This article first appeared in The Edge Malaysia Weekly on January 13, 2025 - January 19, 2025

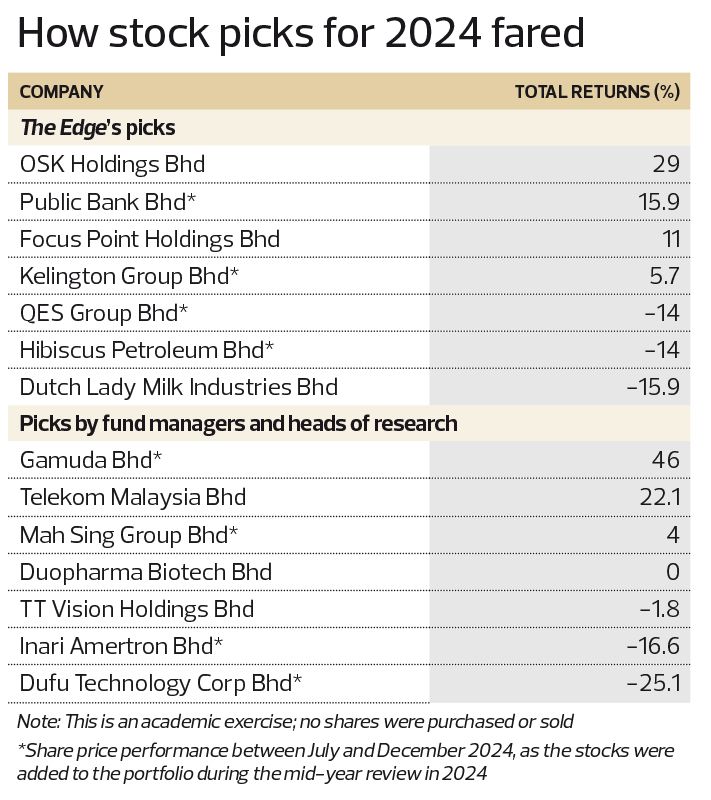

LAST year, the performance of stocks picked by The Edge, fund managers and heads of research was mixed, although it was a good year for the local bourse, especially the benchmark FBM KLCI which posted its first annual gain since 2020.

Among The Edge’s stock picks for 2024, OSK Holdings Bhd (KL:OSK) was the top performer as the stock garnered a total return of 29%, partly driven by its unbilled sales of more than RM1 billion from its property segment.

Our banking pick, Public Bank Bhd (KL:PBBANK), also yielded a decent return of about 16% for investors since we made a “buy” recommendation in mid-2024 after its share price had slipped below RM4. At that time, Public Bank was seen as a laggard with appealing valuations, prompting its share price to surge to a high of RM4.84 in August before paring gains to close at RM4.56.

Kelington Group Bhd (KL:KGB), which provides ultra-high purity UHP gas delivery solutions to the electronics and semiconductor industry, registered a total return of 5.7%. The group, which had an order book of RM1.45 billion as at end-September 2024, is also bidding for jobs worth RM2.62 billion, being its highest ever tender book.

However, Dutch Lady Milk Industries Bhd (KL:DLADY), QES Group Bhd (KL:QES) and Hibiscus Petroleum Bhd (KL:HIBISCS) — which were added to our portfolio during the mid-year review — registered negative returns of 15.9%, 14% and 14% respectively.

Looking at the picks by fund managers and heads of research, Malacca Securities head of research Loui Low’s pick, Telekom Malaysia Bhd (KL:TM), saw a total return of 22.1% in 2024, benefiting from the continued data centre boom, especially the partnership with Singapore Telecommunications Ltd (Singtel) to establish greenfield data centre facilities in Iskandar Puteri, Johor.

Meanwhile, MIDF Research head Imran Yassin Md Yusof’s 2H2024 pick, Gamuda Bhd (KL:GAMUDA), continued to perform well with a total return of 46% during the period, even after a strong rally in the first half of the year.

Technology stocks Inari Amertron Bhd (KL:INARI) and Dufu Technology Corp Bhd (KL:DUFU), however, failed to demonstrate any meaningful recovery. Both counters were down by 16.6% and 25.1% respectively.

What are the investment opportunities that lie ahead for investors? Let’s take a look at the stock picks by The Edge, fund managers and heads of research for 2025.

Picks by fund managers and heads of research for 2025

Duopharma Biotech

Tradeview Capital CEO Ng Zhu Hann:

Duopharma Biotech Bhd (KL:DPHARMA) is a proxy for the healthcare reform sector, as well as a potential beneficiary of the reversal of the US dollar strength and ringgit recovery.

The healthcare sector in Malaysia has been underinvested for many years and there is a need to increase the percentage of investment into this public sector for the betterment of the rakyat.

Duopharma, as one of the key suppliers to the private and public healthcare sectors, will stand to benefit from higher orders and demand. Additionally, the completion of the new manufacturing facility will help with the company’s supply capacity to meet increasing demand.

For the July-September 2024 quarter, Duopharma’s net profit jumped 73.9% to RM15.59 million from RM8.97 million a year ago. This was on the back of higher sales across key sectors, particularly the public health segment.

Last October, Duopharma secured five additional supply contracts from Pharmaniaga Bhd (KL:PHARMA), totalling RM87.66 million, to provide 10 pharmaceutical and non-pharmaceutical products to government offices and facilities that Pharmaniaga operates.

EG Industries

Malacca Securities head of research Loui Low:

EG Industries Bhd (KL:EG) is an electronics manufacturing services (EMS) player that has expanded its capabilities into 5G technology, artificial intelligence (AI) modules and optical components, via collaborations with Cambridge Industries.

Scheduled for completion in 2025, the upcoming Smart Factory 4.0 in Penang, with a 45% expansion in total built-up area that enhances output capacity, is expected to boost EG’s earnings potential.

EG is anticipated to focus on high-margin products, producing cutting-edge 1.6T photonics optical modules for 5G wireless networks, enabling high-speed data transmission crucial for automation and AI applications.

The company kicked off its FY2025 with a record profit of RM35.77 million for the July-September 2024 quarter, driven by higher sales and better margins, particularly from 5G wireless access and photonic-related products.

NationGate Holdings

Malacca Securities head of research Loui Low:

NationGate Holdings Bhd (KL:NATGATE) is an EMS player specialising in the assembly and testing of electronic components and products across various sectors, including networking and telecommunications, consumer electronics, automotive and semiconductors.

