This article first appeared in The Edge Malaysia Weekly on February 3, 2025 - February 9, 2025

RETAILERS and consumer good players will be busy during the first four months of 2025, with the two major celebrations — Lunar New Year and Hari Raya Aldilfitri — only two months apart. These two major festivals in Malaysia are often seen as make-or-break for retailers, as they determine how the traders perform for the year.

The general sentiment is that retail sales will be strong for the first half (1H) of 2025, with the timing of the festivities being close together. The break for the end of the academic year at public schools, which will take place from the end of January to mid-February for a total of four weeks, will also fuel consumer spending momentum.

But after that, will spending power fizzle out as the second half of the year approaches?

In 2024, both major festivals were celebrated within a 2½-month space. Retailers experienced part of the pre-festive sales for Hari Raya Aldilfitri which happened in the second quarter (2Q) (from April 10, 2024), taking place in 1Q, reported Retail Group Malaysia (RGM). However, the festive sales were not encouraging and came below market expectations.

For 2Q2024, RGM reported that retail sales amounted to a meagre 0.6% growth year on year (y-o-y), compared with the 7.8% it saw in 1Q. It subsequently rebounded to a 3.8% y-o-y growth in 3Q, bringing the total retail sales growth for January to September 2024 to 3.8%.

However, the sector will face headwinds in 2H this year. With the petrol subsidy rationalisation expected to take place in mid-2025 and a revision of electricity tariffs slated to happen around the same period, it will inevitably result in higher inflationary pressure, translating into a higher cost of living. The key question is whether the consumer sector can continue to encourage spending as purse strings tighten.

Fortress Capital Group CEO Datuk Thomas Yong says he is expecting to see a surge in spending on consumer goods, travel and hospitality in the first half of 2025 as consumers front-load.

“However, this could indeed lead to a lull in the second half as consumers adjust their budgets post-festivities due to holiday spending fatigue, increased utility costs and possible fuel price adjustments,” he says.

While some take the view that a lull in consumer spending during the second half could take place due to higher cost of living anticipated, others believe that the increase in civil servant salary by an average of 13% since last December, the availability of funds from the Employees Provident Fund (EPF) Account 3 and the adjustment to minimum wage to RM1,700 should raise disposable income and spur spending.

Kenanga Research, in a Jan 6 sector report, believes that the RON95 petrol subsidy rationalisation and proposed electricity tariff hikes could pose some headwinds, and it expects the impact to be limited to the top 15% income earners and domestic electricity users, leaving the wider population relatively unaffected.

“With electricity contributing just 2% to 3% to the headline Consumer Price Index, historical precedents such as the 25% electricity tariff hike in mid-2023 [which affected only the top 1% of households] indicate minimal spillover into electricity inflation,” it said.

As such, it believes that the civil servant salary hike and minimum wage increase are likely to support incremental purchasing power, benefiting both the staple and discretionary segments.

Nevertheless, the Kenanga Research analyst, Thin Yun Jing, adds that she sees the EPF Account 3 withdrawal scheme having a limited impact on retail spending.

“The remaining funds available for withdrawal from this account are unlikely to significantly boost discretionary spending, especially for larger purchases or large-ticket items,” she tells The Edge.

Yong adds that the high personal debt levels in the country could redirect the additional disposable income towards debt repayment, while the real income in wages after inflation may not be significant enough, especially if the prices of essential goods increase at a faster pace than discretionary items.

“Overall, the net effect would likely be a more modest increase in consumer spending power, with the real impact dependent on consumer confidence, inflation and the execution of these policy changes,” says Yong.

As at June 2024, the country’s household debt stood at RM1.57 trillion, equivalent to 83.3% of gross domestic product.

Despite the headwinds crimping spending power RGM, in its growth forecast for the Malaysia retail industry in 2025, sees it growing at a rate of 4% from its revised forecast of 3.9% for 2024.

It adds that the biggest challenge for the local retail industry in 2025 is the rising cost of living, a similar concern to last year.

Analysts warn that the consumer sector faces downside risks due to higher-than-expected costs from the petrol subsidy rationalisation, which could dampen consumer spending. However, a smooth and effective execution of the subsidy rationalisation could sustain consumer spending.

Keep to defensive stocks

With many moving parts at play in 2025, analysts and fund managers are opting to stick to defensive consumer stocks and discretionary stocks that would likely benefit from the festivities in the near term.

