KUALA LUMPUR (Jan 31): Maybank Investment Bank Bhd (Maybank IB) maintained its “negative” rating on the petrochemical sector as the research house sees oversupply persisting for at least the next two to three years.

The rating came after the research house attended Petronas Chemicals Group Bhd’s (KL:PCHEM) products outlook call, which highlighted the supply and demand for most of the olefin and polyolefin producer’s products from 2025 to 2029, according to a note on Friday.

Maybank IB recommended “sell” on Petronas Chemicals and another petrochemical producer Lotte Chemical Titan Holdings Bhd (KL:LCTITAN).

“The outlook call reinforced our bearish view on the petrochemicals sector as most product spreads are likely to face capacity additions exceeding demand growth over the next few years,” it said.

Maybank IB said a glut in supply is expected to persist for ethylene (up to 2028) and polyethylene (up to 2027) — this may include high-density, low-density and liner low-density polyethylene.

The outlook for monoethylene glycol, on the other hand, was slightly better as demand growth is expected to exceed capacity additions in 2025, before a supply surplus in 2026, said Maybank IB.

“The only good news throughout the call was methanol’s annual demand growth, which is expected to exceed capacity additions in 2026-2030E (estimates), but may also face a short-term supply glut environment in 2025E,” it noted.

Urea, meanwhile, is projected to have “0% demand growth” up to 2026, with about two to three million metric tonnes of new capacity additions in the pipeline, it said.

“The petrochemical sector appears to be in an L-shaped recovery. With such heavy capacity addition coming onstream over the next few years, it is unlikely that the sector will revisit its ASP (average selling price) highs in 2021 and 2H22 (second half of 2022) anytime soon,” it said.