It is the first company in Malaysia to manufacture AI servers locally. It will be collaborating with industry leaders, including Nvidia, to integrate cutting-edge technologies into its AI server offerings.

The company had recorded its strongest quarterly net profit since its listing of RM46.6 million in the third quarter of 2024, which included a net forex gain of RM76.2 million. Given the anticipated boom in the data centre (DC) market over the next three to five years, the group’s earnings are expected to grow.

Notably, its share price has seen a jump since the start of the year, touching a record high of RM3.03, on optimism about its prospects, including its shipment of Nvidia H200 and B200 AI graphics processing unit (GPU) servers starting from the first half of 2025.

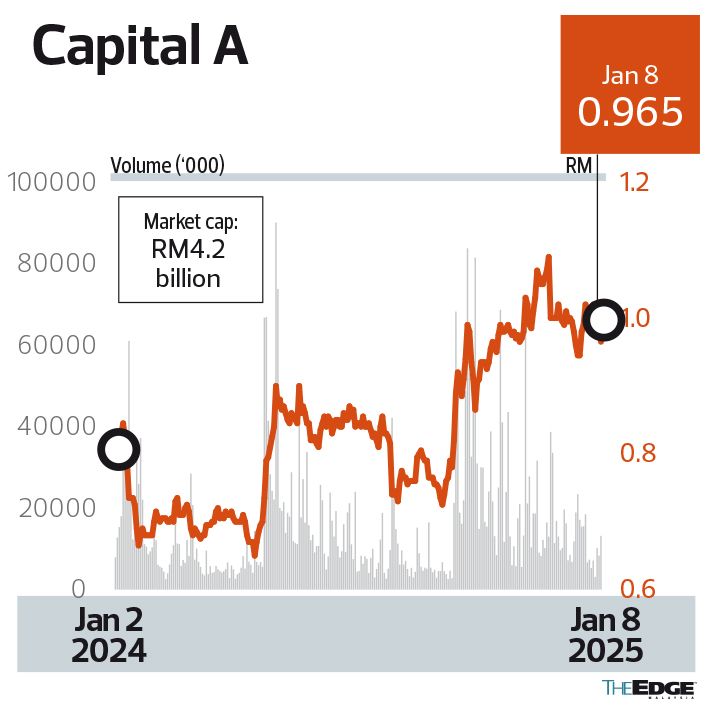

Capital A

Fortress Capital founder and CEO Datuk Thomas Yong:

Capital A Bhd (KL:CAPITALA), controlling a 37% market share in Malaysia’s low-cost airline sector, is undergoing a strategic restructuring to exit PN17 status by divesting its aviation operations to AirAsia X Bhd (KL:AAX) at a valuation of RM6.8 billion. AAX will then transfer its listing status to AirAsia Group (AAG). Post-restructuring, Capital A will retain an 18.5% stake in AAG, which plans to expand its fleet to 242 aircraft by 2025.

Favourable market conditions, including a stronger ringgit, lower oil prices and a balanced supply-demand scenario, are expected to propel AAG’s profitability. Analysts forecast AAG’s profit at RM900 million in 2025, assuming jet fuel at US$100 per barrel and the ringgit at 4.40 to the US dollar. Given that 70% to 80% of AAG’s costs are in US dollars, with jet fuel making up 40% to 50%, earnings are sensitive to these variables. A sensitivity analysis suggests that with the ringgit at 4.35 against the US dollar and jet fuel at US$90 per barrel, AAG’s profit could double to RM1.8 billion, assuming unchanged airfares due to supply constraints.

Beyond aviation, Capital A’s diversified portfolio — including maintenance, repair and overhaul (MRO) through Asia Digital Engineering (ADE), logistics via Teleport, and digital ventures like the MOVE super app and BigPay — adds value to the group’s business operations. ADE alone generated RM61 million in operating profit in 1H2024, with plans to expand from seven to 21 servicing lines in 2025, indicating a significant untapped potential that could lead to a stock rerating as the market currently assigns zero value to Capital A’s non-aviation businesses.

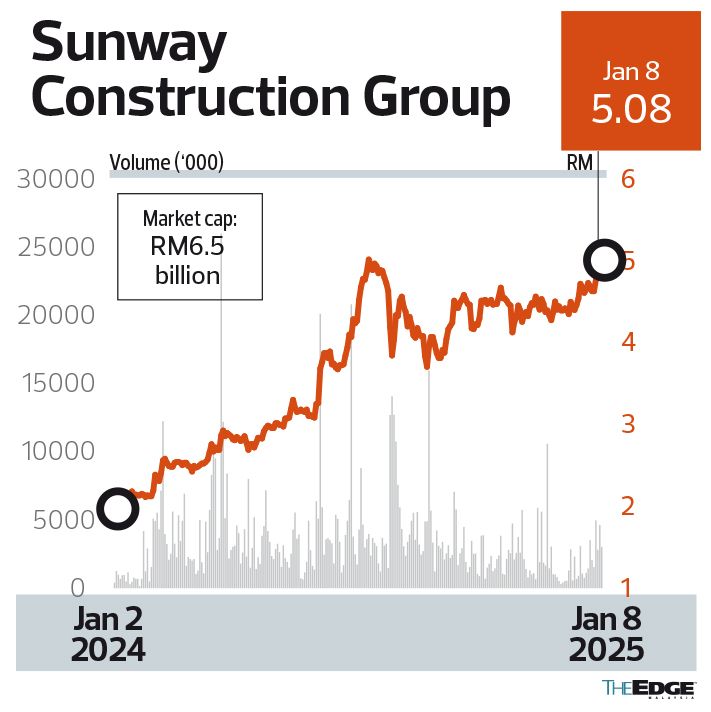

Sunway Construction Group

Fortress Capital founder and CEO Datuk Thomas Yong:

Sunway Construction Group Bhd (KL:SUNCON) is poised to significantly capitalise on Malaysia’s burgeoning DC sector. It is supported by a robust order book of RM7.1 billion as at September 2024, where DCs contributed a significant 54%. Managing five DC projects from four DC clients, SunCon has room for further project upsizing from its existing DC clients. Despite a slowdown in new DC contracts, especially in Johor, due to stringent sustainability checks, Malaysia remains a magnet for major cloud providers like Microsoft, AWS, Google and Oracle with potential investments reaching US$23.3 billion, affirming the sector’s growth trajectory. Knight Frank projects a future potential pipeline of 1.3gw in DC capacity, suggesting a construction market worth RM52 billion.

