This article first appeared in The Edge Malaysia Weekly on January 13, 2025 - January 19, 2025

THE days of “super big profits” once enjoyed by Sime Darby Bhd (KL:SIME) in China’s car market are over, but the automotive and industrial equipment trading company remains confident in its long-term prospects.

Executive director and group CEO Datuk Jeffri Salim Davidson still believes in the long-term outlook for the Chinese passenger car market despite the current headwinds, but he concedes to sleepless nights over the supply glut.

Foreign carmakers, which have dominated China’s car market for decades, are facing problems on multiple fronts, including the rapid rise of China’s home-grown electric vehicle (EV) makers, such as BYD Auto Industry Co Ltd and XPeng Motors.

Sime has not been spared. It is the principal car dealer for automotive brands such as Rolls-Royce, BMW and MINI cars in China. In the July to September 2024 quarter, German luxury carmaker BMW reported an 84% drop in net profit to €476 million as sales in China slumped by a third.

“What happened was we didn’t foresee China becoming an automotive juggernaut. The pace of development by Chinese carmakers was unprecedented,” Jeffri tells The Edge in a wide-ranging interview.

For the first 11 months of 2024, China accounted for a staggering 34.1% of global car sales that reached 82.01 million units, according to the China Passenger Car Association. The US came in second with a market share of 18.2%.

During the pandemic financial year ended June 30, 2021 (FY2021), Sime posted a net profit of RM1.4 billion, up 74% from the previous financial year as Chinese consumers splurged on luxury cars to make up for the months of lockdown and inability to travel overseas.

In FY2022, Sime’s China motor division’s profit was hurt by supply chain disruptions and numerous pandemic-related lockdowns. The group saw net profit fall 23% year on year (y-o-y) to RM1.1 billion.

The situation has become increasingly difficult since then. A debilitating price war in China’s automotive industry, coupled with weak consumer demand, has severely hurt the mainland’s car players. In addition, the country’s EV industry is producing more cars than it can sell domestically.

According to news reports, there are now more than 200 EV manufacturers in China, the world’s largest automotive market. EVs make up more than half of new car sales in the market, propelled by government incentives and fast-expanding charging infrastructure.

This worries Jeffri, 60, whose concerns about the oversupply in China’s car market keep him awake at night.