Yong believes that consumer staples will likely outperform due to the resilience in economic downturns, while food and beverage and those with household product offerings should benefit from steady demand. He also sees discretionary items such as budget fashion or leisure to possibly see gains where both benefit from the seasonal festivities.

UOB Kay Hian head of research Vincent Khoo says he is selectively “overweight” on the consumer sector, opining that the sector will outperform in the near term amid the uncertain and volatile market.

“The hikes from minimum wage and the increase in civil servant salary and consumption spurt play would benefit consumer discretionaries like Mr DIY Group (M) Bhd (KL:MRDIY),” he comments.

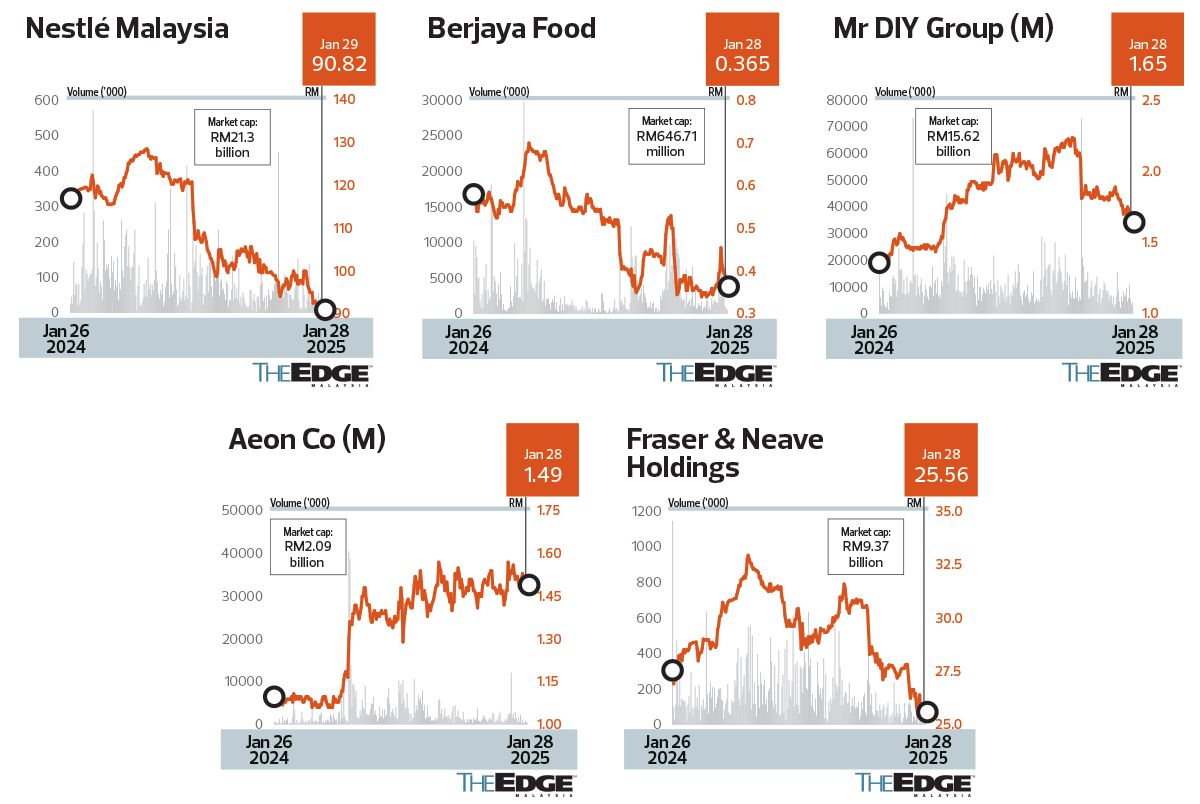

Kenanga’s Thin’s top picks for the sector include the likes of Fraser & Neave Holdings Bhd (KL:F&N) for its earnings defensiveness given the stable demand for essential food items. The counter is also seen as a proxy to a recovery in domestic consumption and the return of tourists in Thailand adds to the appeal. F&N derives slightly over 40% of its revenue from its operations in Thailand. Thin has an “outperform” call on the stock with a target price of RM36.30 based on a one-year forward price-earnings ratio (PER) of 22 times.