SunCon benefits from its first-mover advantage in DCs, its vertically integrated operations and a strategic partnership with Engie Services Malaysia, a France-headquartered global group focused on low-carbon energy and services solutions. SunCon’s 73,500 cu m Integrated Construction and Prefabrication Hub (ICPH) in Singapore further enhances its capability in DC construction. With that, the group is well positioned for future awards, especially in Johor as DC capacity there is expected to grow from 10mw in 2021 to 2.7gw by 2027. The post-US election clarity in 2025 could accelerate investment decisions by multinational corporations, enhancing prospects for SunCon, particularly with its active tender book of RM10.6 billion, where DC packages constitute a significant portion. DC projects typically offer quicker turnaround times and higher margins compared to traditional residential or infrastructure projects, as evidenced by SunCon’s 3Q2024 results showing an increase of 0.4 percentage point (ppt) quarter on quarter as well as an expansion of 1.0ppt year on year in profit before tax margin.

With political uncertainties behind it, SunCon stands to leverage this sector’s momentum, potentially securing further contracts beyond DC, in semiconductors and infrastructure like the Penang light rail transit, and solidifying its growth narrative in 2025.

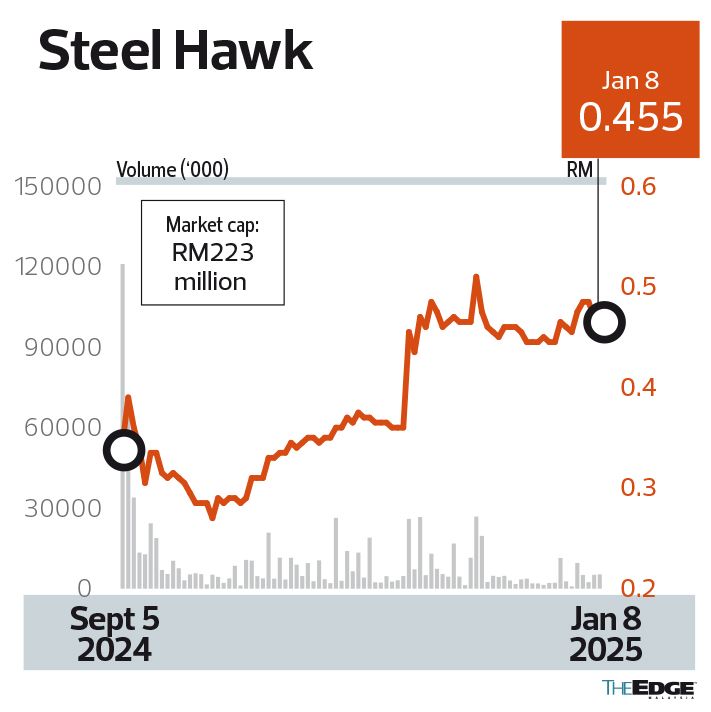

Steel Hawk

Rakuten Trade head of equity sales Vincent Lau:

Having transferred its listing status from the LEAP Market to ACE Market last September, Steel Hawk Bhd (KL:HAWK) is an under-the-radar small-cap oil and gas firm with a good execution track record. Though coming from a small profit base, it is set to grow with the new work packages (estimated to be RM2.5 billion) obtained from Petroliam Nasional Bhd to service Petronas’ downstream operating plant units for the period of 2024 to 2027.

The company already has a good head start in Sabah and Sarawak with licences from Petroleum Sarawak Bhd and an operating team in Sarawak.

The financial performance for the first nine months of 2024 demonstrated significant growth. Revenue increased 19% year on year, reaching RM60 million, while net profit surged 60% to RM9.1 million compared to the same period in the previous year.

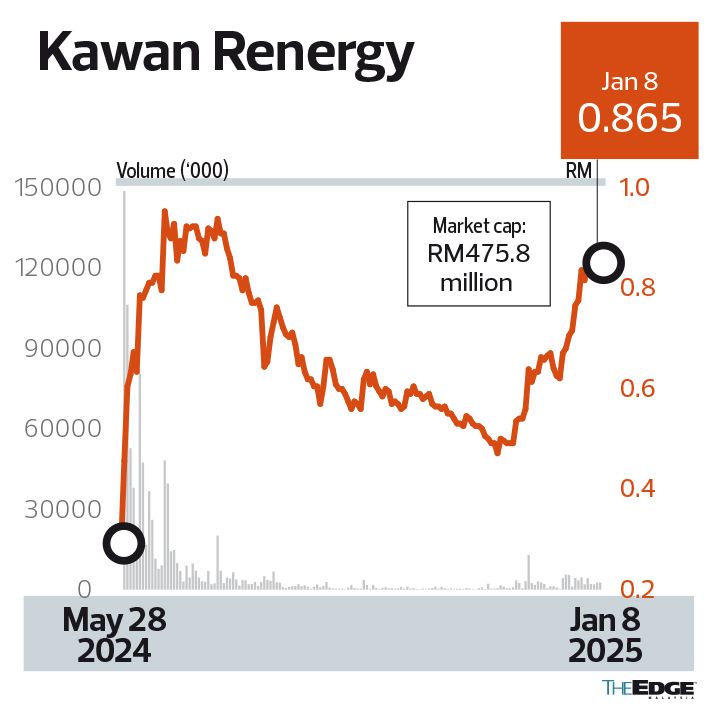

Kawan Renergy

Rakuten Trade head of equity sales Vincent Lau:

The strong inflow of DC investments into Malaysia could benefit Kawan Renergy Bhd’s (KL:KENERGY) co-generation business. Given the high uptime requirement and need for thermal energy from DCs, there could be a need to install a second on-site system to complement the primary source of energy from the grid. The company has received several enquiries on DC-related jobs. However, all these are still in the negotiation stage.

As at Oct 31, 2024, its order book stood at around RM142 million, with higher-margin renewable energy and co-generation plants making up 47%, while the balance came from industrial process equipment (35%) and industrial process plants (18%).

Kawan Renergy has a tender book of RM600 million, with “a lot more in the pipeline” but they have yet to be disclosed due to non-disclosure agreements and early-stage negotiations.

The company reported all-time high earnings for its financial year ended Oct 31, 2024 (FY2024) as net profit surged 44.5% to RM19.22 million compared with RM13.3 million in FY2023.

For FY2025, its key growth driver will be from a growing tender book that is skewing more towards the higher-margin renewable energy space as well as the maiden opportunity to tap the DC theme.

