KUALA LUMPUR (Feb 3): Analysts from Hong Leong Investment Bank (HLIB) Research have turned bullish on the banking sector, upgrading it to an “overweight” call after a recent pullback in share prices, citing an attractive risk-reward profile for investors.

The equity research firm noted that the sector remains undervalued, currently trading below its pre-pandemic five-year average price-to-book (P/B) ratio — positioned one standard deviation below the historical mean.

Further, HLIB Research also believes that Malaysian banks are well-positioned to benefit from a potential emerging market (EM) rotational play, driven by the unwinding of long-term inflation expectations in the US, a stronger greenback, and elevated Treasury yields.

However, the research firm flagged that the market has yet to fully account for potential downward surprises in US inflation, particularly from lower oil prices and artificial intelligence (AI)-driven productivity gains.

Looking ahead, HLIB Research expects domestic liquidity, particularly from government-linked investment companies (GLICs), to provide near-term support for index-heavy sectors.

In a separate note, CGS International, which kept a similar stance on the banking sector, cited potential sector-rerating catalysts of further write-backs in macro-overlays (MO), and rising dividend payout ratios.

The research house projected a 6.2% net profit growth for banks in 2025, driven by a 7.9% increase in net interest income, and a 3.5% rise in non-interest income. Loan growth, which moderated to 5.5% at the end of 2024, is expected to remain in the range of 4.5% to 5.5% in 2025.

In 2024, the banking sector’s asset quality improved, with gross impaired loans (GIL) — debts deemed unrecoverable as a percentage of total loans — falling by RM2.8 billion, leading to a 21-basis-point contraction in the GIL ratio. Banks’ total provisions also declined by RM1.24 billion quarter-on-quarter in 4Q2024.

CGS further noted that loan loss provisioning (LLP) remained low in 4Q2024, coming in below RM1 billion — a more than 40% year-on-year decline, which was partly attributed to the write-back of macro-overlays by certain banks, it added.

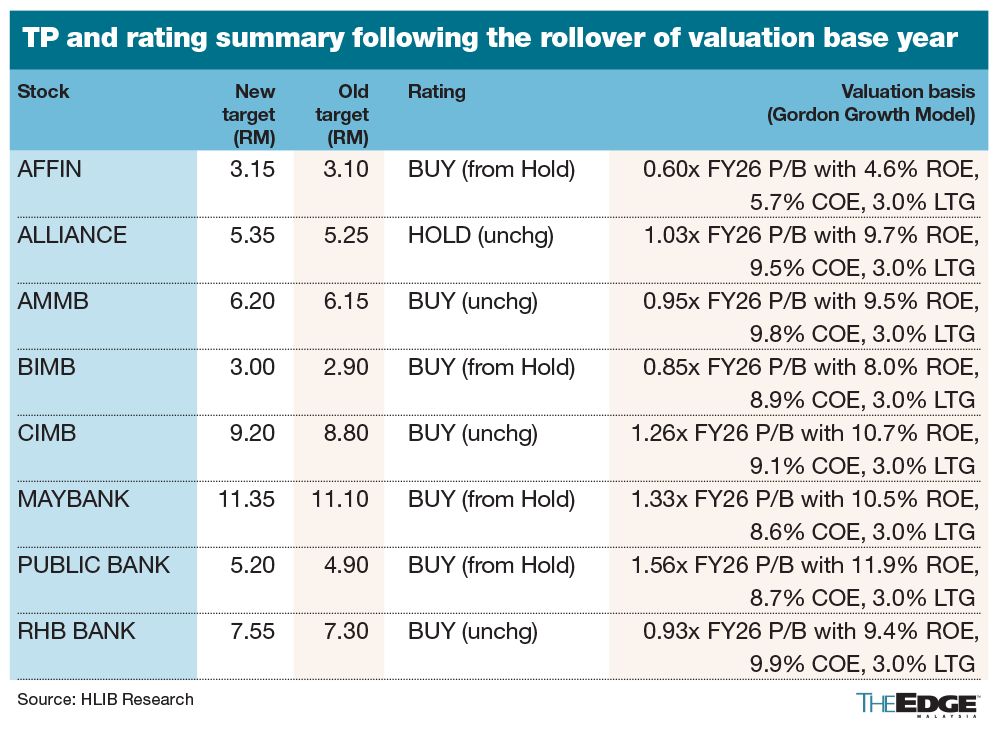

Among notable upgrades under HLIB’s coverage are Affin Bank Bhd (KL:AFFIN) (target price/TP: RM3.15), Bank Islam Malaysia Bhd (KL:BIMB)(TP: RM3.00), Malayan Banking Bhd (KL:MAYBANK)(TP: RM11.35), and Public Bank Bhd (KL:PBBANK)(TP: RM5.20). Meanwhile, CGS’ top picks include Hong Leong Bank Bhd (KL:HLBANK), Public Bank; and AMMB Holdings Bhd (KL:AMBANK), all rated as “add”.

- All Malaysia-based carriers failed to meet international punctuality target in January — Mavcom

- EU races to expand €2 tril trade network as US links sour

- What Samsung and Vietnam stand to lose in Trump's tariff war

- Trump's trade team chases 90 deals in 90 days. Experts say good luck with that

- US tariffs risk straining Malaysia-China ties, Anwar warns

- Aaron-Wooi Yik trounce defending champions, edge closer to first BAC title

- Amanah confident in helping to secure 5 voting districts in Ayer Kuning state by-election

- Russia's Lavrov praises Trump's understanding of Ukraine conflict

- Trump exempts phones, computers, chips from ‘reciprocal’ tariffs

- Fed’s deepest tariff fear is a price shock that won’t fade away