This article first appeared in Capital, The Edge Malaysia Weekly on January 27, 2025 - February 2, 2025

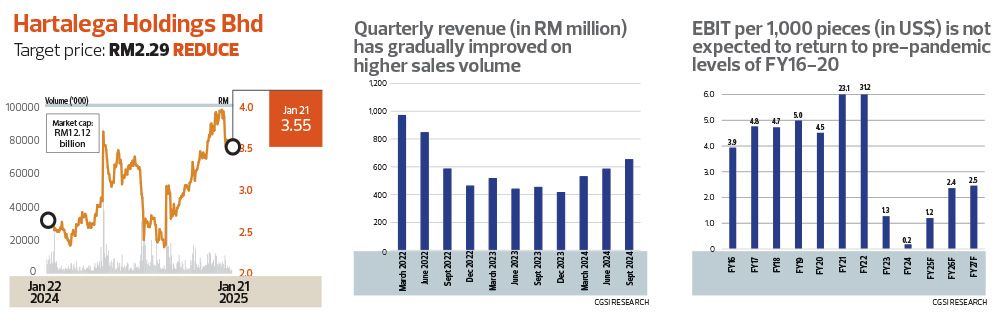

Hartalega Holdings Bhd

Target price: RM2.29 REDUCE

CGS INTERNATIONAL (JAN 17): We hosted Hartalega Holdings Bhd (KL:HARTA) at our recent Malaysia Corporate Day 2025 event on Jan 8. Following the US imposition of a 50% import tariff on China-made medical gloves from Jan 1, 2025, there has been a notable shift in orders to Malaysian glove manufacturers. Hartalega expects its December 2024 quarter sales volume to grow by up to 10% q-o-q to 7.5 billion pieces, compared with 6.8 billion in the September 2024 quarter. However, sales volumes for the March 2025 quarter are projected to decline by 5% to 10% q-o-q due to frontloaded orders.

The company reports pushback from US distributors against substantial average selling price (ASP) increases by Malaysian glove makers, citing lingering excess capacity in the sector. This indicates limited cost pass-through ability, while improving, which remains below pre-Covid-19 levels. Additionally, falling raw material prices are expected to moderate ASPs in the March 2025 quarter, potentially leading to slightly weaker operational performance. However, the weaker ringgit against the US dollar (averaging 4.50 compared with 4.41 in the December 2024 quarter) may partially offset this.

We keep our “reduce” call on persisting operational challenges, coupled with our view that Hartalega‘s operational margins may not, even by FY27, return to pre-pandemic FY16-FY19 levels. Current valuations of 42 times FY26 PER and 2.5 times FY26 P/B still look excessive as we expect FY26-FY27 return on equity to remain subdued at 6% to 7% (versus FY16-FY19 average of 17%) even as we project robust EPS recovery.

Upside risks include stronger-than-expected volume growth driven by a new pandemic, reduced pricing power among regional competitors and sustained ringgit weakness. Conversely, downside risks include intensifying price competition and higher operating costs.

Pekat Group Bhd

Target price: RM1.17 HOLD

APEX SECURITIES (JAN 20): We recently visited Pekat Group Bhd’s (KL:PEKAT) EPE Switchgear (M) Sdn Bhd’s facility in Nilai, Negeri Sembilan, a specialist in manufacturing medium voltage switchgear products. The facility is operating at 70% utilisation.

With high barriers to entry and only five to seven market players, we believe EPE is well positioned, backed by 50 years of experience and a proven track record. EPE has partnered with Tenaga Nasional Bhd (KL:TENAGA) to develop an innovative feeder pillar with a smart monitoring system for both new developments and urban replacements, targeting an estimated market of 8,000-10,000 units annually. The company holds an unbilled order book of RM180 million, ensuring earnings visibility for FY25-FY26 and a tender book of up to RM500 million, with a historical win rate of 20%.

Following a recent rally in its share price, the recommendation has been revised to “hold” with a target price of RM1.17 derived from an SOP valuation. The company also holds a three-star ESG rating.

We remain in favour of Pekat for its synergistic business model, strong margins in the EPE segment and sustainable order book. We also noted that Pekat’s strong historical financial results qualify the group for the transfer to the Main Market of Bursa Malaysia.