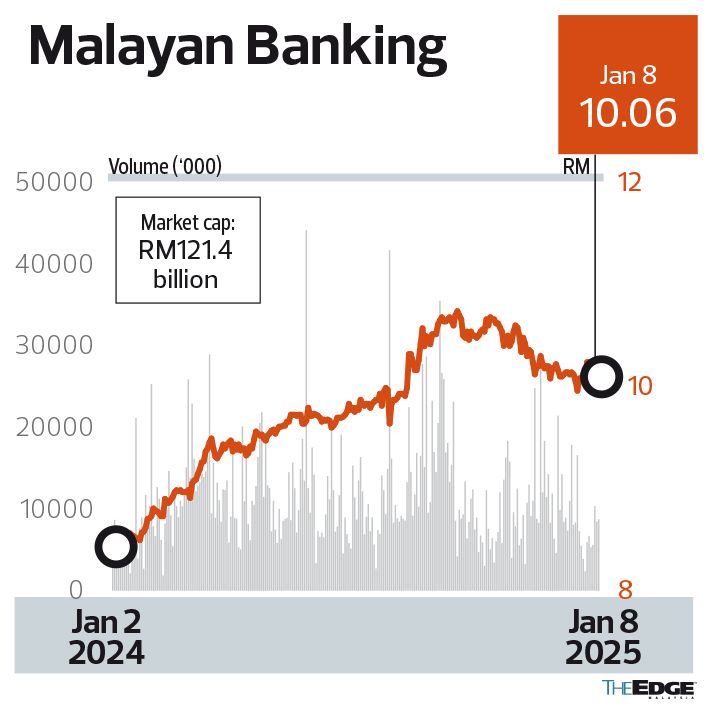

Malayan Banking

MIDF Research head Imran Yassin Md Yusof:

We believe the banking sector will be a beneficiary of Malaysia’s economy, which is expected to continue growing albeit at a more normalised pace. Banks’ loans book is expected to continue expanding, while their asset quality remains stable and improving.

With several banks continuing to maintain their intention to increase dividend payouts, we believe 2025’s dividend outlook remains very bright.

Hence, we like Malayan Banking Bhd (KL:MAYBANK) due to its excellent dividend yield, which is about 6.8%.

For the first nine months of 2024, the bank’s net profit climbed 8.5% to RM7.56 billion. Net fund-based income increased to RM14.66 billion supported by loan growth while non-interest income surged 26% to RM7.49 billion, thanks to its fees and insurance business.

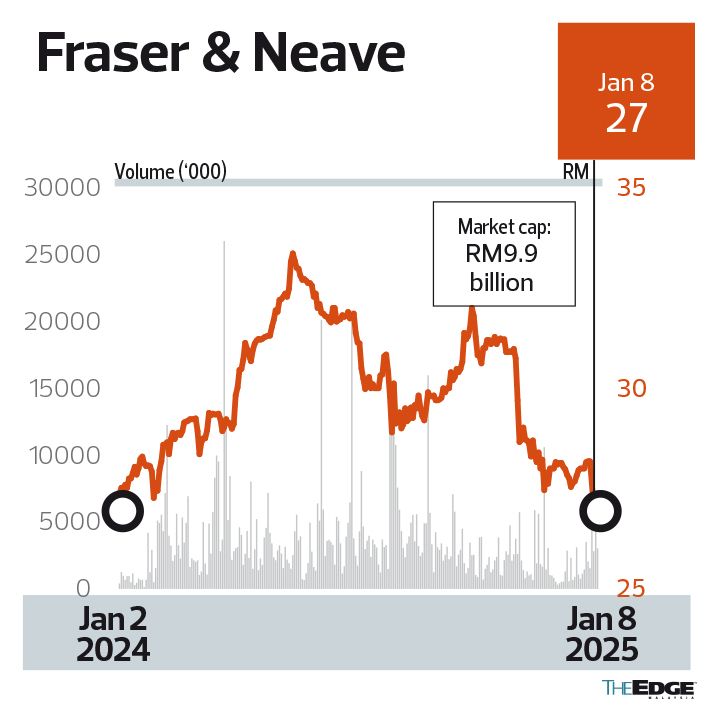

Fraser & Neave Holdings

MIDF Research head Imran Yassin Md Yusof:

We like the consumer sector as a potential laggard play and undervaluation. Fraser & Neave Holdings Bhd (KL:F&N) is well positioned to capitalise on the rising demand for ready-to-go beverages, particularly from increasing tourist traffic. The company’s expansion into integrated dairy farming could further boost its revenue base.

F&N is currently trading at a 2025 price-earnings ratio of 17.4 times, notably lower than both its three-year historical average of 21 times and the sector’s forward three-year price-earnings mean of 28.2 times. This undervaluation, coupled with F&N’s strong fundamentals, presents a rare investment opportunity.

F&N has said that its established operations will continue to generate cash flow and will support the launch of new business units, such as F&N Agrivalley and F&N Foods (Cambodia), despite the temporary delay in milk production at its integrated dairy farm in Gemas, Negeri Sembilan.

The Edge’s picks

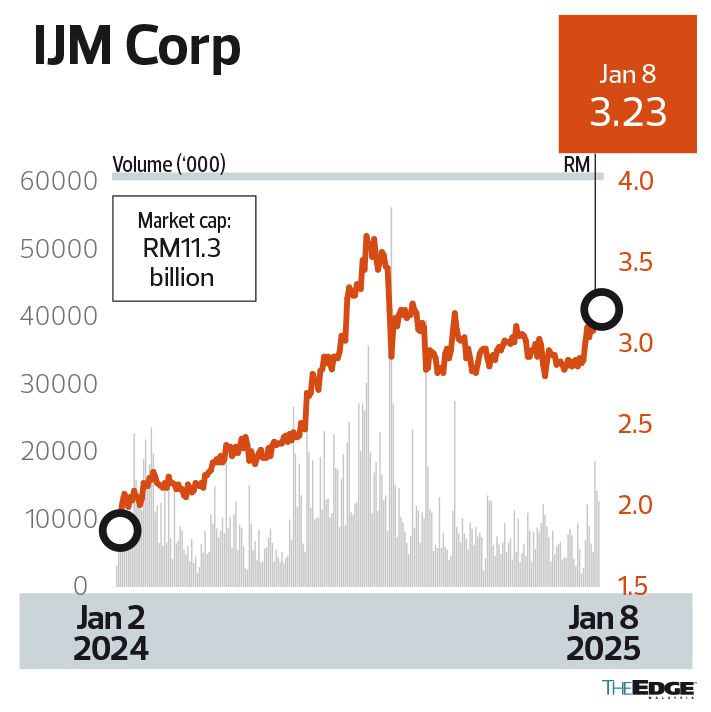

IJM Corp

As the construction boom is expected to continue this year, we may miss the opportunity if we do not have a construction stock in our portfolio.

