redefine digital services and customer journeys," he added.

CelcomDigi shares closed six sen or 1.5% lower on Thursday at RM3.87, valuing the group at RM45.4 billion.

- Xi's showdown with Li Ka-shing threatens China’s pro-business push

- Tan Kean Soon steps down as T7 Global executive deputy chairman, board says no operational impact

- Company auditor loses RM1.29m to investment scam

- Huawei posts surprise loss after aggressive tech research

- Perak emerges as Malaysia's No 1 sweet corn producer