Bloomberg filepix for illustration purpose only.

KUALA LUMPUR (Jan 7): Maybank Investment Bank (Maybank IB) expects a de-rating for the Malaysian oil-and-gas sector, given the high possibility of capital expenditure reduction by Petroliam Nasional Bhd (Petronas) in 2025.

The house said potential cut in capital expenditure could delay upstream exploration and production (E&P) projects, resulting in slower growth for oil & gas service and equipment (OGSE) companies.

Consequently, the research firm prefers defensive plays, especially mid-stream and floating production storage and offloading (FPSO) players, over OGSE counters, while advising investors to avoid petrochemical stocks for 2025.

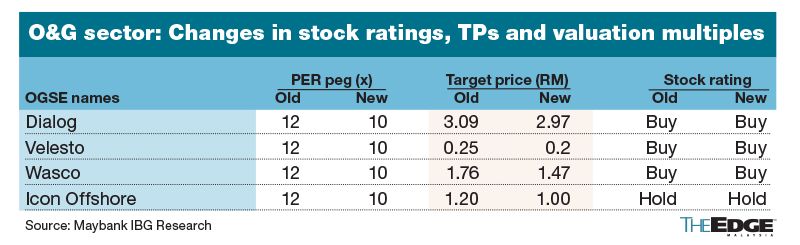

Also, Maybank IB lowered its target price-to-earnings multiple to 10 times (from 12 times currently) for all oil-and-gas stocks under its coverage, translating into lower target prices for each stock (see table).

Petronas’ capex cut to result in slower growth for OGSE players

Potential capital expenditure (capex) reductions could delay upstream exploration and production (E&P) projects, resulting in slower growth for OGSE companies, said Maybank IB in a note on Tuesday.

This follows the shift of control of Sarawak’s natural gas resources away from Petronas to Petroleum Sarawak Bhd (Petros), impacting the national oil-and-gas company’s revenue stream and free cash flows.

“...although we are unable to quantify the impact. We believe that a Petronas capex deferral is a possibility, as a significant portion of its trading revenues have likely been lost,” Maybank IB said.

In the past, local-centric OGSE players’ revenues were generally positively correlated with Petronas’ capex spending, it said.

“For instance, the aggregate OGSE players’ revenue mirrored the fall in capex spending in 2016, 2017 and 2021.

“Applying what we have observed in the past, we flag that there is a possibility that many local-centric upstream OGSE names may see slower growth/need a reset in growth expectations in 2025E (estimate), due to the ongoing industry development,” the house added.

Maybank IB noted that Petronas’ earlier plans to spend RM300 billion in capex over the next five years (2023-2027E), may not materialise, given the current circumstance it is facing with Petros.

FPSOs in ‘golden age’, avoid petrochem sector

Given the recent developments in the sector, the house prefers defensive stocks, particularly mid-stream players and FPSOs, which are expected to ride on the global deep and ultra-deepwater capex investments.

Also, the house forecasts Brent crude oil prices to average US$70/barrel (bbl) in 2025, reflecting a decline from US$80/bbl in 2024 as a surplus in supply, and exerting downward pressure on prices.

This follows the Organization of the Petroleum Exporting Countries (Opec+) plans to increase crude oil production by 2.2 million barrels per day, starting April 2025.

FPSO systems are expected to drive offshore oil-and-gas production, with an annual average of 10-11 project awards projected until 2030, the house noted.

“We think the FPSO market is currently in the ‘golden age’ due to a robust global tender pipeline — with an expected 60 awards from 2024-2028E,” Maybank IB said .

The house believes that this “golden age” for FPSOs presents opportunities for Malaysian companies like Yinson Holdings Bhd (KL:YINSON)(“Buy”, target price/TP: RM4.78) and Bumi Armada Bhd (KL:ARMADA)(“Buy”, TP:71 sen), given their strong positioning in deepwater and ultra-deepwater markets.

Meanwhile, Maybank IB named Dialog Group Bhd (KL:DIALOG) as its top pick from the mid-stream sector, as it forecast record high earnings of RM714 million (+17% year-on-year/y-o-y) for the group in FY2025.

“We still like Dialog, as the group may benefit from: i) ChemOne’s development of Pengerang Energy Complex (PEC); and ii) Petronas’ RM6b development of a 650,000 biorefinery with Enilive and Euglena, with the need for tank terminals for LT (liquid tanks) storage of refined/crude products,” it added.

At noon break on Tuesday, Yinson and Bumi Armada shares were unchanged at RM2.68 and 66.5 sen respectively, while Dialog slid one sen or 0.5% at RM1.86, valuing the group at RM10.5 billion.

Petrochemical ASPs have bottomed

Maybank IB believes that the petrochemical sector has found a bottom in terms of average selling prices (ASPs).

“...the sector appears to be in an L-shaped recovery.

“Coupled with additional polymer capacities coming onstream regionally in 2026, it is unlikely that the industry will revisit its ASP highs in 2021 and 2H2022 anytime soon,” it added.

The house also views that the worst is not over for Petronas Chemicals Group Bhd (KL:PCHEM).

“... we expect the group to rake in y-o-y decline in FY2025E profits, post-incorporation of PPC’s (Pengerang Petrochemical Company Sdn Bhd) losses of >RM700m (million) annually; and ii) PE (polyethylene)-naphtha spreads are not wide enough for Lotte Chemical Titan Holding Bhd (KL:LCTITAN) to turn profitable. We have a ‘sell’ rating on both PCHEM and LCTITAN.”

At noon break on Tuesday, Petronas Chemicals shares settled four sen or 0.8% higher at RM4.93, valuing the group at RM39.4 billion, while Lotte Chemical’s shares slipped one sen or 1.6% at 62.5 sen, translating into a market capitalisation of RM1.4 billion.

- China suppliers mock tariffs with Nike, Lululemon deals on TikTok

- Malaysia declares state funeral for Tun Abdullah Ahmad Badawi

- Reach Energy, Cahya Mata, Able Global, Pestec, Bina Puri, Jentayu Sustainables

- Yellen says sell-off in Treasuries shows US confidence loss, not dysfunction

- Nvidia to produce AI servers worth up to US$500b in US over four years