This article first appeared in Capital, The Edge Malaysia Weekly on February 10, 2025 - February 16, 2025

Malaysian automotive sector

Neutral (unchanged)

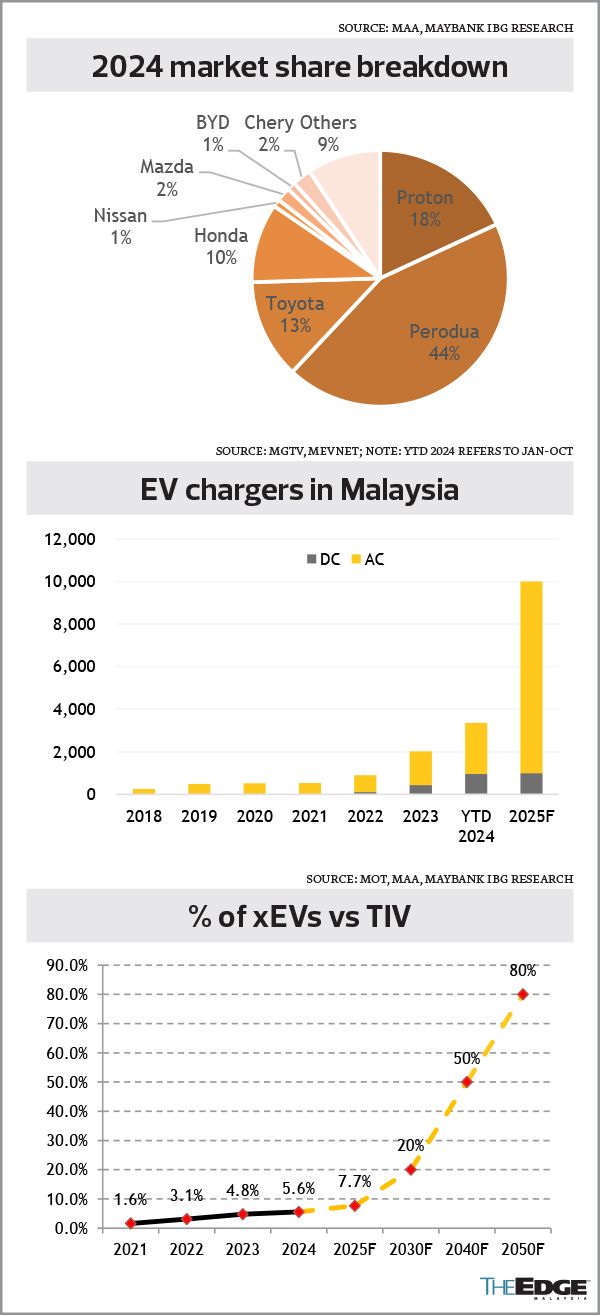

Maybank Investment Bank (Feb 4): We raise our total industry volume (TIV) forecast by 5% to 790,000 units (from 750,000) versus 2024’s record high of 816,747 units (+2% y-o-y). In 2024, growth was largely driven by Perodua (+8% y-o-y, 358,102 units), Honda (+2% y-o-y, 81,699 units), and new entrants like Chery and BYD (growth more than doubled).

Our new 2025 forecast assumes sustained mass-market growth, offset by weakness in the premium/luxury segment, with a positive catalyst (versus our previous assumption) from another year of open market value (OMV) deferment.

We project battery-powered electric vehicle and hybrid EV adoption to reach 3%/5% in 2025 (compared with 2%/4% in 2024), driven by new model launches and aggressive pricing, especially from completely built-up brands rushing to sell before the EV CBU incentives expire.

As of October 2024, only 3,354 EV chargers were installed, far below the 10,000 unit target for 2025. Meeting this goal requires 554 new chargers to be installed per month, compared with 2024’s average of about 111 per month.

Sime’s positive outlook is supported by UMW’s contribution, which provides resilience against challenges in its industrial and motor segments, particularly in China.

BAuto’s sales contraction for Mazda and Kia has stabilised, with the launch of the Kia Sportage expected to drive growth. Its new distributorships for XPeng and Deepal strengthen its EV portfolio, positioning it to compete more effectively with other new Chinese marques in the Malaysian market.