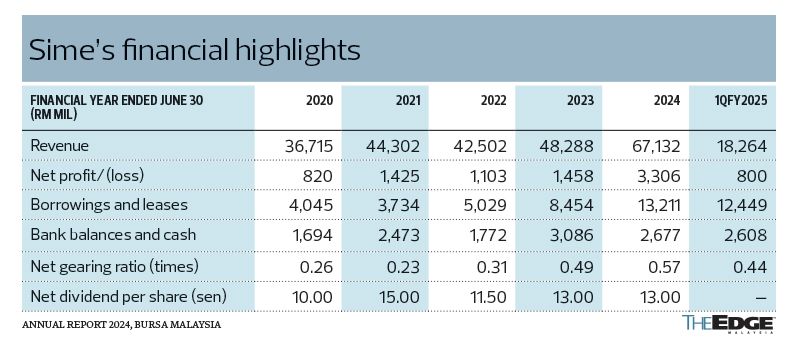

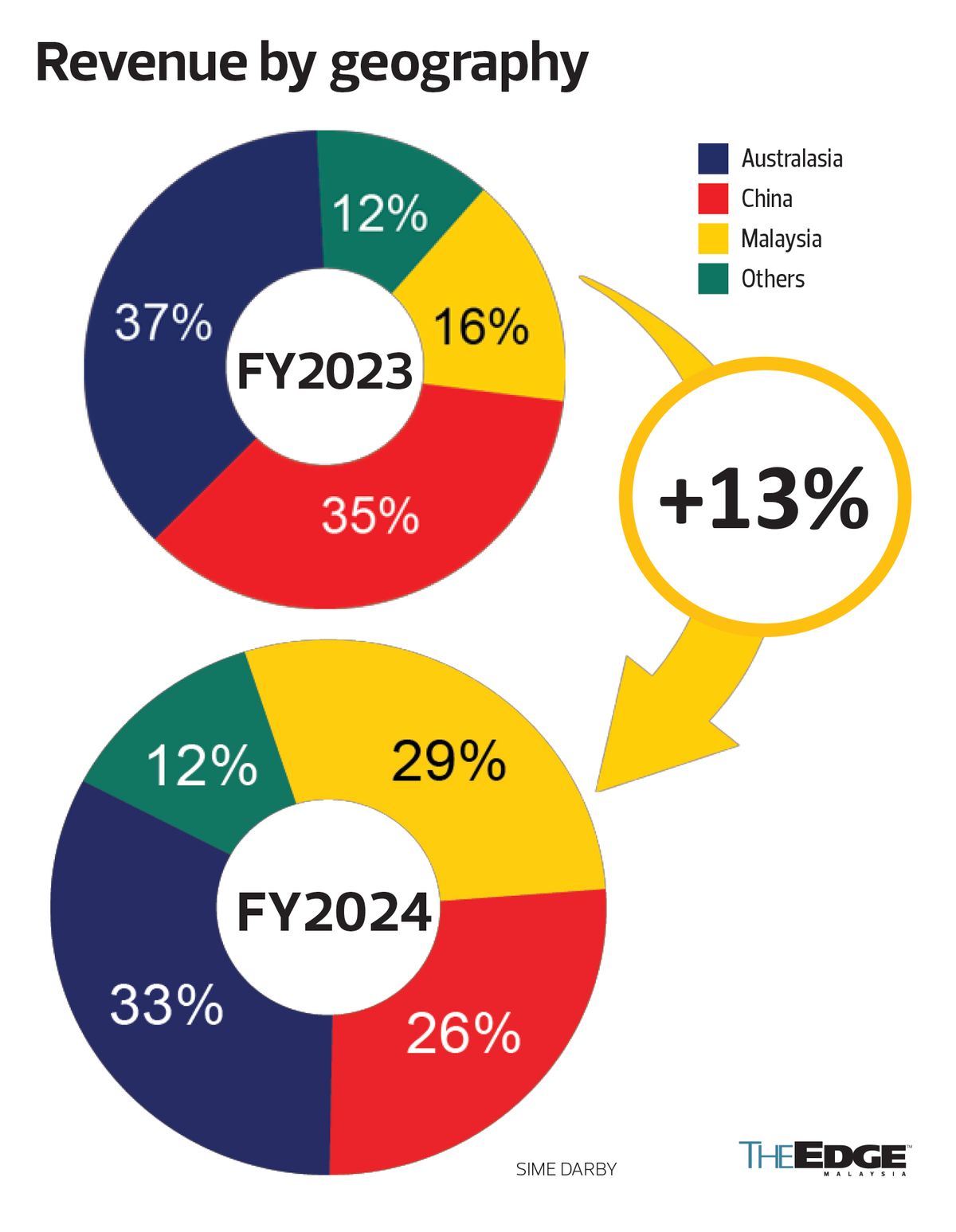

Sime’s motor business in China has been severely affected by the intense competition in the country, which accounts for one-third of the group’s revenue. It contributed 26% of the group’s revenue in FY2024, down from 35% in the previous financial year.

Notably, the motor business in China recorded a loss of RM123 million in FY2024, dragging the group’s motor division profit before interest and tax (PBIT) down by 44% to RM584 million in FY2024, from RM1.05 billion in FY2023.

In announcing its 1QFY2025 financial results last November, Sime said its China motor operations had improved. However, Sime’s motor division PBIT continued to slide in 1QFY2025, falling 6.4% to RM190 million on lower profits from Australasia.

Jeffri points out that while China’s economic growth has weakened, it is still growing at a clip of 5%. “The bigger problem we have in China is the supply-demand imbalance. Demand is holding up and we have been achieving our sales volume targets [set by our franchisors], but Chinese automakers are building too many cars,” he says, noting that the overcapacity has led to industry-wide aggressive discounting, affecting the group’s margins.

