(Jan 21): France’s first syndicated bond sale in about eight months met an unprecedented flood of investor demand as the new government attempts to muster enough political support to pass a much-needed budget.

Orders for the new €10 billion (RM46.51 billion) note maturing in 2042 blasted past €134 billion, the most on record, according to data compiled by Bloomberg. Tuesday’s offering will price at eight basis points over comparable bonds, said people familiar with the matter who asked not to be identified.

The country’s last syndicated offering — an inflation-linked bond — was in May, less than a month before French President Emmanuel Macron called early legislative elections and plunged the country into a period of political turmoil.

France’s borrowing costs jumped sharply over the past six months as investors demanded greater compensation to hold its debt through a period of political instability. The previous government, led by Michel Barnier, collapsed after failing to win enough support for a budget that included big spending cuts to tackle the country’s large deficit.

Prime Minister Francois Bayrou is facing similar challenges. He survived a no-confidence vote last week with both the far-right and the Socialists — who joined up to push out his predecessor — abstaining. But the outlook remains uncertain.

Bayrou’s finance minister has secured support from Brussels for his deficit-reduction path, which aims to narrow the deficit to 5.4% of GDP this year. While that’s less ambitious than the previous government’s target of 5%, the prime minister has maintained a goal of getting it below the European Union’s 3% limit by 2029.

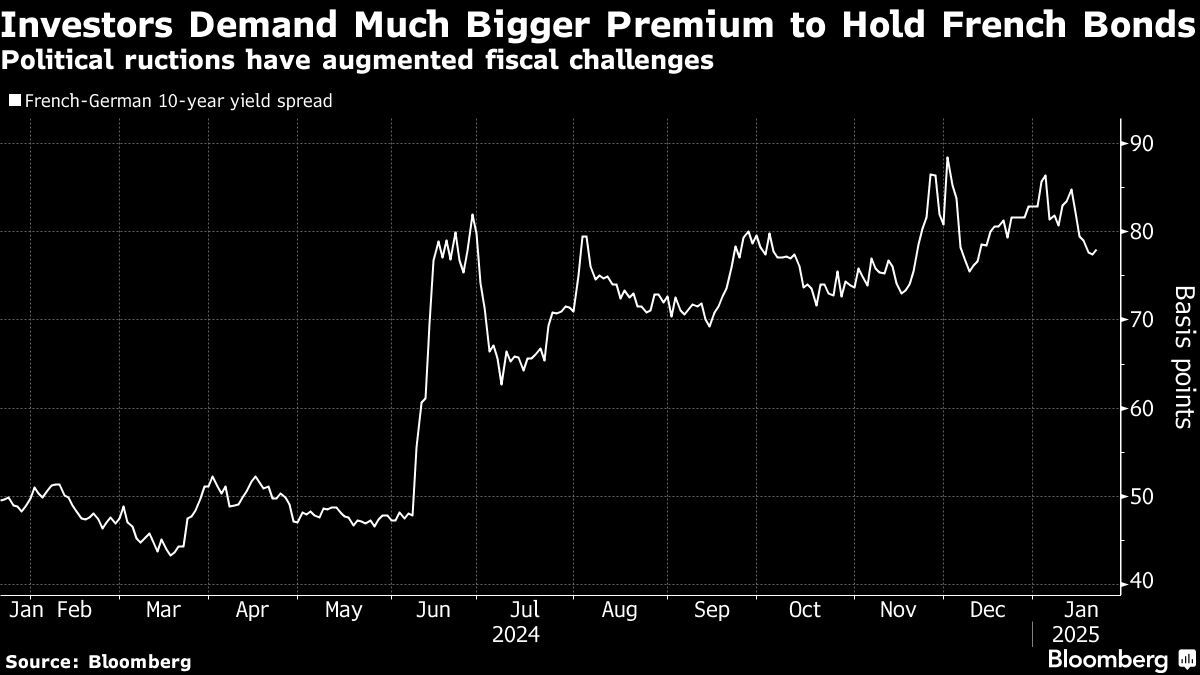

The gap between French and German 10-year yields, a closely watched risk gauge, last week fell the most since October and was one basis point tighter at around 77 on Tuesday.

Debt syndications are typically more expensive than auctions but they allow governments to raise large sums quickly while diversifying their investor base.

Uploaded by Arion Yeow

- Global funds hit pause on Indonesia after Prabowo policy changes

- Embattled billionaire Ong Beng Seng’s firm to be run by veteran executives

- Jentayu signs 40-year power purchase agreement for RM2.8b 162MW Sabah hydropower project

- Trump warns tariffs coming for electronics after reprieve

- Singapore eases monetary policy as expected, sees weaker growth in 2025

- MOF Inc-owned Pernas appoints former MBSB Bank CEO as new chief

- Ageas to buy UK insurer Esure from Bain for £1.3 bil

- China, Vietnam ink deals as Xi visits Hanoi amid US tariff tensions

- Cars to gadgets: What US consumers are losing to Trump tariffs

- Citigroup turns cold on US equities, joining Wall Street peers