KUALA LUMPUR (Jan 2): HLIB Research, an equity research arm of Hong Leong Investment Bank, is not that upbeat about banking stocks, although the sector’s valuation is reaching its lowest point in five years.

Currently, the sector is inexpensive when stacked against its five-year mean pre-pandemic price-to-book (P/B) ratio, but is pricey versus regional peers, according to HLIB.

“We only get excited if there are price dips to buy on weakness,” said HLIB, noting that it would be difficult for banking stocks to outperform the broader market in the first half of 2025.

“This is because the sector will still need to contend with seasonal deposit rivalry for at least one more quarter, and we have to wait for February’s reporting season to get hold of FY2025 NIM (net interest margin) guidance,” it commented in its latest research note.

Furthermore, HLIB commented that with US President Trump coming into office, emerging markets may be in for a bumpy ride, as investors digest the actual rollout of his “America First” policies.

“Not forgetting, the valuations of local banks are relatively pricier than their regional counterparts. Besides, dividend yield of the banking sector is currently (circa) c.5% and the yield spread differentials vs risk-free instruments like 10-year MGS/US treasury are 160bp/80bp respectively,” said HLIB.

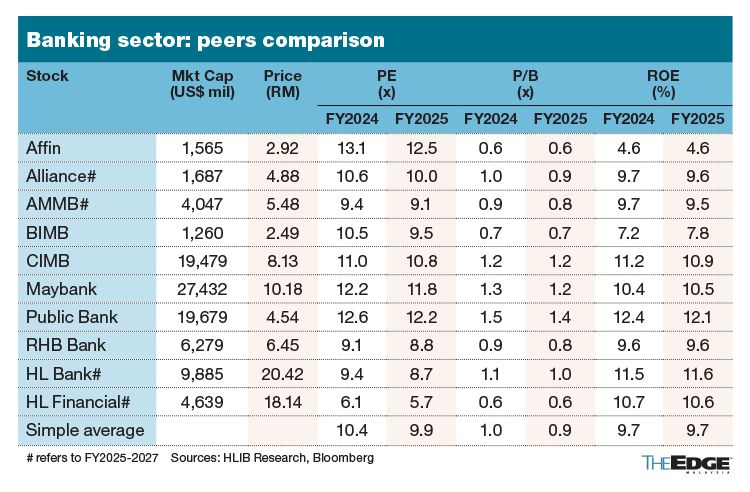

HLIB, which has a “neutral” call on the banking sector, deems banking stocks as attractive only if they are trading at less than one time P/B value, and below 10 times price-to-earnings (P/E) multiple.

Based on HLIB data, banks that meet the criteria are RHB Bank Bhd (KL:RHBBANK), Bank Islam Malaysia Bhd (KL:BIMB), AMMB Holdings Bhd (KL:AMBANK), Hong Leong Bank (KL:HLBANK), and Alliance Bank Malaysia Bhd (KL:ABMB).

Its top picks for the banking sector are RHB Bank and AMMB.

HLIB recommends RHB, with a target price of RM7.30, for its attractive yield of more than 6%. It sees RHB as “an affordable KLCI index banking component”. Additionally, it said RHB’s elevated CET1 ratio which creates scope for capital management, or to grow the bank at a faster clip.

HLIB pegs the target price of AMMB at RM6.15. It is the top pick because of the banking group’s five-year “Winning Together” strategic plan that has shown a lot of promises so far (two successive quarters of good financial results), and a long runway to dish out more dividends, said the research outfit.

While being cautious on the outlook, HLIB concurs with the consensus view that the banks will experience a recovery on NIM, decent credit growth, and a chance for pre-emptive provision write-backs.

HLIB projects a flattish non-interest income (NOII) growth of 4% in 2025, a significant slowdown compared to the robust 9% in 2024.

Although 2024 was on track to ink robust NOII growth, HLIB said it is “sceptical that this tempo can be kept, given the historical volatility of treasury gains.

In terms of asset quality, HLIB expects stability due to strong economic conditions, reflected by a 40 basis points (bps) half-year improvement in Stage 2 household loans, and a 30bps decrease in missed repayments by small and mid-sized enterprise (SMEs).

While there are encouraging prospects for pre-emptive provision write-backs, HLIB anticipates that banks may choose to retain these provisions as a buffer against potential economic headwinds.

Consequently, HLIB anticipates net credit costs (NCC) to remain relatively stable at 22–23bps in FY2025 and FY2026, comparable to the estimated 2024 levels and within the pre-Covid-19 run-rate of 24bps.

- Mr DIY founder Tan Yu Yeh relinquishes vice chairman post, to serve as adviser

- 50,000 Malaysian jobs at risk, business chamber warns as it calls for urgent US tariff mitigation council

- Malaysia refutes 47% US import tariff claim, takes measures to prioritise well-being of businesses and people

- Trump hits China tariff retaliation, says policy will remain

- China retaliation on US farm goods hits soybeans, bolstering Brazil

- ‘Worst-case scenario’ for tech wipes $1.4 trillion from Nasdaq

- Anwar says impact of latest US tariff on nation's economy still being assessed

- Tok Mat, Rubio discuss bilateral relations, Asean-US Special Summit date

- US solar’s hoarding habit will help blunt sting from Trump tariffs

- Wall Street rout drags Nasdaq near bear market