Foreign and Chinese carmakers are now grappling with huge oversupply, and experts predict many smaller companies will not survive the fiercely competitive environment. To combat these issues, Chinese carmakers are exporting their vehicles to overseas markets. Because Europe and the US are limiting sales of China-made EVs with tariffs, Chinese carmakers are focusing on Asia-Pacific, South America and Africa.

“The problem is the [profit] margins are gone because of the oversupply and there is a price war/discounting going on [in China]. You get into a situation where you are almost selling the car for nothing. The question is when will the industry recalibrate? We don’t know,” says Jeffri.

Still, car dealers such as Sime are eligible for a rebate on the purchase price conditional on their achieving the sales targets set by the franchisor. This has helped put the group back in the black, says Jeffri. “However, we may never see the big margins like those [enjoyed] three to five years ago again. FY2021 was the best year [for Sime Darby’s motor business in China].”

So, does Sime expect a drop in its China business in FY2025? “Absolutely,” he affirms.

Nevertheless, the group expects its industrial business in Australasia, Malaysia and Singapore and the full-year contribution from its newly acquired UMW division, driven by its mass-market brands Toyota and Perodua, to cushion the weakness in its China operation.

Jeffri is positive on the mining industry in Australia in FY2025, pointing out that minerals will always be needed. “You need metallurgical coal in the production of steel, and copper is a critical mineral for energy transition. Australian minerals are some of the best quality and the cheapest in terms of extraction cost per tonne. We are in a good space.”

The group acquired Cavpower Group, a Caterpillar dealership based in South Australia, in 2023 and stands to gain from the acquisition, as the Australian state has almost 70% of the world’s copper resources.

“We have had a good run over the last few years. Our results are still pretty strong despite the fact that [our motor operations in] China are struggling. Wouldn’t it be nice if China was still firing, together with Australia and UMW?” he remarks.

In 1QFY2025, Sime posted a 36% y-o-y rise in net profit to RM800 million, helped by a one-off gain from the disposal of its Malaysia Vision Valley land in Negeri Sembilan and profit contribution from the UMW division. Revenue for 1QFY2025 amounted to RM18.26 billion, up 31% y-o-y.

Expands brands to include Chinese automakers

As the China oversupply cloud looms over Jeffri, it is now clear to him that his concerns about the emergence of the agency direct sales model were unwarranted. This shift was one of three issues that used to keep him up at night.

“I am very clear now that this was a false worry. The agency model has been tried and tested and the reality of it is that more and more automotive original equipment manufacturers (OEMs) are realising that the traditional dealership model, where they work with a local partner that is close to customers and understands the market, is fundamental. We had a couple of cases in which the carmakers employed the agency model in certain markets, but it didn’t work. So, they shifted back to us. It doesn’t mean that the agency model approach to the sale of new cars won’t come back later, but I am less worried about it,” he says.

Another thing that Jeffri used to fret over was the industry’s gradual transition from internal combustion engine (ICE) vehicles to EVs and how that would affect the group’s after-sales profits.

“I am less concerned about that also. In fact, with hybrids, we have two types of power trains to repair — electricity and gas. In addition, there are still many petrol and diesel cars in the market,” he says.

Sime is not resting on its laurels and has pivoted to securing distribution rights with other automotive OEMS such as BYD in Malaysia and Singapore, and XPeng Motors in Hong Kong. It has also expanded its assembly business in Malaysia through the assembly of Chery vehicles and wheel and door modules for Porsche.

“When BYD came to Malaysia, its first ‘port of call’ was Sime Darby. Why? We have a strong [automotive retailer] reputation, a long history with all our partners and are able to deliver. We have been a Caterpillar dealer for 95 years and in a partnership with BMW for 56 years. We play the long game.

“We also have a professional management team, our governance is strong and our team is international — comprising Australians, Indonesians and Malaysians — simply because our business is spread so far and wide.”

In regards to the rise of used car e-commerce platforms such as Carsome and myTukar (Carro), which are backed by significant capital and have shifted the used car market online, Jeffri observes that Sime has similarly fortified its own used car business.

“That is doing quite well, as we are focused on profit whereas these e-commerce platforms are focused on revenue and market share. Still, we are keeping an eye on them because we are fighting in the same marketplace.”

