With the acquisition of UMW, Sime now commands over 50% of the domestic automotive market. (Photo by Zahid Izzani/The Edge)

This article first appeared in The Edge Malaysia Weekly on December 30, 2024 - January 12, 2025

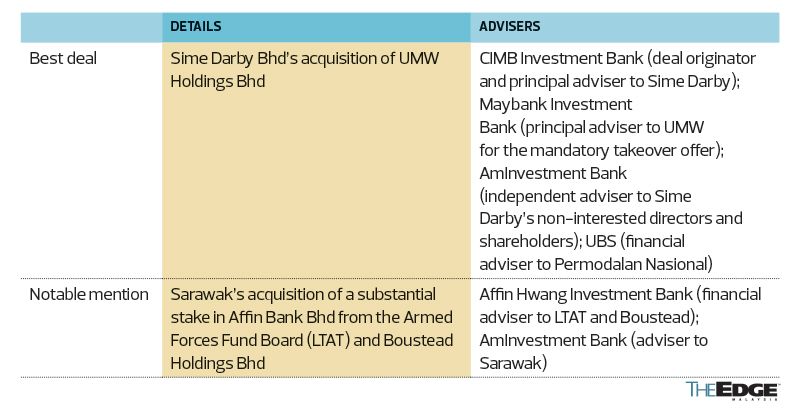

THERE are few mergers and acquisitions (M&A) that appear to make as much sense as the acquisition of UMW Holdings Bhd by Sime Darby Bhd (KL:SIME), which was completed early this year.

Looking at the automotive business of both Sime and UMW, they seemingly fit like a glove when merged as Sime is a regional distributor of luxury marques BMW, Mini, Porsche and Jaguar, while UMW is a local assembler and distributor of mass market brands such as Toyota and Perodua.

The acquisition immediately creates a large automotive group with a geographical presence in Malaysia as well as China and Australasia, and one that has a major presence in each market segment.

With the acquisition of UMW, Sime now commands more than 50% of Malaysia’s domestic automotive market through Perodua and Toyota. As at November 2024, Perodua’s market share stood at 48.6% of the total industry volume.

“This is a strategic move to further scale up and strengthen our presence in the Malaysian automotive sector, adding two highly performing brands into our Malaysian portfolio — Toyota and Perodua,” Sime group CEO Datuk Jeffri Salim Davidson had said. “As a partner of choice to some of the more admired brands in the automotive sector, we are very excited to have the opportunity to work with Toyota, one of the world’s largest and most respected automakers.”

The acquisition does not just make sense for Sime and UMW operationally. It also allows their common ultimate largest shareholder Permodalan Nasional Bhd (PNB) to unlock the value of its investment in UMW without losing control over the group’s large and diversified businesses.

The deal was announced in August 2023, for the acquisition by Sime of the entire 61.18% stake in UMW owned by both PNB and its funds. Sime also offered to acquire the remaining shares in UMW not owned by PNB or its funds at RM5 per share.

The acquisition of the equity interest of PNB and its funds in UMW was completed on Dec 13, 2023, while the mandatory general offer (MGO) and compulsory acquisition of all the remaining shares in UMW were completed on May 21, 2024.

The 61.18% stake was acquired for total cash consideration of about RM3.574 billion. CIMB was the deal originator and principal adviser to Sime for the M&A, while AmInvestment was the independent adviser to Sime for the acquisition.

In total, Sime spent RM5.8 billion to acquire UMW.

The acquisition goes beyond the automotive sector, as both Sime and UMW are distributors of industrial machinery.

Through Toyota Industries Corporation (Tico), Sime’s industrial segment portfolio is expanded, and it gives the group exposure to the materials handling business while complementing its existing mining and construction equipment business.

Sime is one of the largest distributors of Caterpillar’s industrial machinery in Asia-Pacific.

Besides Tico, the acquisition also brings Komatsu — a Japanese industrial machinery brand — into Sime’s fold, as UMW is the distributor for the brand in Malaysia, Singapore, Brunei, Papua New Guinea, China, Myanmar and Vietnam.

Notable mention

The Sarawak government’s acquisition of a roughly 26% stake in Affin Bank Bhd (KL:AFFIN) from the Armed Forces Fund Board (LTAT) and Boustead Holdings Bhd gets a notable mention in the M&A category, as it was good for all the parties involved.

It enabled Sarawak to raise its equity interest in the country’s second-smallest banking group by assets to 31.25%, from 4.81% previously, thus becoming its largest shareholder. Sarawak had long wanted to have a retail bank to support its strong developmental needs.

The deal helped unlock value for LTAT and its debt-laden unit, Boustead, as it puts much-needed cash into their hands. Conglomerate Boustead had, for some time, been looking to rationalise some of its non-core assets to help with its cash-flow needs.

While Boustead has ceased being a shareholder in Affin, LTAT still holds a 22.01% stake, allowing it to continue to benefit from the bank’s growth. As for Affin, having Sarawak as its biggest shareholder opens doors to business opportunities in the fast-developing state, thereby improving its growth prospects.

Even Affin’s minority shareholders have benefited, as the bank’s share price — after years of underperforming those of its peers — moved up strongly over the course of this year, peaking at RM3.43 on Aug 21, on the expectation that Sarawak would increase its stake. As at its Dec 13 close of RM2.91, the stock had gained 43.1% year to date, giving the bank a market value of RM6.99 billion.

Under the deal, Sarawak — via a wholly-owned subsidiary, SG Assetfin Holdings Sdn Bhd — acquired 634.72 million of the bank’s shares (a stake of about 26%) from LTAT and Boustead in a direct business transaction on Nov 25.

While they did not disclose the price at which the shares were acquired, Bloomberg data shows that it was done at between RM2.46 and RM2.84 a share. This represented a discount of between 16.9% and 4.1% over Affin’s closing price of RM2.96 on the open market that day. It is understood that LTAT and Boustead, which also sold 12.43 million shares on the open market, fetched RM1.78 billion in total from the divestment.

Consequently, LTAT saw its stake in Affin reduced to 22.01%, compared with 28.88% just prior to the deal, while Boustead, which used to hold a 20.08% stake, is no longer a shareholder.

Save by subscribing to us for your print and/or digital copy.

P/S: The Edge is also available on Apple's App Store and Android's Google Play.

- Ghost of MBI reawakens, police raids rattle Penang

- China said to advise Shein against shifting supply chain

- Trump's reciprocal tariffs: Five things Malaysia must do now

- The world suddenly has a plausible alternative to US Treasuries

- Hydroshoppe, Menara KL lose bid to temporarily halt KL Tower's takeover by LSH Capital's unit

- Harley CEO Zeitz plans to retire this year amid turnaround

- Police deny claims of concealing fatalities in Putra Heights disaster

- Wall Street rebounds sharply on hopes of tariff talks

- AEON Credit, Matrix Concepts, Fajarbaru, S P Setia, Yong Tai, Taghill, LSH, KNM, Northern Solar, PetGas, Panasonic Malaysia, Subur Tiasa

- Massive US tariffs likely to neutralise ringgit's weakness as export aid, say economists