This article first appeared in Capital, The Edge Malaysia Weekly on December 30, 2024 - January 12, 2025

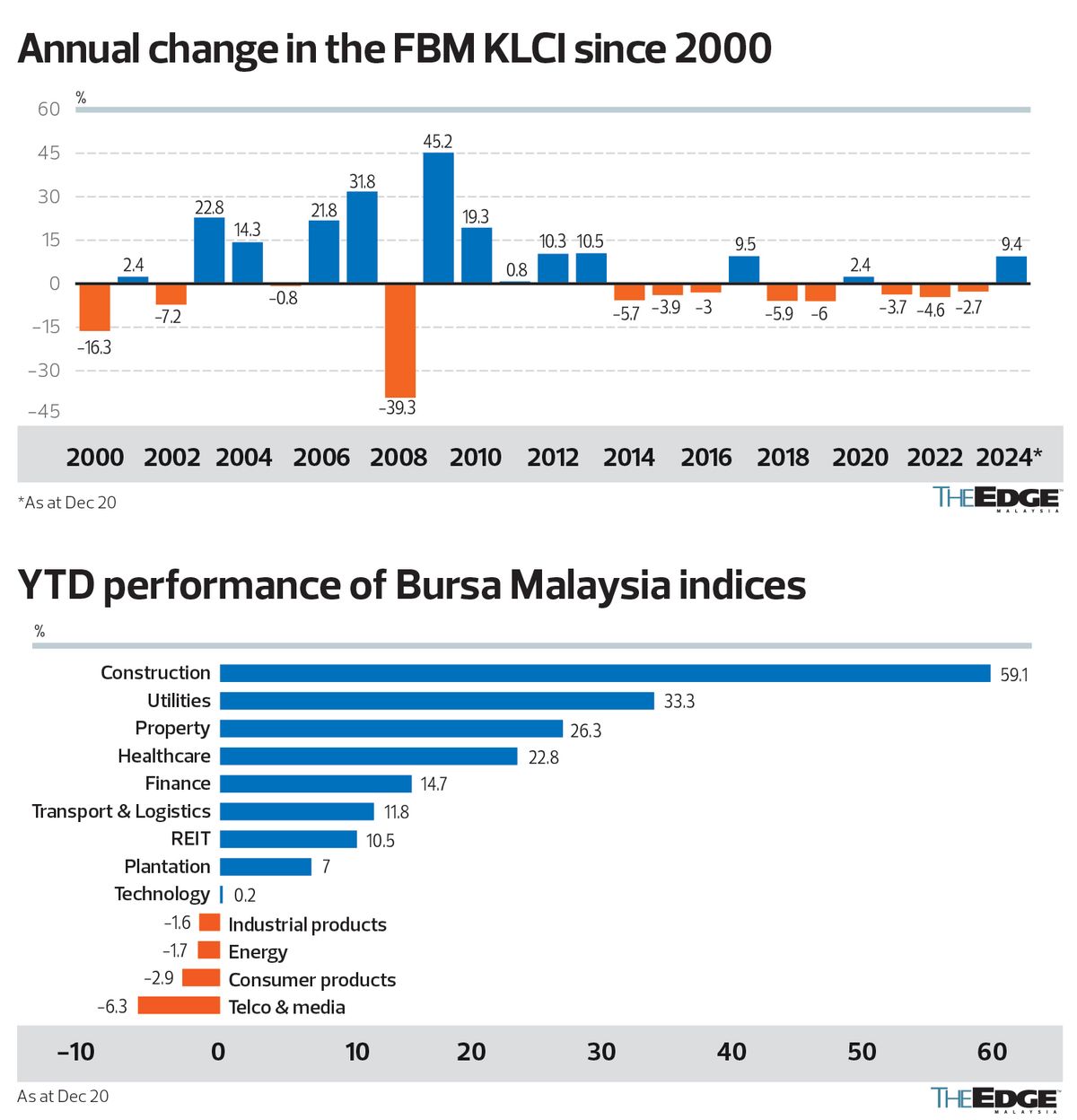

THE year 2024 was a turning point for the Malaysian equity market. After three consecutive years of negative returns, the benchmark FBM KLCI finally delivered its first annual gain in 2024, emerging as one of the best-performing markets in the region.