Compared to its peers like Gamuda Bhd (KL:GAMUDA) and Sunway Construction Group Bhd (KL:SUNCON), IJM Corp Bhd (KL:IJM) appears to be offering a bigger upside potential based on the consensus target price of RM3.67.

IJM is the front runner for a number of large-scale infrastructure projects, with a growing presence in the data centre (DC) space. The group bagged RM2.1 billion worth of new contracts in the first half ended Sept 30, 2024 (1HFY2025), lifting its total outstanding construction order book to RM6.5 billion — equivalent to 3.8 times FY2024 construction revenue. Its property division has RM2.3 billion in unbilled sales.

TA Securities anticipates the group posting stronger earnings in 2HFY2025, driven by higher contribution from the acceleration of three deferred construction projects, all currently progressing at less than 10%. In addition, management’s FY2025 order book replenish target of RM5 billion is expected to underpin further growth.

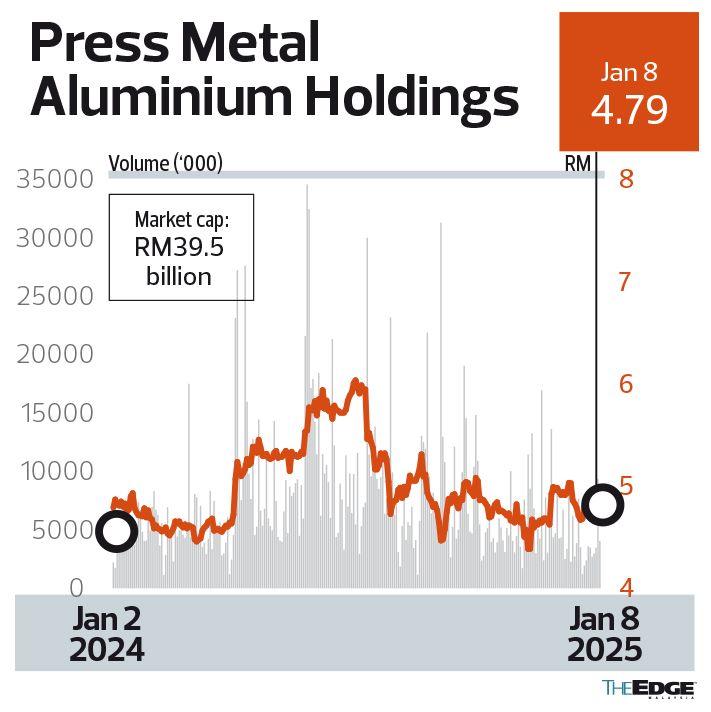

Press Metal Aluminium Holdings

Analysts generally remain positive on the aluminium industry on the back of the recovery in aluminium prices.

RHB Research believes Press Metal Aluminium Holdings Bhd (KL:PMETAL) should benefit from a hike in global aluminium prices, the removal of the 13% tax rebate on aluminium exports by China, and increased demand for aluminium from non-China manufacturers.

The bank-backed research house believes the group is well positioned to capitalise on the potential spillover effects of a heightened US-China trade dispute as well as the growing demand for low-carbon aluminium.

Aluminium prices have fluctuated between US$2,400 and US$2,600 a tonne over the past two months. Kenanga Research says concerns linger regarding the sustainability of Chinese demand as it relies heavily on the recovery of the infrastructure and property sectors, both of which remain uncertain. On the supply side, environmental pressures have led to the shutdown of coal-powered smelters, while Western sanctions on Russian aluminium producers are adding to supply constraints. These factors are likely to influence market dynamics in the near term.

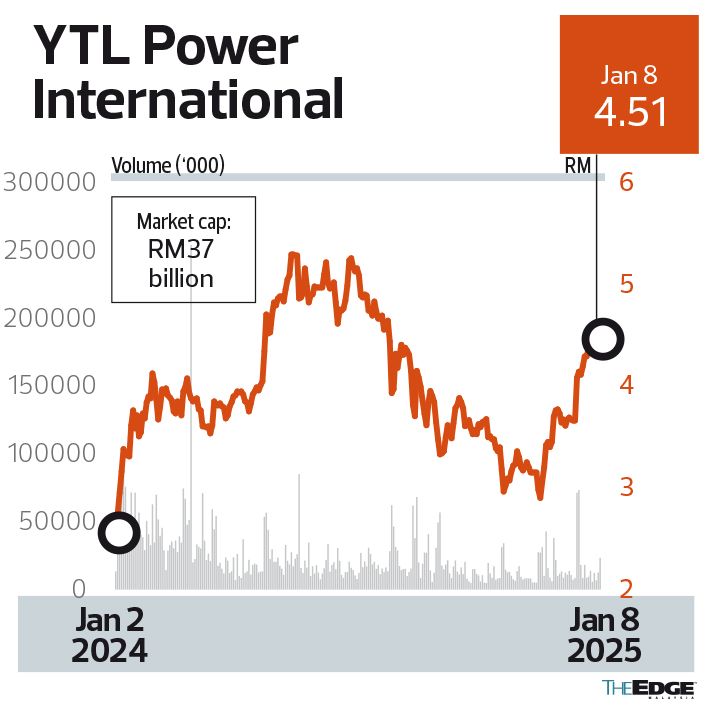

YTL Power International

The Malaysian Anti-Corruption Commission (MACC) has cleared YTL Power International Bhd’s (KL:YTLPOWR) 60%-owned subsidiary YTL Communications of any wrongdoing in connection with the 1BestariNet project, thus removing the overhang on the group. This is evidenced by the strong rebound in YTL Power shares over the past month.

1BestariNet was a project initiated by the Ministry of Education, which sought to provide 10,000 schools throughout the country with high-speed internet access and virtual learning platforms, among others, but was wrought with difficulties.

Of the 14 analysts covering the stock, 13 have “buy” calls on YTL Power, with a consensus target price of RM5.31, which offers quite a decent potential upside. Its 12-month forward price-earnings of 12 times represents a steep discount against its historical PE of 24 times.

