(Jan 28): Defaulted Chinese developer Logan Group Co said that creditors holding over 66% of the group’s US$6.2 billion (RM27.26 billion) offshore debt have signed an agreement in support of its restructuring plan, a key progress in its yearslong overhaul talk.

The Shenzhen-based homeseller said that other creditors holding over 12% of debt have indicated support but required more time to complete their internal approval processes due to the Lunar New Year holidays, according to a Hong Kong stock exchange filing late Monday. The early-bird deadline has been extended to Feb 12, the filing shows.

If Logan is able to obtain such approvals, the company’s support level for the debt plan will surpass 78%, meeting the minimum threshold of 75% required for the execution of a restructuring arrangement in Hong Kong.

That would bring the tussle between Logan, which has more than 150 residential developments in China, and its creditors one step closer toward the finishing line. The builder’s restructuring process has stretched over several years, marked by periods of progress as well as setbacks.

Logan, once the nation’s 20th-biggest builder by sales, updated its restructuring plan earlier this month. The amount of debt eligible for cash payouts to creditors has reduced to a cap of US$787 million from US$1.3 billion announced in January 2024.

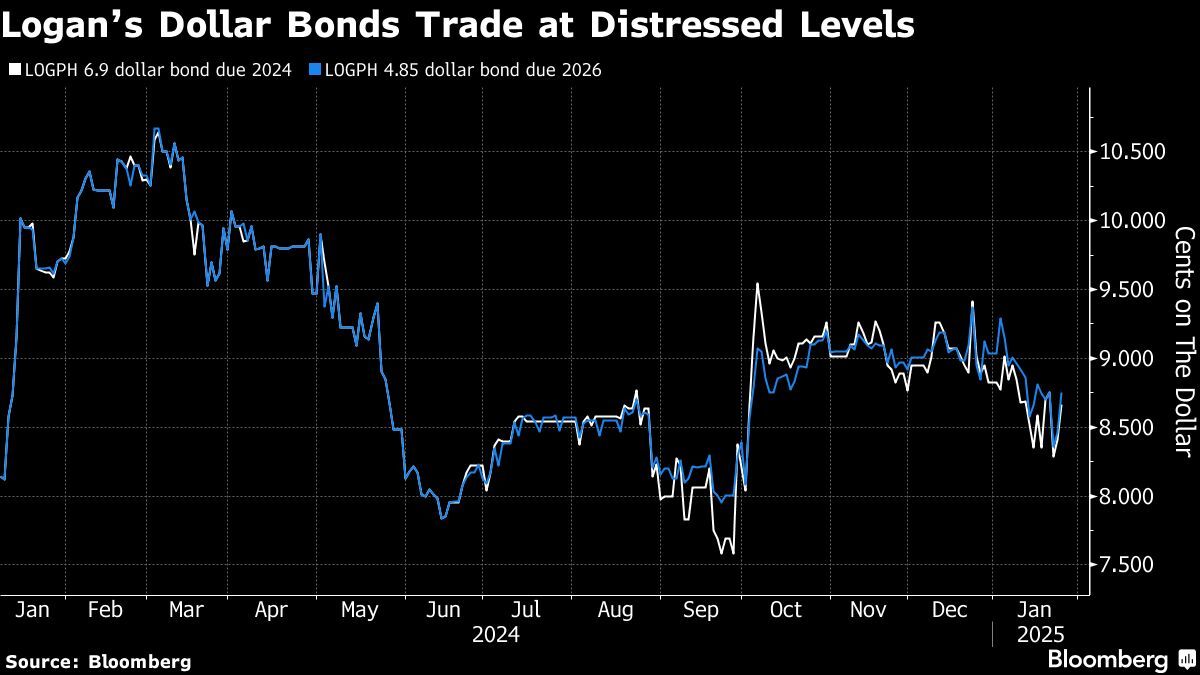

Logan gained support from a group of bondholders on the debt restructuring plan in January after some negotiation. Prices of the company’s greenback bonds are trading at distressed levels, below 10 cents on the dollar, according to data compiled by Bloomberg.

Uploaded by Arion Yeow

- Pak Lah, the gentleman of politics, passes away at 85

- MOF Inc-owned Pernas appoints former MBSB Bank CEO as new chief

- Malaysian Bar defends Chief Justice amid backlash from former law minister over judicial reform remarks

- Yellen says sell-off in Treasuries shows US confidence loss, not dysfunction

- Reach Energy faces trading suspension, possible delisting, as regularisation plan deadline extension rejected