The OMV excise duty revision, originally set for 2020, has been deferred multiple times, with the latest deadline of January 2025 now postponed to January 2026. If implemented, completely knocked down car prices could rise by 10%-30%, making locally assembled cars significantly more expensive.

Local auto parts players can capitalise on the EV transition through technical partnerships and upskilling to expand their customer base and access global supply chains, while traditional auto parts suppliers risk losing out. We see MCE Holdings Bhd (KL:MCEHLDG) as a proxy for EV component supply, while Sime’s diversified portfolio positions it well to navigate the transition and seize consolidation opportunities.

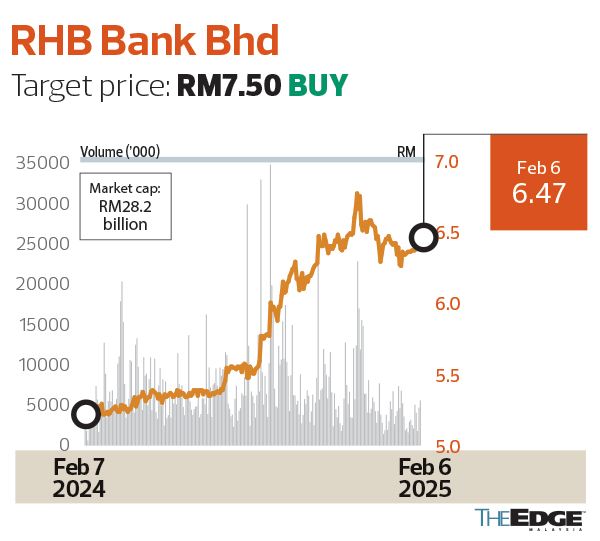

RHB Bank Bhd

Target price: RM7.50 Buy

Phillip Capital (Feb 4): We expect RHB’s (KL:RHBBANK) net fund-based income in 4Q24 to hold up, supported by a higher loan base. Despite this, net interest margin (NIM) is expected to see a four- to five-basis-point (bps) q-o-q contraction, largely attributable to the delayed impact of US Fed Fund rate cuts on US dollar-denominated loans.

We anticipate RHB to recognise a one-off gain of RM50 million from the disposal of its Thailand brokerage business, partly offsetting weaker trading-related income. We believe RHB’s 4Q24 core Patami to be in line with our RM704 million estimates (+20% y-o-y, -16% q-o-q), bringing 2024E core net profit to about RM3 billion (+7% y-o-y). Headline NIM is expected to close at 1.88% (+6bps y-o-y), at the higher end of management’s guidance of 1.82%–1.88%. We expect RHB to declare a DPS of 27 sen in 4Q24, bringing the full-year 2024 DPS to 42 sen, implying a 60% payout ratio (2023: 61%).

We continue to like RHB for its undemanding valuations (0.86 times 2025E P/B with 10% return on equity) and a sector-high dividend yield of about 7%.

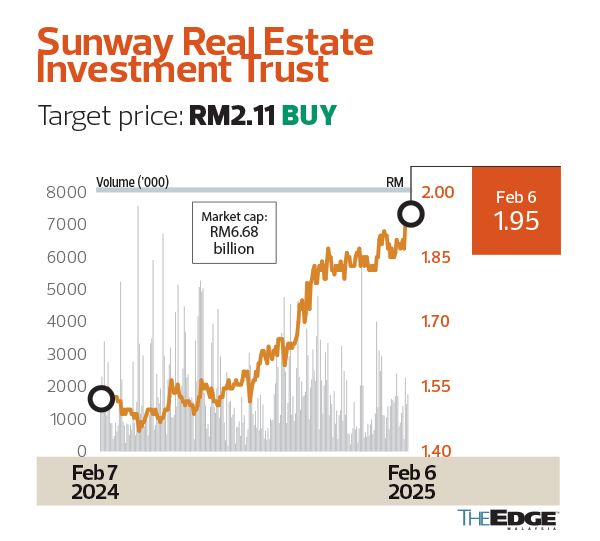

Sunway Real Estate Investment Trust

Target price: RM2.11 Buy

CIMB Securities (Feb 4): Sunway Real Estate Investment Trust (KL:SUNREIT) reported a core net profit of RM343.8 million for FY24, which is in line with expectations.