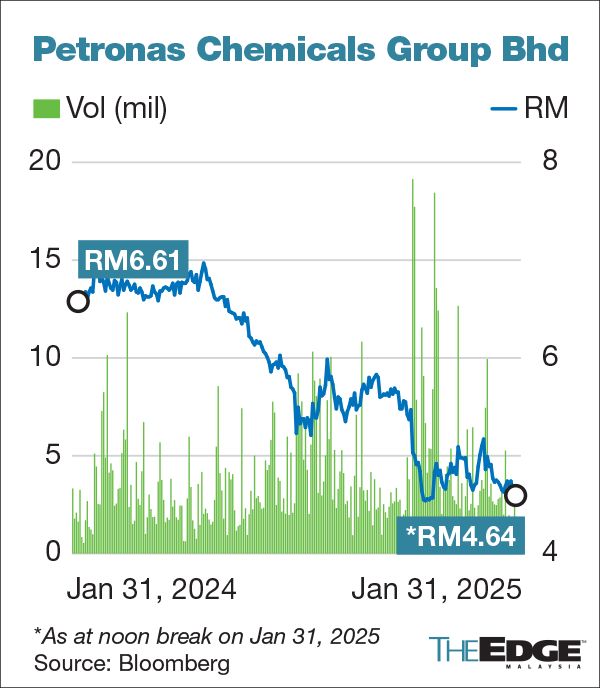

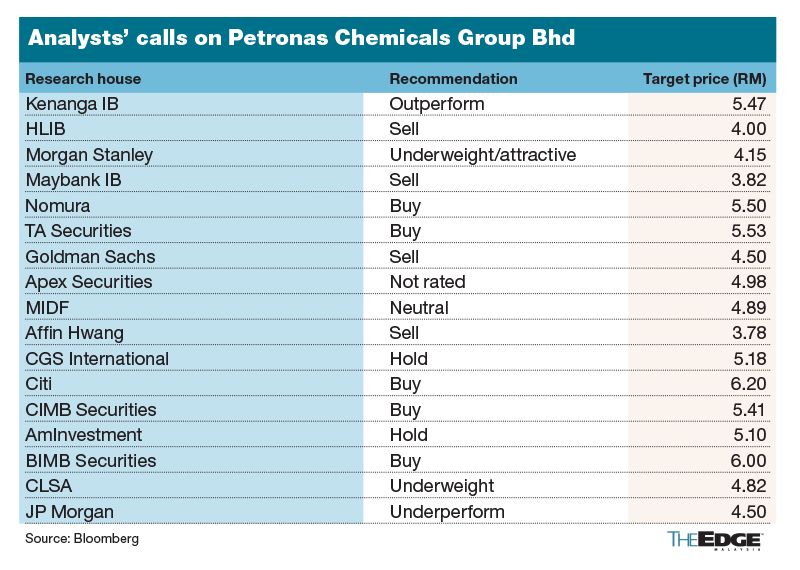

Maybank IB flagged that the worst is not over for Petronas Chemicals and expects the group to record a year-on-year decline in profit for the financial year of 2025 (FY2025), with profits post-incorporation of Pengerang Petrochemical Company Sdn Bhd’s (PPC) losses of more than RM700 million annually. Despite this, Petronas Chemicals still feature six “buy” calls, four “hold” ratings and six “sell” recommendations, according to Bloomberg data. In the past one year, the counter has declined over 31%

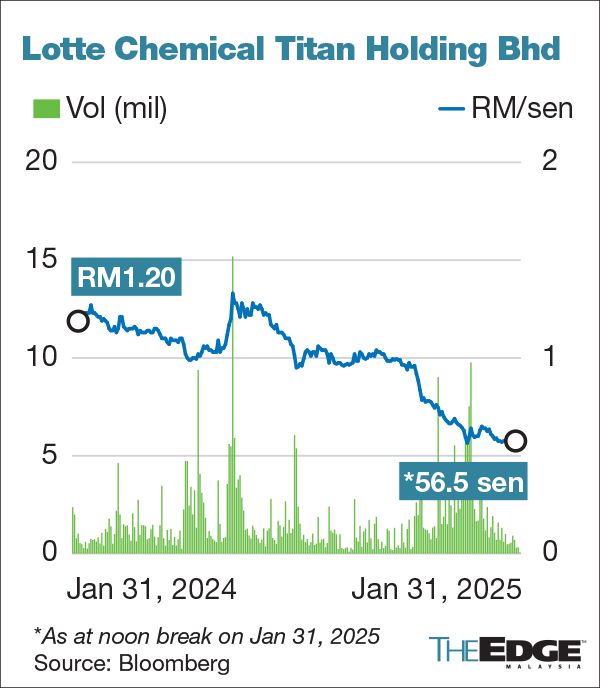

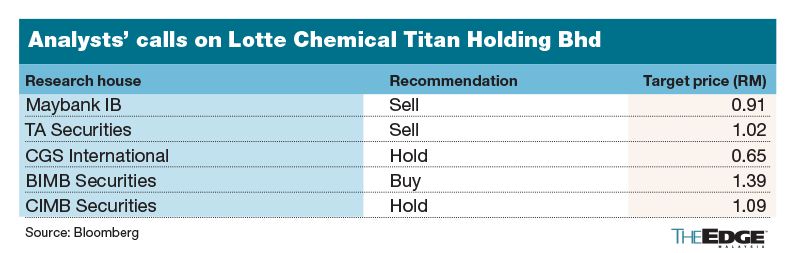

On Lotte Chemical, the research house sees that its polyethylene-naphtha spreads are not wide enough for the company to turn profitable. The Main Market-listed company has been loss-making for 10 consecutive quarters since the second quarter of 2022. The counter has one “buy” recommendation, two “hold” and another two “sell” calls. The stocks has fallen over 52% in the past one year.

- Mr DIY founder Tan Yu Yeh relinquishes vice chairman post, to serve as adviser

- 50,000 Malaysian jobs at risk, business chamber warns as it calls for urgent US tariff mitigation council

- Malaysia refutes 47% US import tariff claim, takes measures to prioritise well-being of businesses and people

- Trump hits China tariff retaliation, says policy will remain

- China retaliation on US farm goods hits soybeans, bolstering Brazil

- ‘Worst-case scenario’ for tech wipes $1.4 trillion from Nasdaq

- Anwar says impact of latest US tariff on nation's economy still being assessed

- Tok Mat, Rubio discuss bilateral relations, Asean-US Special Summit date

- US solar’s hoarding habit will help blunt sting from Trump tariffs

- Wall Street rout drags Nasdaq near bear market