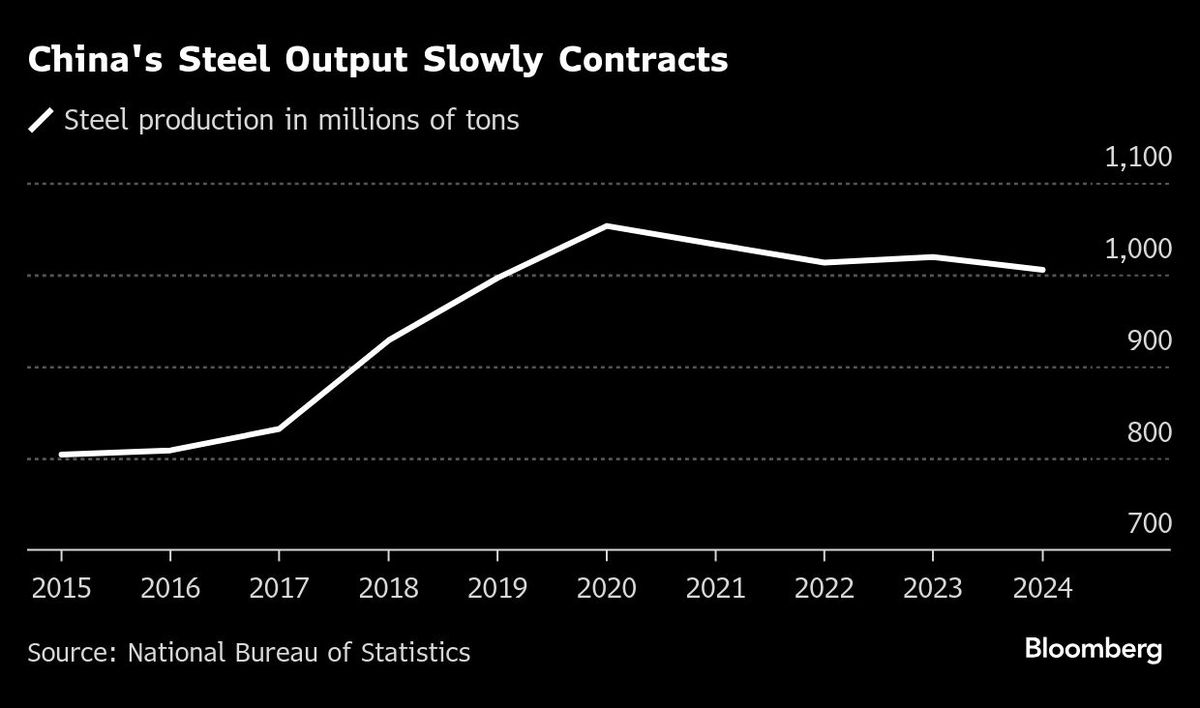

(Jan 20): China is still producing too much steel, setting up the industry for more pain as domestic consumption drops and unprofitable mills reach a tipping point.

Output edged lower in 2024, although it stayed above one billion tonnes for a fifth consecutive year. Deeper cuts will be necessary to align with demand, which is faltering due to the protracted crisis in China’s property market, and the changing nature of its economy.

Decades of expansion, driven by construction and state investment, are at an end, and new growth areas for the industry aren’t enough to replace those drivers. The government is shifting its focus to greener, high-tech growth and consumption, which is shrinking steel’s importance to the economy.

“The worst is not over,” said John Chen, Standard Chartered Plc’s regional head of commodities sales in Singapore. “Almost all steel mills are bleeding.”

Chinese research firm Mysteel expects output to sink to less than 900 million tonnes by 2030. Some projections for demand are even more stark.

From over one billion tonnes in 2020, Chinese steel consumption could fall below 800 million tonnes by 2030, according to the base case forecast by Bloomberg Intelligence. Its worst case is that consumption plunges to 525 million tonnes by the end of the decade.