SunREIT declared a distribution per unit (DPU) of 5.3 sen for 2H24 (1H24: 4.66 sen). This brings its full-year DPU to a record-high 10 sen, meeting 102% of our and 103% of consensus full-year projections. SunREIT’s FY24 net property income (NPI) grew 8.5% y-o-y. Excluding the impact from new acquisitions in FY24, SunREIT’s NPI grew 1.3% y-o-y, attributable to healthy rental reversion and the completion of refurbishment activities.

SunREIT started 2025 with the announcement of its AEON Mall Seri Manjung acquisition on Jan 21, 2025; this could lift our FY25/FY26F earnings projections by 0.3%–0.7%. We view the acquisition positively owing to its fair purchase consideration (4.8% below market value) and the resulting expansion and diversification of SunREIT’s earnings base.

We expect the company’s FY25 earnings to grow by 11.6% y-o-y. We retain our “buy” call on SunREIT with a higher DDM-based target price of RM2.11 (from RM2.09) as we raise our FY25/FY26F earnings estimates by 0.9%–1.8% following the completion of the Sunway Kluang Mall acquisition.

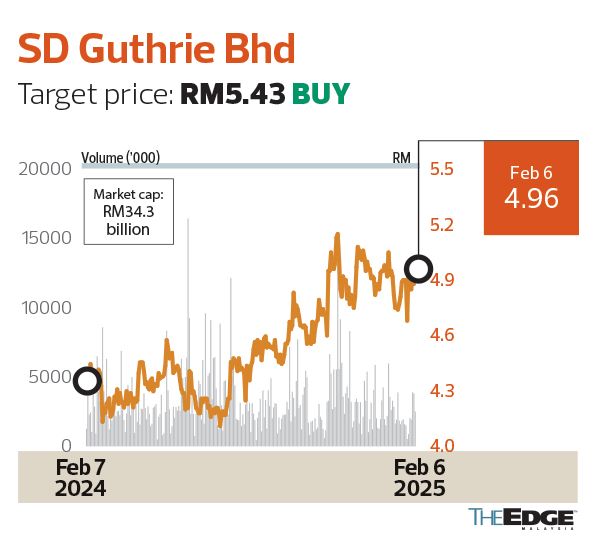

SD Guthrie Bhd

Target price: RM5.43

MIDF (Feb 4): SD Guthrie’s (KL:SDG) downstream arm, SD Guthrie International Ltd (SDGI), has announced the acquisition of a 48% stake in Marvesa Supply Chain Services BV for about RM250 million. SDG remains committed to expanding its presence in the EU, positioning it as one of the key hubs for both companies to pursue growth opportunities.

This makes Marvesa an ideal partner to serve customers from its Zwijndrecht refinery in the Netherlands, which has an annual capacity of 300,000 tonnes. Additionally, the collaboration stands to benefit SDGI in terms of trading volumes in lecithin, soy and other soft oils, aligned with SDGI’s diversification strategy into non-palm sectors.

In addition to its unique product offerings, Marvesa’s refinery continues to produce a traditional range of oils and fats used in industrial frying, emulsifiers, bakery and confectionery ingredients, margarines, dairy products, candles and milk substitutes, meeting the evolving needs of the market.

Currently, with a healthy balance in hand, about 24% or 0.24 times in 9MFY24, SDG is on a stronger footing to embark on any business expansion. Assuming the acquisition was funded through term-loans, net gearing is expected to increase 0.25 times or 25%, a +5% increase, which we believe is still within the average sector’s net gearing of 19-25 times.

Save by subscribing to us for your print and/or digital copy.

P/S: The Edge is also available on Apple's App Store and Android's Google Play.

- Subang’s turbulence: Malaysia’s airport expansion faces market realities

- Intel jumps 10%, as investors cheer appointment of new Malaysian-born CEO Tan

- UWC's 2Q net profit more than doubles on semiconductor industry's strong recovery

- Apollo Food 3Q net profit drops 66% on lower margin, absence of one-off gains

- Trump threatens 200% wine tariff if EU does not relent on whiskey

- Stock turmoil spreads as fear hits the world of corporate bonds

- Putin backs US ceasefire idea for Ukraine, but says many details need to be sorted out

- Democrats in standoff with GOP as US shutdown deadline nears

- Vocational college murder case: Third accused says did not see victim steal money

- Anglo American plans fresh job cuts at corporate office under restructuring