TA Securities said the next milestone for YTL Power would be the commissioning of its artificial intelligence (AI) DCs by the middle of this year. Phase 1 to Phase 3 of the group’s DC development are targeted to be completed by the second to third quarters of the year. A total of 48mw co-location capacity is being developed under Phase 1, with SEA Ltd as the anchor tenant that has committed to 32mw take-up.

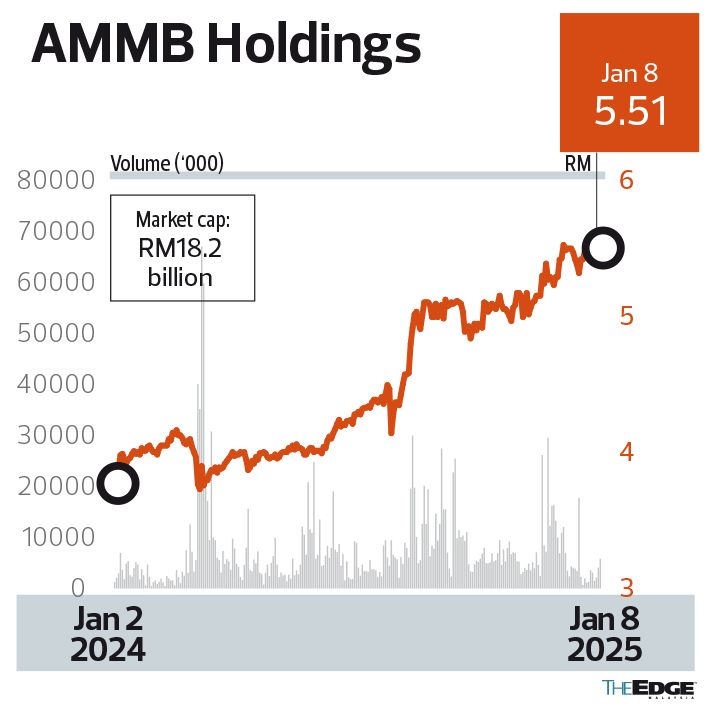

AMMB Holdings

There has been talk of AMMB Holdings Bhd (KL:AMBANK) embarking on a possible merger and acquisition down the road, as its key shareholder and founder Tan Sri Azman Hashim may be amenable to parting with some of his shares if he can secure a good price.

AMMB, the sixth-largest domestic banking group in terms of assets, is currently trading at a forward 12-month price-to-book ratio of 0.9 times, which is lower than the banking sector’s average of 1.2 times.

Kenanga Research sees a more solid return-on-equity backbone in AMMB, which focuses on stronger earnings drivers as opposed to gaining market share in less profitable segments. Also, the group’s newly acquired common equity tier-1 levels of 15% could lead to more generous dividend payouts and make it one of the leaders in yield prospects of 6%. This is premised on the anticipated dividend payout of 50% against the group’s more gradual step up of 45% from 40%.

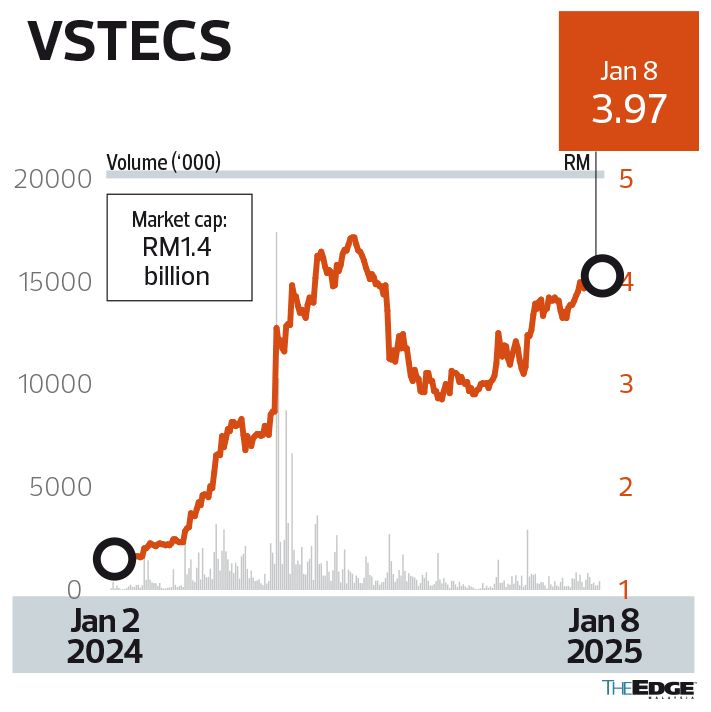

VSTECS

IT hardware and software distributor VSTECS Bhd’s (KL:VSTECS) profitability has grown steadily over the years, reaching RM67.4 million for FY2023 from RM59.7 million a year ago.

In 2024, it secured a series of new distributorships, including key partnerships with Starlink, AWS and Google Gemini, prompting its share price to surge about 200% in the past year.

Despite that, UOB KayHian, the sole research house covering VSTECS, continues to see an upside potential in the stock, giving it a target price of RM5.02.

The government has announced plans for incentives, to be backed by a RM1 billion strategic fund, to cultivate local talent and promote high-value activities in the electrical and electronics and AI sectors. UOB KayHian believes this could be an inflection point for VSTECS, as it will further accelerate its DC equipment and graphics processing unit (GPU) server deals by multiple-fold, growing from the current tens of millions of ringgit.

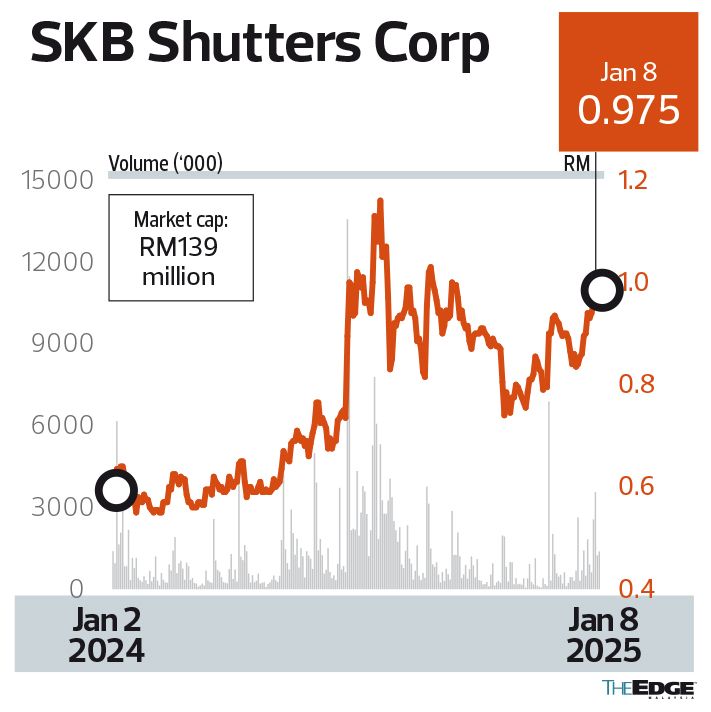

SKB Shutters Corp

Amid the booming DC theme, SKB Shutters Corp Bhd (KL:SKBSHUT) could benefit from the rising number of DC projects in the country. In a recent report, Tradeview Research says the roller-shutter specialist has been supplying its products to DC players, with 20% of its financial year ended June 30, 2023 (FY2023), revenue derived from this segment.