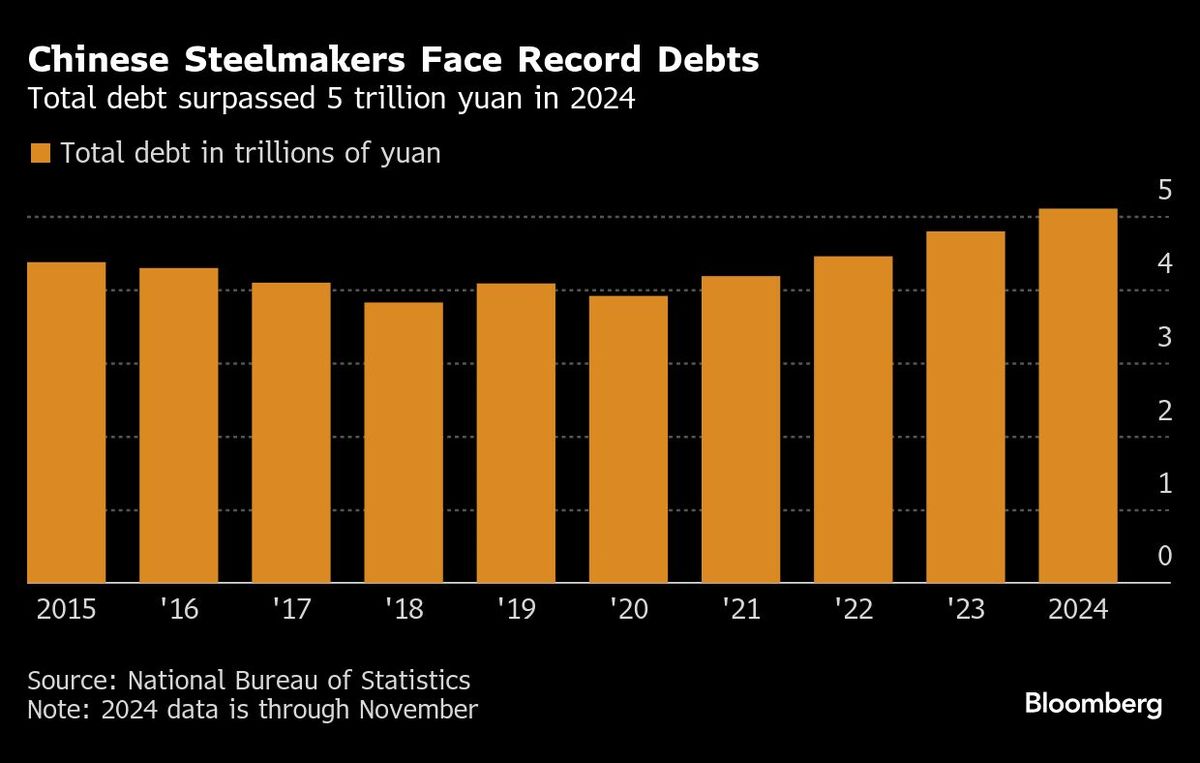

Those kind of predictions have lit a fire under efforts to consolidate the industry, which are likely to speed up this year, as mills struggle to maintain cash flow and margins. The sector has lost money for most of the year, while its total debt had climbed to a record 5.1 trillion yuan (US$696 billion, or RM3.13 trillion) by November, according to the statistics bureau.

Smaller, private mills are most vulnerable, as they tend to focus on construction steel and are more geared to the crisis in the property market, said Mysteel analyst Yu Chen in Shanghai.

In the latest earnings period, steelmakers recorded their weakest free cash flow for a third quarter since 2015, according to Bloomberg calculations based on 59 steel mills listed on the mainland. Their debt-to-asset ratio, meanwhile, increased to the highest since 2017.

Although the sector’s contribution to the economy has lessened over the years, it was still worth 5.7% of nationwide gross domestic product (GDP) in 2023, according to an estimate by Gary Ng, senior economist at Natixis SA in Hong Kong. That has implications for the growth targets set by local governments, including the biggest steel producing province of Hebei.

“If we are expecting another harsh winter for the Chinese steel industry, several regional governments may particularly struggle,” said Martina Reber, an analyst at Frontier Commodities in Zug, Switzerland. “Hebei province has already shown signs of significant strain.”

The province’s main steel hub of Tangshan is a case in point. Steelmaking accounts for half the city’s economy, but in the first 10 months of last year, it was Tangshan’s worst-performing industry, after racking up losses of 3.1 billion yuan.

Exports, which helped shore up demand last year, are also facing a decline, as importing countries step up anti-dumping measures and tariffs. Domestically, rising usage by manufacturers and carmakers are helping offset the housing market’s weakness, but they aren’t enough to completely fill the shortfall.

“The real estate sector must stabilise before we can see a floor to steel demand, or production,” said Jinshan Xie, an analyst at Shanghai-based Horizon Insights.

Uploaded by Liza Shireen Koshy

- Malaysia secures zero-import duties with four-nation European bloc amid trade uncertainties

- Paramount's 70%-owned unit and 2 others sued over Taman U-Thant land deal

- US Treasuries slide with sell-off worst since 2019 repo blowout

- TNB, Paramount, TXCD, UUE, SkyWorld, LBS Bina

- Yusoff Rawther should have parked car inside condo if having issues with locks, says IO, but cross-examination answers seem to favour the defence

- Janus Henderson fund manager says investors should cut exposure to stocks as recession looms

- Lagarde tells finance chiefs to let EU take lead on trade talks

- Dimon predicts Treasury market ‘kerfuffle’ where Fed steps in

- Wan Rosdy appointed National Entrepreneur and MSME Development Council Special Advisor

- Volvo Cars may take up to two years to expand US production to avoid tariffs, CEO tells daily DN