On Tuesday, F&N closed at RM25.56, valuing the company at RM9.37 billion.

Apart from F&N, analysts’ top picks for the sector also include Mr DIY and Aeon Co M Bhd (KL:AEON).

MIDF Research likes Aeon for its strong presence in general merchandise and supermarket space which it believes is poised to benefit from robust domestic demand for essential goods. It adds that Aeon’s Property Management Services segment is expected to thrive, driven by optimised tenant mixes and improved rental rates.

It has a “buy” call on the stock with a target price of RM1.67. Aeon closed at RM1.49 with a total market capitalisation of RM2.09 billion.

MIDF’s target price sits on the lower end of the range among the nine analysts covering the stock, ranging from RM1.35 to RM1.95.

Meanwhile, Maybank Investment Bank Research says it likes Mr DIY as it sees it benefiting from higher consumer spending.

“MR DIY has carved out a distinct consumer following with its wide product offering, low price points and mass-market appeal. An overall lift in consumer spending in 2025, driven by higher disposable income will likely drive sales momentum upwards in all MR DIY stores across Malaysia,” it said, adding that Mr DIY plans to open more than 20 new retail chain KKV stores — the group’s newest investment.

Maybank IB Research has a “buy” call on the stock with a target price of RM2.35, based on a 30 times FY2025 estimated PER.

Gaza ceasefire to boost beaten down stocks?

As the Gaza ceasefire and hostage release deal has finally been agreed upon between Israel and Hamas after 15 months of conflict, consumer product companies that have been hurt by boycotts due to their perceived links to Israel could finally get a reprieve.

Nestlé (Malaysia) Bhd’s (KL:NESTLE) earnings for the cumulative nine months ended Sept 30, 2024 fell 27% to RM374.5 million from RM511.77 million a year ago.

While the company did not mention that it has been affected by the boycotts, analysts concluded that the company’s weaker earnings were a result of the boycotts that started at the end of 2023.

Over the period of one year, Nestlé’s share price has declined 28.55% from RM116.754 on Jan 26, 2024 to RM90.82 on Jan 28, 2025.

Meanwhile, Berjaya Food Bhd (KL:BJFOOD), which holds the exclusive rights to operate Starbucks in Malaysia, has seen a similar fate. Its share price has declined 37.1% in a period of one year from 58 sen on Jan 26, 2024 to close at 36.5 sen on Jan 28, 2025.

The group recorded a net loss of RM33.7 million for its first quarter ended Sept 30, 2024 (1QFY2025), representing the fourth consecutive quarter of losses for the group, which also saw its revenue falling 55% y-o-y to RM124.19 million for the quarter.

On Tuesday, Berjaya Food closed at 36.5 sen, valuing the company at RM646.71 million.

Analysts say the ceasefire should bode well for these counters that have been beaten down by the boycotts. However, recovery will take time and may not happen in the immediate term.

“Consumers who opted to boycott earlier have strong allegiance to their belief system and will not succumb to these promises without witnessing strong commitments to end the war. Consumer companies are doing their best to win back consumers but the progress is slow,” says TA Securities head of research Kaladher Govindan.

That said, others also opine that the impact could be modest as consumers may have got used to the myriad alternatives and new brands that have entered the market in the past year, adding that the return to these boycotted brands could be gradual.

Currently, there are three “buy”, five “hold” and five “sell” calls on Nestlé, with an average target price of RM99.22. Berjaya Food has three “sell” and one “buy” call, with target price averaging at 34 sen.

Save by subscribing to us for your print and/or digital copy.

P/S: The Edge is also available on Apple's App Store and Android's Google Play.

- 50,000 Malaysian jobs at risk, business chamber warns as it calls for urgent US tariff mitigation council

- Malaysia refutes 47% US import tariff claim, takes measures to prioritise well-being of businesses and people

- Trump hits China tariff retaliation, says policy will remain

- China retaliation on US farm goods hits soybeans, bolstering Brazil

- Wall Street rout drags Nasdaq near bear market

- ‘Worst-case scenario’ for tech wipes $1.4 trillion from Nasdaq

- Anwar says impact of latest US tariff on nation's economy still being assessed

- Tok Mat, Rubio discuss bilateral relations, Asean-US Special Summit date

- US solar’s hoarding habit will help blunt sting from Trump tariffs

- Wall Street rout drags Nasdaq near bear market