Sime has positioned itself to participate in the new mobility ecosystem by investing US$3 million (RM13.4 million) in Socar Mobility Malaysia — a joint venture between South Korea’s SK Inc and car-sharing company Socar Inc — and US$5 million in Singapore-based Carro.

No major acquisitions for now

The group, which unveiled a refreshed “Sime” brand last November to reflect its renewed focus on the automotive and industrial equipment sectors, is taking a break from making large-scale acquisitions over the next year or two, after its RM5.8 billion acquisition of 100% equity interest in UMW Holdings Bhd last March.

The takeover resulted in the absorption of UMW’s 51% stake in UMW Toyota Motor Sdn Bhd and 38% share in Perusahaan Otomobil Kedua Sdn Bhd (Perodua).

Jeffri says the group will focus on integrating its newly acquired businesses. “It will now be a ‘digestion period’ for us, making sure all the synergies are extracted and our businesses are running properly.”

He adds that Sime has no plans to increase its shareholding in Perodua for now. Daihatsu Motor Co owns a 25% stake in Perodua; MBM Resources Bhd (KL:MBMR) holds 20%; state-owned investment fund Permodalan Nasional Bhd, 10%; and Japan’s Mitsui & Co, 7%.

“Even if I wanted to buy another 10% from somebody, you need to get everyone else to agree. It [also] needs the Ministry of Investment, Trade and Industry’s (Miti) approval.”

While Jeffri indicates that the group has no plans to undertake another major acquisition like those of Onsite Rental Group, Cavpower Group and UMW in the near future, it would “never say never” to the possibility of yet another such expansion.

“We are always seeking new opportunities. Some will come true, some will not come true,” he says, commenting on a recent report by The Edge that Sime was in talks to acquire an 80% stake in the retail and after-sales businesses of Ingress Corp Bhd — a Malaysian company controlled by privately held Ramdawi Sdn Bhd (88.98%), Datuk Rameli Musa (10.19%) and Ab Wahab Ismail (0.83%).

While Sime’s gearing ratio has increased to 0.57 times as at June 30, 2024, from 0.49 times a year ago, it remains comfortably within the group’s gearing limit of 0.6 times. “It is a conservative limit; so, we still have room to grow. Our cash flow [from operating activities of RM1.23 billion for the three months ended Sept 30, 2024] remains quite strong,” says Jeffri.

The acquisition of UMW solidifies Sime Darby’s leading position in the Malaysian automotive market, while reducing its reliance on the Chinese market — a recurring point of contention among its board members in the past.

Today, revenue by geography is closely balanced between Australasia, China and Malaysia, following the UMW acquisition.

Perodua sold a record 358,102 vehicles in 2024, capturing a 44% share of the country’s total industry volume (TIV) of 814,000 units estimated for the year. Meanwhile, UMW Toyota Motor sold more than 102,300 units last year, accounting for around 13% of expected new-car sales in Malaysia.

“Along with the market share held by the other brands such as Hyundai and BMW of another 4% to 5%, we hold about 60% of Malaysia’s TIV,” observes Jeffri.

In a Dec 26, 2024, report, RHB Research says it is anticipating a softer TIV of 730,000 units in 2025 as the high-base effect kicks in. It sees no compelling factors for 2025 automotive sales to be maintained at the current elevated levels.

Jeffri concurs, predicting that TIV will ease to a more normalised level of between 730,000 and 750,000 units this year, following a faster-than-expected demand recovery after the pandemic disruption.

While the influx of Chinese OEMs and competitive pricing may heighten market competition in Malaysia, he does not foresee the situation escalating to the levels seen in China. “This is where government policies are important. They cannot allow Chinese OEMs to just import thousands of cars and fight here. I think Miti understands that.”

Will EVs continue to grow here? “That is a good debate. If you see the China story, EVs constitute about 50% of the market. But what we are beginning to see is that hybrid cars have been ‘eating’ into the battery-only EV market share in the last few months. What it means is that Chinese consumers are beginning to buy hybrids. If you look at BMW, they have EVs, hybrids and ICE cars. Toyota is betting on hybrids [over EVs].”