It should be noted that roller shutters and steel doors for DC projects fetch higher margins because of the required product specification with shorter delivery timelines.

Apart from that, the research house says an increase in both domestic and foreign direct investments in the industrial sector bode well for SKB Shutters, which has been the preferred supplier of roller shutters, steel doors and rack systems for major multinational corporations and contractors.

Meanwhile, the rise in infrastructure projects around the region is seen as another catalyst for the company, as it was the supplier for key infrastructure projects such as Mass Rapid Transit (MRT) Lines 1 and 2 in Malaysia, as well as Changi International Airport in Singapore.

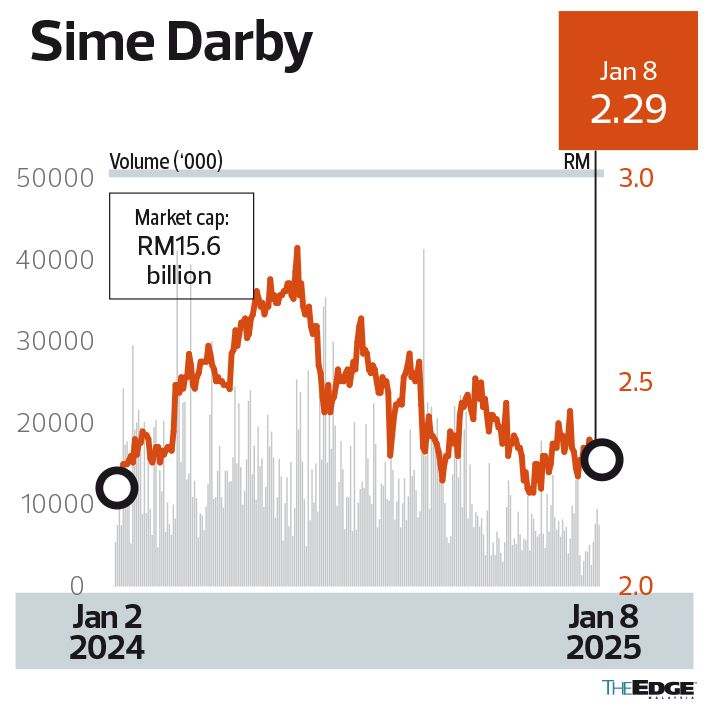

Sime Darby

Shares in Sime Darby Bhd (KL:SIME), which has exposure to both the automotive and industrial equipment sectors, are trading at a 12-month forward PE ratio of below 10 times, according to Bloomberg data.

Since touching nearly RM3 in May 2024, the stock has seen some pullback to close at RM2.29 last Wednesday, with a decent dividend yield of 5.7%.

Operationally, having full control of Umw Holdings Bhd continued to create value for Sime Darby, contributing RM302 million, or 30%, of the group’s core profit before interest and tax for the July-to-September 2024 quarter.

The addition of mass market brands Perodua and Toyota has further strengthened Sime Darby’s presence in the local automotive market, as Malaysia now accounts for 36% of its revenue for the same quarter, against 18% pre-acquisition.

RHB Research says Sime Darby remains its top pick for the sector, underpinned by its robust industrial segment on top of wide-ranging offerings in the local automotive market.

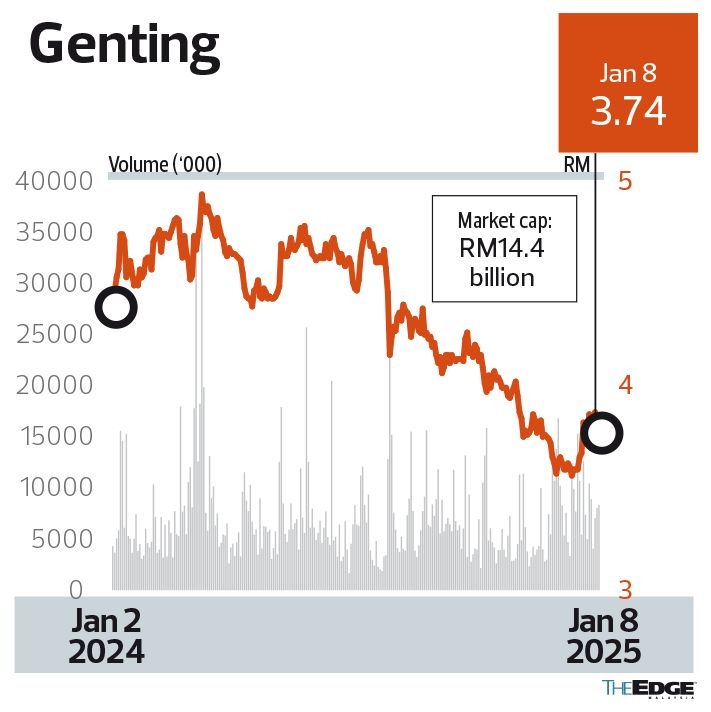

Genting

Genting Bhd (KL:GENTING) was one of the worst-performing big-cap stocks in 2024, as its share price tumbled more than 20%. We believe it is an attractive entry point for investors, given the consensus target price of RM5.13 for Genting. Almost all analysts covering the stock gave “buy” calls.

Genting and its 49.3%-owned Genting Malaysia Bhd (KL:GENM) were removed from the FBM KLCI constituents, following the semi-annual review late last year.

Sentiment on Genting shares has also been affected by the recent negative publicity, including allegations that Genting’s Resorts World Las Vegas LLC had failed to ban criminals from its resort. Also, the casino licence for Singapore’s Resorts World Sentosa was renewed for only two years instead of the usual three, owing to its “unsatisfactory performance” in promoting tourism between 2021 and 2023.

