(Jan 13): Just over a year ago, Sunac China Holdings Ltd became a model for the country’s defaulted developers by clinching the sector’s first major offshore debt restructuring deal. Now, its problems are mounting again.

At a time when Sunac is trying to complete an onshore debt overhaul, questions over whether it will meet looming repayment deadlines are putting its offshore agreement at risk. On top of that, it’s now contending with another court petition to wind up.

Sunac said late on Friday that it “can’t rule out” a second offshore debt restructuring. Should the wind-up petition become successful, it may not be able to pay some offshore debt.

The first task for Sunac is to secure support for its proposal to restructure about 15.4 billion yuan (US$2.1 billion, or RM9.47 billion) of onshore debt as early as Jan 21, people familiar have said. Next up is the liquidation hearing in Hong Kong on March 19. Later that month, the developer must pay about US$60 million in estimated interest on its restructured dollar notes, or face the possibility of a second revamp of its offshore borrowings.

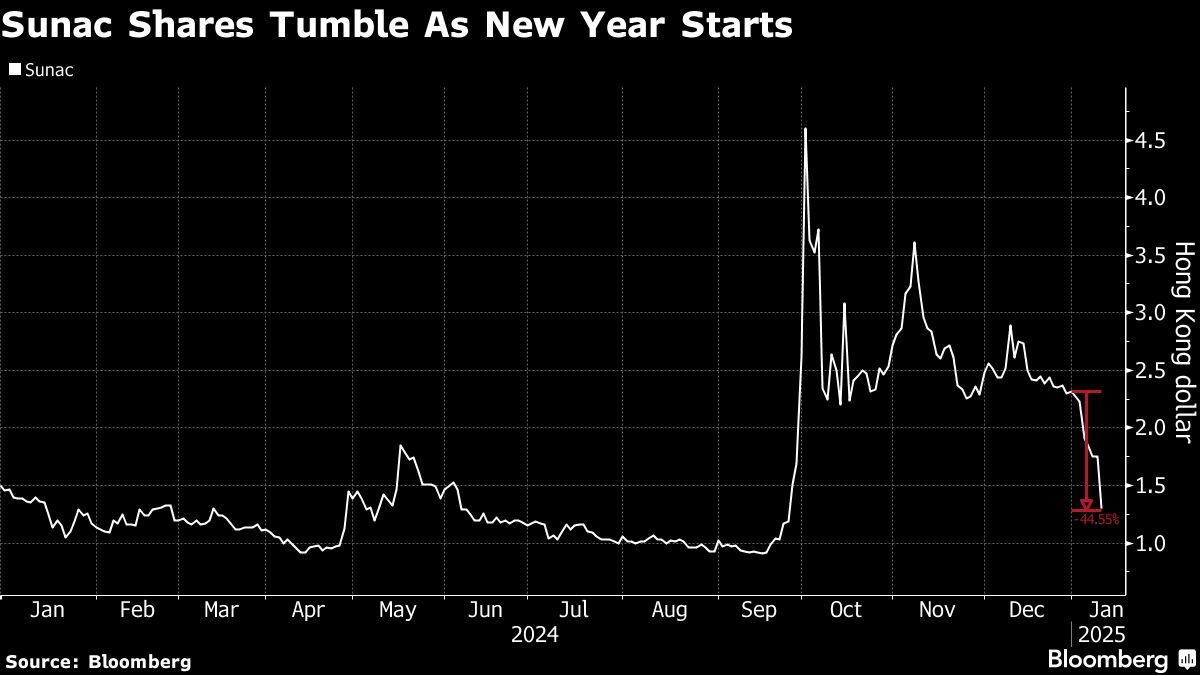

Sunac became one of China’s first distressed developers to restructure its offshore debt in late 2023, about a year and half after defaulting on a dollar bond, fuelling optimism that such deals can be done. But its stock and bond prices have now slid to the lowest level in months, as the country’s ongoing housing downturn dims expectations that the company can revive itself.

On top of interest payments, Sunac also has a US$500 million note due on Sept 30, though the maturity can be extended by a year, according to the company’s filing.