Jeffri says that regardless of how EVs, hybrids or ICE cars perform in sales, Sime is well positioned in all three segments.

“The market will decide whether it wants EVs or hybrids, and the manufacturers will decide what cars they want to build based on what they think the market wants. We therefore believe that, while there may be ups and downs in some years, the long-term outlook for our automotive business in Asia-Pacific is positive.

“Asia is seeing a huge, fast-growing middle class. Asia-Pacific’s share of global GDP is expected to be more than 50% in 2050. This is where the growth is. The Chinese in China, in particular, are getting richer and want to buy aspirational products like BMWs. So, I think we are in the right place.

“China remains the world’s largest consumer market. We remain long-term bullish on its growth prospects, though we expect conditions to remain difficult in the next year. There will be blips along the way but, in the long run, it will be quite strong.”

Why the market is not pricing in Sime’s industrial segment and UMW acquisition

Ten months after its RM5.8 billion acquisition of UMW Holdings Bhd to create the country’s largest automotive group, the share price of Sime Darby Bhd (KL:SIME) is trading at a low valuation compared with industry peers such as DRB-Hicom Bhd (KL:DRBHCOM).

Sime is trading at 9.83 times its one-year forward price-earnings ratio (PER), compared with DRB-Hicom’s forward PER of 11.93 times. As DRB-Hicom, which has brands like Proton, Honda, Mitsubishi and Isuzu under its stable, is a much more diversified conglomerate than Sime, it should also be compared with listed automotive players. A look at three other automotive stocks shows that MBM Resources Bhd (KL:MBMR) is trading at a forward PER of 7.79 times and Bermaz Auto Bhd (KL:BAUTO) has the lowest forward PER of 7.26 times (see table). Tan Chong Motor Holdings Bhd (KL:TCHONG) is currently loss-making.

Post-acquisition, Sime’s share price has shown lacklustre performance, despite commanding a 60% share of Malaysia’s total industry volume (TIV). In the last one year, its shares are down 2% compared with the benchmark FBM KLCI’s 8.6% gains. It hit a six-year high of RM2.95 in May 2024 but has since erased those gains to close at RM2.29 on Jan 8. At the day’s closing price, the group was valued at RM15.61 billion.

Sime has continued to pay out dividends despite the challenges in its automotive business, especially in China, where there has been heavy discounting due to oversupply. It paid a total dividend of 13 sen per share for the financial year ended June 30, 2024 (FY2024), translating into a dividend yield of 5.7%, based on the latest closing price.

Factors behind the stock’s underperformance

Sime executive director and group CEO Datuk Jeffri Salim Davidson believes a reason for the stock’s performance is intense competition in China’s car market, which has affected the group’s motor business.

“One is the concern about China’s story, and there is a worry about its impact on our results. Another is perhaps we have not done a good job explaining to analysts and investors Sime’s potential,” Jeffri tells The Edge in an interview.

He notes that while Malaysian analysts are well versed in the local automotive industry, they may not have fully grasped the group’s exposure to strong growth in the mining sector, leading to an underestimation of the potential of its industrial business. “As Asia-Pacific grows, demand for infrastructure and construction will intensify. Development in the region will also spur demand for commodities and mining services,” he says, noting that Sime has become Caterpillar’s second-largest dealership group in the world by volume, with operations in Malaysia, China, Australia and New Zealand.

“We need to do a better job at explaining to the market. Our revenue by geography has been closely balanced between Australasia, China and Malaysia, following the UMW acquisition … While one piston [motor division in China] is not firing well, the other two [its motor operations in Southeast Asia, especially Malaysia, and its industrial equipment and automotive trading business in Australia] are still strong and will drive the business forward,” he says.

Post-acquisition, Sime has three main business segments: industrial, motor and UMW. Jeffri stresses that the group should be seen as both an automotive and industrial player.

The acquisition of UMW was a strategic move to further scale up and strengthen the group’s presence in the Malaysian automotive sector, adding Toyota and Perodua to its portfolio.

Nevertheless, 13 of the 16 analysts covering Sime have a “buy” recommendation and only three have a “hold” call. The consensus 12-month target price is RM2.88, implying a potential upside of 26% from last Wednesday’s closing price of RM2.29.