The 30-stock index closed at 1,591.41 points on Dec 20, rising 9.4% year to date (YTD), against a 2.7% decline in 2023. Its performance also fared better than the FBM Small Cap Index’s 7% increase and the FBM ACE Market Index’s 1% decline so far this year.

The market rally and risk-off sentiment pushed the local bourse’s total market value to breach RM2 trillion for the first time in May, driven by broad gains in blue-chip stocks and a slew of new listings in recent years. As at market close on Dec 20, the local bourse’s market value was at RM2.025 trillion.

Foreign investors have turned more positive on Malaysia, convinced by the country’s push towards artificial intelligence data centres and the increased foreign direct investment (FDI) commitments in the semiconductor industry. The latter includes German semiconductor giant Infineon Technologies AG’s plan to invest an additional €5 billion (RM23 billion) in constructing the world’s largest 200mm silicon carbide power fabrication plant in Kedah.

For the first nine months of this year (9M2024), Malaysia approved investments totalling RM254.7 billion, representing an increase of nearly 11% compared with the same period last year.

All these positive developments, which also include much-needed policy reforms such as subsidy rationalisation, led to a strong inflow of foreign funds totalling RM3.6 billion in 9M2024.

During the October-December period of this year, however, the market saw the exit of a net RM6.5 billion due to external jitters from Trump 2.0, erasing the earlier net inflows, which resulted in a YTD tally of RM3 billion in net outflows, according to Hong Leong Investment Bank (HLIB) Research. Over the past decade, foreign net inflows in Malaysia only occurred in 2017 (RM11.3 billion) and 2022 (RM4.7 billion).

That said, the research house believes the slide in foreign equity holdings has likely bottomed out and should see a recovery on the back of the US Federal Reserve’s ongoing rate reduction, which should encourage inflows to emerging markets, including Malaysia.

“In addition, Malaysia is witnessing a rejuvenated domestic scene — which we reckon foreigners have yet to fully appreciate — backed by sustained growth, record approved investments and subsidy reforms in motion, alongside a more stable political landscape,” HLIB Research says in a Dec 23 note, forecasting an 8.3% growth for the FBM KLCI in 2025 in anticipation of earnings momentum gathering pace.

Malaysia’s equity market saw positive rating revisions by foreign research houses in 2024 amid the strengthening of the ringgit and robust foreign fund inflows. After six years, JP Morgan finally upgraded Malaysia’s rating to “neutral” from “underweight”, which it attributed to policy reforms, data centre investments and a significant infrastructure buildout.

Nomura Global Markets Research also revised upwards its call on Malaysian stocks to “overweight” from “neutral”, as part of its equity strategy call that US rate cuts will stoke a rally in emerging markets.

While market volatility is expected to heighten in the first half of next year (1H2025) as investors grapple with Trump’s confrontational “shoot from the hip” style, HLIB Research sees calmer waters in 2H2025 once it becomes clearer that Trump isn’t going all guns blazing with tariffs, but is instead taking a more targeted approach.

The research house is “overweight” on the aviation, construction, consumer, gaming, healthcare, property, renewable energy and utilities sectors.

The FBM KLCI touched its recent peak of 1,678.8 points in August — the highest since December 2020 — with several banking stocks hitting their record highs, including Malayan Banking Bhd (KL:MAYBANK) and RHB Bank Bhd (KL:RHBBANK) as they were the key beneficiaries of the renewed foreign interest, coupled with banks being a good proxy for the economy.

Sector-wise, construction has been the best-performing sector in 2024, with a rise of 59.1%, followed by utilities (+33.3%), property (+26.3%), healthcare (+22.8%) and finance (+14.7%).

However, telecommunications and media posted a negative return of 6.3%, along with consumer (-2.9%), industrial (-1.6%) and energy (1.7%).

Worth noting is that the technology sector’s performance has been flat (+0.2%), partly due to a stronger ringgit, which has weighed on export revenue. Much has been said about the tech sector bottoming out, but market observers say a meaningful recovery may only happen in 2H2025.