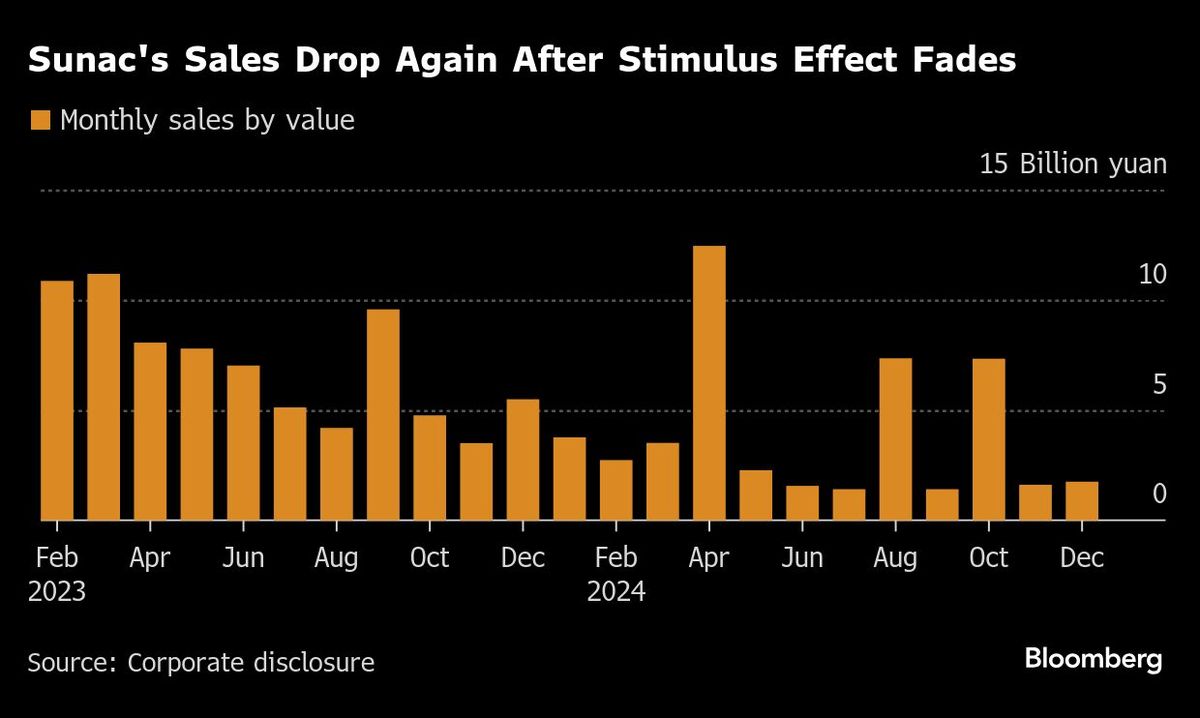

“Sales in the primary market are clearly not recovering sufficiently for these property developers to meet their ongoing debt servicing needs,” said Justin Ong, a Singapore-based credit analyst at Columbia Threadneedle.

Sunac’s diminishing cash of about 5.4 billion yuan as of June could still cover interest payments for dollar bonds due by March 30, according to Bloomberg Intelligence. Yet, the developer might still choose to suspend payments in favour of a second offshore restructuring, analysts Daniel Fan and Hui Yen Tay said.

A representative for Sunac declined to comment.

Sunac earned plaudits from creditors when it quickly amassed support for its offshore debt restructuring, before China’s property crisis intensified last year. But private-sector developers have yet to escape a years-long downturn in the country’s property market, as sales of new homes remain weak and prices continue to fall. Mounting government support has focused on rekindling demand, rather than resolving liquidity challenges for distressed builders.

Policy aid for developers’ financing from the past year won’t reach real estate companies, including Sunac, Bloomberg Intelligence’s Fan added.

Relaxed funding rules are mostly helping builders with investment properties that can be used as collateral, Fan added.

Key dates

- Jan 21: Sunac has yet to win bondholders’ approval for extension on the principal and interest payments for one of its 10 onshore bonds, people familiar said. It’s a 6.8% note that has a 15% installment due on Dec 9, the people said, adding that the grace period ends on Jan 21.

- March 19: A Hong Kong court is due to hear a liquidation petition from China Cinda HK Asset Management Co, Ltd. A similar wind-up petition was filed against Sunac several months after its initial default, but was withdrawn in mid-2023.

- March 30: Sunac needs to make an interest payment of about US$60 million in cash on its restructured dollar notes, according to Bloomberg calculations based on company filings

- Sept 30: In 2023, Sunac extended part of its offshore debt into six tranches of bonds, including a short-dated tranche A note of US$500 million due Sept 30. The note’s maturity can be extended by a year.

Uploaded by Liza Shireen Koshy