Jeffri admits that there is a “disconnect” between the expectations of analysts and fund managers.

Another factor affecting sentiment could be unmet expectations for a large dividend payout in FY2024, following its sale of Ramsay Sime Darby Healthcare Sdn Bhd (RSDH) for a significant gain on disposal of RM2 billion, he notes. “But we had made it very clear right from the beginning that proceeds from the sale would be used to fund the UMW acquisition.”

Its dividend per share of 13 sen for FY2024 was unchanged from FY2023.

Analysts positive on Sime despite market hesitation

According to Bloomberg consensus, Sime is expected to register a net profit of RM1.69 billion on revenue of RM72.32 billion for FY2025. In FY2026, its net profit is expected to rise 4.73% to RM1.77 billion on revenue of RM73.98 billion.

Sime closed FY2024 on a strong footing, with its net profit more than doubling to RM3.31 billion, from RM1.46 billion in the previous financial year, owing largely to the RM2 billion gain from the disposal of RSDH. Revenue rose 39% year on year to RM67.13 billion.

Stripping out the one-off item, the group posted core net profit of RM1.3 billion in FY2024, up 14% from FY2023, on higher profits from its industrial business in Australia, the strong performance of the motor businesses in Malaysia, Singapore and Taiwan, as well as the maiden profit contribution from the UMW division.

In 1QFY2025, Sime posted a 36% y-o-y rise in net profit to RM800 million, helped by a one-off gain from the disposal of its Malaysia Vision Valley land and profit contribution from the UMW division. Its revenue for 1QFY2025 amounted to RM18.26 billion, up 31% y-o-y.

“FY2025 would be the first year for Sime to capture full-year contributions from UMW, and we expect stronger contributions in the upcoming quarters, especially from Perodua,” says CGS International in a Nov 28, 2024 note. It has an “add” recommendation on the stock, with a target price of RM3.60.

“While 1QFY2025 results made up 19% of our and consensus FY2025 estimates, we expect stronger contributions in coming quarters led by UMW. We believe the market continues to underestimate the significant margin upside to UMW from the ringgit’s appreciation against the US dollar, while industrial demand is stable,” it adds.

UMW holds about 60% of Malaysia’s TIV, with the Malaysian Automotive Association recently revising the 2024 TIV forecast upwards to 800,000 units, from 760,000 previously, the research firm says.

CGS International is forecasting higher car sales volumes for the group’s 2QFY2025 and 3QFY2025, supported by year-end sales campaigns and festive season demand in the first quarter of this year.

Sime’s industrial division is expected to deliver stable earnings, supported by a robust order book of RM798 million in Australia as at October 2024, it says.

In a Nov 29, 2024, report, BIMB Securities Research says the industrial segment benefits from resilient commodity demand and the resultant increase in mining activity, sustained mining fleet utilisation, and a new RM798 million mining truck contract secured in Australia in October 2024. The local research firm maintains a “buy” call on Sime, with a lower target price of RM2.60, from RM3 previously.

RHB Research projects that Sime will deliver an annual net profit of RM1.57 billion in FY2025, rising to RM1.61 billion in FY2026 and RM1.62 billion in FY2027. The revision reflects an upward adjustment to its FY2025 and FY2026 earnings estimates by 2%, after accounting for a higher 2025 Perodua sales volume forecast of 330,000 units, up from 310,000 units.

“We expect the industrial division to post strong numbers in line with robust commodity demand. Though demand for coal from China is expected to fall because of falling steel prices, Australia has diversified its export of metallurgical coal, with India, Japan, and South Korea as its main customers. In Malaysia, the motor segment is expected to remain strong, supported by an anticipated uptick in electric vehicle sales before the tax holiday expires at end-2025 while Perodua continues to be Malaysia’s favourite car brand,” says RHB Research in a Nov 29, 2024, note. It reiterates a “buy” call on Sime, raising its target price to RM3.15, from RM3.10 previously.

Save by subscribing to us for your print and/or digital copy.

P/S: The Edge is also available on Apple's App Store and Android's Google Play.