PublicInvest Research notes that as the group’s hospitality businesses are generally dependent on Chinese tourist arrivals, the economic slowdown in China is expected to affect its operations. While visitation should improve over time, the quality of spending has not reverted to pre-pandemic levels.

Nonetheless, the downside risk for Genting seems to be lower for now.

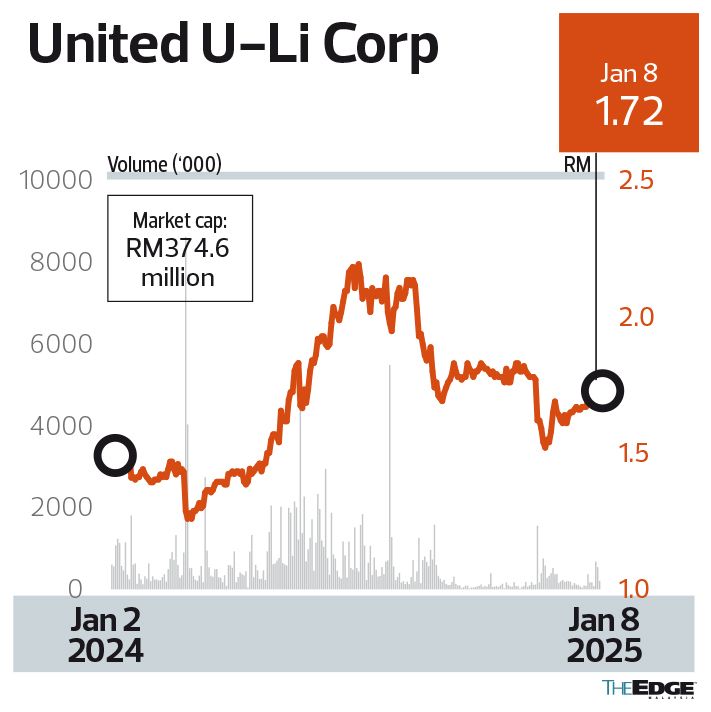

United U-Li Corp

Cable support system provider United U-Li Corp Bhd (KL:ULICORP) is expected to continue to reap the benefits of the ongoing construction boom, including the development of DCs.

Although the company reported a lower net profit of RM23 million for the first nine months of 2024 against RM31.7 million in the same period a year ago, its 2025 net profit is forecast to reach RM50.8 million.

Kenanga Research highlights that the consolidation in the local cable support system market during the pandemic era has led to reduced competition, which augurs well for market leader United U-Li.

The research house says the company’s earnings prospects are strong, driven by strong demand for its cable support systems, both in the private space (such as DCs, warehouses and hospital projects) and public mega projects (ongoing and impending such as the East Coast Rail Link, Johor Bahru-Singapore Rapid Transit System, Bayan Lepas LRT and MRT3).

The stock is currently trading at a 12-month forward PE of 12.3 times, with a dividend yield of 4.7%.

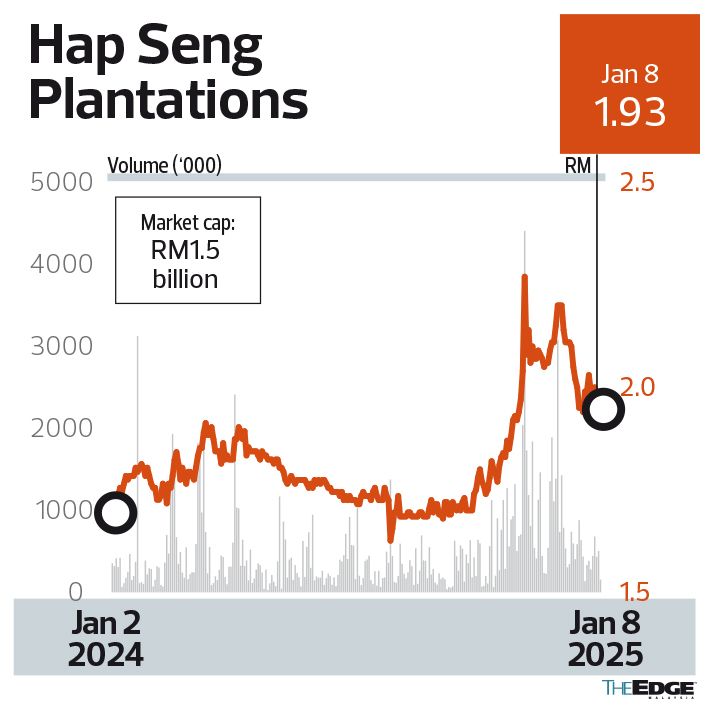

Hap Seng Plantations Holdings

For exposure in the plantation sector and to ride the crude palm oil price (CPO) rally, Hap Seng Plantations Holdings Bhd (KL:HSPLANT) stands out as a better option, mainly because the company is cash-rich and has cheaper valuations. As at end-September 2024, it had RM502 million in net cash.

In addition, the plantation firm is well managed with robust operational statistics — a relatively higher fresh fruit bunch yield of 19.7 tonnes per hectare and an oil extraction rate of 20.75%.

Hap Seng Plantations, which has a land bank of 39,103ha across five estates in Sabah, posted its highest quarterly financial results in nearly three years, with a net profit of RM55.43 million for the July-to-September 2024 quarter, against RM37.8 million a year ago.

CIMB Securities views Hap Seng Plantations as a “pure proxy to rising CPO prices”, as every RM100 per tonne change in the CPO price could shift FY2025’s net profit forecasts by 8%.

Save by subscribing to us for your print and/or digital copy.

P/S: The Edge is also available on Apple's App Store and Android's Google Play.

- Global funds hit pause on Indonesia after Prabowo policy changes

- Embattled billionaire Ong Beng Seng to step down from Hotel Properties

- Trump warns tariffs coming for electronics after reprieve

- Jentayu signs 40-year power purchase agreement for RM2.8b 162MW Sabah hydropower project

- Singapore eases monetary policy as expected, sees weaker growth in 2025

- Sony lifts PS5 price in Europe by 25% ahead of a likely US hike

- Anwar to meet Myanmar junta head in Bangkok

- UK rushes to find materials to keep British Steel plant running

- Majujaya files petition to wind up Bina Puri for failure to pay RM30m awarded by court

- Bursa to keep IPO target of 60 listings this year despite tariff turmoil