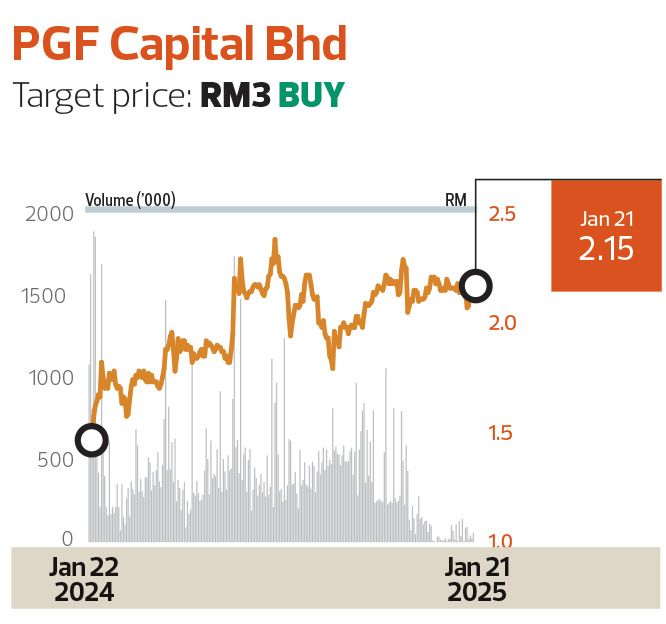

PGF Capital Bhd

Target price: RM3 BUY

TA SECURITIES (JAN 21): PGF Capital Bhd’s (KL:PGF) 9MFY25 core profit of RM23.2 million — after adjusting for foreign exchange losses of RM3.2 million and other exceptional items — met 83% of our full-year forecast. This is within expectations, as exports typically slow seasonally in the last quarter.

On a q-o-q basis, 3QFY25 core profit declined to RM7 million from RM9.7 million, driven by reduced construction activity in Australia, which impacted glass wool panel exports. Exports to Australia and New Zealand accounted for 73% of the group’s total revenue this quarter.

The ongoing housing crisis in Australia, marked by rising home prices due to delays in housing approvals and red tape, remains unresolved. However, we expect the government to expedite approvals, increasing housing supply and providing long-term demand for glass wool insulation panels.

Domestically, the Energy Efficiency and Conservation Act 2024, effective Jan 1, 2025, presents new opportunities for PGF’s glass wool manufacturing. The act, aimed at promoting energy sustainability, is expected to boost demand for insulation products in government and commercial buildings.

Genting Malaysia Bhd

Target price: RM3.30 BUY

PHILLIP CAPITAL (JAN 21): Genting Malaysia Bhd (KL:GENM) 4Q24 video lottery terminal (VLT) operations continued outperforming peers in New York, with its market share rising to 43.3%.

Genting Malaysia has reopened part of the former Genting Casino floor, representing less than one-third of the previous space. Heading into the Lunar New Year, two scenarios are possible: (i) Both Genting Casino 1 and 2, plus connecting areas, could progressively reopen, restoring about half of the old casino floor; or (ii) status quo, with only Genting Casino 2’s existing space operational.

We raise our 2024–2026 earnings forecast by 2%–4%, factoring in a revised foreign exchange assumption and lower tax rate (from 30% to 26%), partially offset by higher associate losses from Empire Resorts.

We maintain a “buy” call on Genting Malaysia with an unchanged SOP-derived target price of RM3.30. It trades at an undemanding 6.1 times 2025E EV/EBITDA with an 8% dividend yield. Potential rerating catalysts include securing the downstate New York City casino license, expected by end-2025. Key risks include lower-than-expected win rates, higher gaming taxes, drag from associates and value-destructive related-party transactions.

Save by subscribing to us for your print and/or digital copy.

P/S: The Edge is also available on Apple's App Store and Android's Google Play.

- China suppliers mock tariffs with Nike, Lululemon deals on TikTok

- Malaysia declares state funeral for Tun Abdullah Ahmad Badawi

- Reach Energy, Cahya Mata, Able Global, Pestec, Bina Puri, Jentayu Sustainables

- Yellen says sell-off in Treasuries shows US confidence loss, not dysfunction

- Nvidia to produce AI servers worth up to US$500b in US over four years