Meanwhile, the property market has been boosted by the introduction of the Johor-Singapore Special Economic Zone that serves as a catalyst to boost bilateral economic cooperation and unlock growth potential in both Malaysia and Singapore.

Overall, Phillip Capital observes that investors have largely gravitated towards large-cap stocks this year, driven by strong growth in several key sectors, particularly construction, property and utilities.

“A major factor driving this outperformance has been the expansion of data centre developments, which has significantly boosted contractors’ order books. The surge in infrastructure projects has not only invigorated the construction sector but has spurred an increase in land transactions, particularly in Johor, due to the growing presence of data centres,” it says in a Dec 24 note.

The research house also points out that the positive returns for the local equities have been largely driven by increased participation from government-linked investment companies, or GLICs. Notably, the Employees Provident Fund (EPF) has raised its stake in the Malaysian equity market to RM188 billion, representing 9% of total market capitalisation, higher than the historical five-year average of 7.8%.

“Historically, foreign flows have been the key determinants of KLCI performance. However, their impact has been less pronounced of late. While the foreign shareholding level remains low at 20.1% at end-November, the KLCI has appreciated by 9.7% YTD. This positive return has largely been driven by increased participation from government-linked investment companies,” Phillip Capital adds.

Notably, EPF’s new annual investment allocation has increased to above 70% for the domestic market, following Prime Minister Datuk Seri Anwar Ibrahim’s call for the pension fund to shift the domestic-foreign split of its investment portfolio to 70:30, from about 64:36 at the end of 2022.

Looking ahead, Phillip Capital remains upbeat on the local market on sustained FDIs, a stronger ringgit, robust domestic liquidity, positive economic trend, corporate earnings growth and the realisation of multinational corporations’ investment commitments. It has “overweight” calls on the banking, construction, electronic manufacturing services, gaming, healthcare, industrial (represented by data centre names), oil and gas, renewable energy, rubber glove, technology, telecommunications and transport sectors.

Penny stocks sell-off on margin calls

Though the broader market has been generally positive this year, more than a dozen small-cap stocks were caught in a bloodbath early this year due to the domino effect of margin calls.

Heavy selling pressure first hit three stocks linked to prominent investor Datuk Dr Yu Kuan Chon, namely Rapid Synergy Bhd (KL:RAPID), YNH Property Bhd (KL:YNHPROP) and Imaspro Corp Bhd (KL:IMASPRO). YTD, the share prices of these stocks have tumbled 73% to 97%.

Soon after, it ignited a widespread sell-off in several companies, including Sarawak Consolidated Industries Bhd (KL:SCIB), Mercury Securities Group Bhd (KL:MERSEC), Artroniq Bhd (KL:ARTRONIQ), Jentayu Sustainables Bhd (KL:JSB), Silver Ridge Holdings Bhd (KL:SRIDGE), Mestron Holdings Bhd (KL:MESTRON), Leform Bhd (KL:LEFORM) and Widad Group Bhd (KL:WIDAD). This prompted the regulator to issue unusual market activity queries to several counters.

Margin calls occur when those who pledge their shares are unable to keep their positions open by topping up the balance to the minimum margin in response to the sharp decline in share prices. Due to the selling wave, some stockbroking houses demanded upfront cash payments for a list of stocks that were on the downward spiral.

Save by subscribing to us for your print and/or digital copy.

P/S: The Edge is also available on Apple's App Store and Android's Google Play.

- Global funds hit pause on Indonesia after Prabowo policy changes

- Trump warns tariffs coming for electronics after reprieve

- Embattled billionaire Ong Beng Seng to step down from Hotel Properties

- Jentayu signs 40-year power purchase agreement for RM2.8b 162MW Sabah hydropower project

- Singapore eases monetary policy as expected, sees weaker growth in 2025

- China's March exports jump in temporary boost as Trump 2.0 heaps pressure

- Stocks rally in Asia as electronics get a tariff break

- Miti: 30 Malaysian firms set for 150 business matching sessions at Expo 2025 Osaka

- Frankly Speaking: After special review, what’s next for YNH?

- Share buybacks in vogue again amid market uncertainty