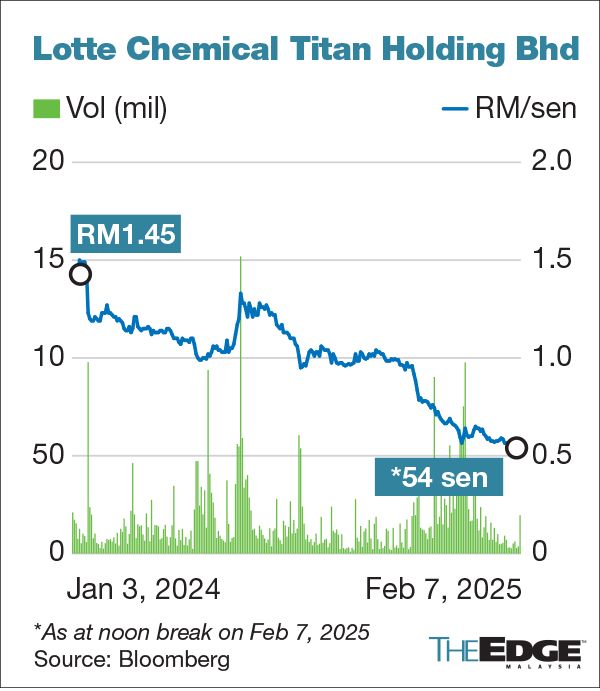

KUALA LUMPUR (Feb 7): Shares of Lotte Chemical Titan Holding Bhd’s (KL:LCTITAN) fell on Friday to a new record-low after the petrochemical company reported its largest quarterly loss.

Lotte Chemical fell by four sen or 7% to close at 53.5 sen on Friday, marking a new low since its listing nearly eight years ago. At the last price, the company has a market capitalization of RM1.24 billion. The counter saw some 2.48 million changed hands for the day.

Analysts at Maybank Investment Bank (Maybank IB) have cautioned that the petrochemical company will likely stay in the red for the foreseeable future, widening their FY2025-FY2026 earnings forecasts to net losses of RM 604 million and RM 712 million, respectively.

“We foresee Lotte Chemical Titan to still be in the red in 1Q2025 and for the rest of the year, as we view that the petrochemical cycle will remain muted over the next three years,” said Maybank IB in a note on Friday.

For the fourth quarter ended Dec 31, 2024 (4QFY2024), Lotte Chemical Titan’s net loss widened to RM510.07 million, from RM186.48 million a year earlier — marking the group’s largest quarterly net loss since its listing in 2017.

Meanwhile, revenue for the quarter fell 3.37% to RM1.79 billion from RM1.86 billion. Its loss before tax widened to RM645.1 million, from RM255.2 million.

According to Maybank IB, the group’s losses were exacerbated by weak polymer-naphtha spreads, which averaged US$330 per metric tonne (MT) in the fourth quarter of 2024. The downtrend has continued into 1Q2025, with spreads slipping further to USD300/MT as of early February.

However, in order for Lotte Chemical’s net profit to break even, analysts have estimated that the group requires spreads above US$500/MT, but this threshold remains out of reach due to depressed polymer prices and sustained high naphtha costs.

Despite cost-saving measures — including a reversal of royalty expenses from its parent company Lotte Chemical Corp and a one-off RM 28 million payment from the termination of a pipeline lease — the company remains burdened by structural challenges.

Additionally, its operating rates have been trimmed to 52% for FY2025E (estimate), reflecting weak demand conditions.

In light of the persistent losses, Maybank IB slashed the group’s target price to 39 sen from 91 sen, while maintaining a “sell” call on the stock.

- China suppliers mock tariffs with Nike, Lululemon deals on TikTok

- Malaysia declares state funeral for Tun Abdullah Ahmad Badawi

- Reach Energy, Cahya Mata, Able Global, Pestec, Bina Puri, Jentayu Sustainables

- Yellen says sell-off in Treasuries shows US confidence loss, not dysfunction

- Nvidia to produce AI servers worth up to US$500b in US over four years