This article first appeared in The Edge Malaysia Weekly on December 23, 2024 - December 29, 2024

APEX Healthcare Bhd (KL:AHEALTH) is doubling down on its pharmaceutical business in a bid to replace the earnings it used to receive from its associate Straits Orthopaedics (Mfg) Sdn Bhd, which it holds through Straits Apex Group Sdn Bhd.

Straits Orthopaedics contributed about 9% to 11% to Apex Healthcare’s profit before tax prior to the divestment.

Straits Orthopaedics is a contract manufacturer for orthopaedic medical devices, and Apex divested its interest to Singapore-based private equity firm Quadria Capital Investment Management Pte Ltd in May 2023. Following the divestment, Apex’s effective interest in Straits was reduced to 16% from 40%.

The group is not intimidated by the task to fill the earnings gap, but has been working on driving Apex’s next phase of growth through rigorous research and development (R&D) of its pharmaceutical products.

“I think 2025 is quite exciting for us because we’re going to start to see the impact of our increased investment in R&D in our product pipeline,” says Apex chairman and CEO Dr Kee Kirk Chin in an interview with The Edge.

In the financial year ended Dec 31, 2023 (FY2023), Apex invested RM8.5 million in R&D, representing 3.2% of its total manufacturing revenue, which saw an 18.9% increase compared with FY2022. The group has committed to reinvest 5% of its total manufacturing revenue into R&D each year for product innovation going forward.

“Everything links back to our product pipeline and R&D, which is really the core — the heart — of the business,” says Kee.

The CEO notes that the group will file its first generic pharmaceutical product for regulatory approval in the European Union (EU) this year. The original drug’s patent will expire in 2026.

It is a big step for the group, given that the product has been developed to EU standards — deemed global standards — and that it will open up new markets for Apex.

“Since it meets global standards, it can be sold into the EU and with a little bit more adjustment, it can be sold in the US, but we have not focused on [the US] yet. We are developing our dossiers, certain products according to EU standards and we are going to file the first product in the fourth quarter this year,” Kee adds.

He attributes the group’s ability to do so to its collaborations with contract research organisations (CROs) as it speeds up the development process. He says its previous way of just relying on manufacturing and selling products from its in-house R&D is “too slow” and limited to the talent pool available locally.

“We can’t be restricted by [relying on in-house R&D only] now because the world is so connected today. So in the last three years, we have been doing a lot of R&D collaborations.

“We’re using contract research organisations. We also formed joint ventures like Zynexis Healthcare Pte Ltd so that we can have more channels to bring new products into our portfolio,” he explains.

Zynexis is a 40% associate company of Apex, and a result of a joint venture with Fortune 500 company Shanghai Pharmaceuticals Holding Co Ltd.

Kee says Apex has “well over 10 contracts” with CROs in place where some of the products are being developed to EU standards.

Apex is strategic on the type of pharmaceutical products that it is developing for commercialisation, looking into therapeutic segments in respiratory, dermatology, cardiovascular and alimentary tract and metabolism, and also in areas with substantial disease burdens.

“So we have got molecules in all the different classes under development in our product pipeline. We hope to be able to reach the market when the patent expires. These formulas that we develop will meet EU standards.

“The key is to have a very strong portfolio of products that you can be first to market after the patent expires, or have a better version of the generic that’s already available, or have a generic that has got very few other generics in the market. Those are the three areas we are going into,” he says.

Apart from utilising CROs, Apex is also growing the business through Zynexis, where it is tapping the relationship with its Chinese pharmaceutical company partner to identify strong products to licence to Zynexis that it can bring to some Asian markets.

“We have filed nine core products in Malaysia and Singapore for regulatory approvals as at end-September in new therapeutic areas with high disease burdens. These are products that are new to the group that we [do not] have in our portfolio currently. We hope to get approvals in early or mid-2026 so that we can launch our first product then,” says Kee.

As well as pushing growth in the pharmaceutical product segment, Kee says Apex also plans to put more emphasis on building its consumer healthcare portfolio. Currently, that business segment contributes to less than 10% of its revenue.

“We have always been strong in prescription medicines but we don’t have strong consumer brands. We believe that our strength with the doctors can help us create endorsement for our consumer brands and that can translate into sales directly to consumers,” he says.

Xepa is Apex’s well-known prescription medicine proprietary brand. Apex also has proprietary brands in the consumer healthcare space, including KAPS, Agnesia and Remeco, among others.

This year, it has launched nine consumer products. While it develops the formulas, it uses contract manufacturers to manufacture its products as the cost of using their EU-certified pharmaceutical plant would be too high.

“We find it is better to use a contract manufacturer. We also can have different dosage forms this way and for some products like probiotics, where we don’t have the facility to grow [microorganisms] with bioreactors and all that, we can get them from reputable contract manufacturers,” explains Kee.

He admits that the consumer product space is a competitive one, but sees growing the consumer product portfolio as a way to balance out its portfolio.

“Consumer products are not going to be the main thing for us. It is something where we see ourselves under-represented. We want to balance our portfolio so as to make it more resilient and not entirely dependent on prescription medicine,” shares Kee, adding that he will be happy if Apex is able to grow this segment to about 20% to 25% of its group revenue.

Apex’s net profit for the cumulative nine months ended Sept 30, 2024 (9MFY2024) stood at RM63.1 million, substantially lower than RM377.9 million a year earlier. This was mainly due to the absence of non-recurring gains amounting to RM304.4 million as a result of the Straits divestment.

Apex also saw a share of loss from Straits for 9MFY2024 amounting to RM3.2 million, compared with a gain of RM319.1 million a year earlier, due to foreign exchange losses from the strengthening of the ringgit, which was further exacerbated by financing costs and amortisation of intangible assets.

Revenue increased 4% to RM724.3 million for 9MFY2024 compared with RM696.2 million a year ago.

Notably, Apex derives two-thirds of its revenue from Malaysia, while the remaining amount comes from Singapore and other international markets. The group also predominantly derives revenue from the private sector market for its group brand products, and about 10% of revenue comes from the government sector.

Apex to eventually exit Straits

Kee shares that before deciding to divest its interest in Straits, Apex had considered “very seriously” to buy the company off its partner when the offer was made. However, the company eventually decided against it, given that orthopaedic medical devices are not its strong suit and it does not have enough know-how to manage this business.

“Straits’ business is really quite different from our pharmaceutical business. We don’t have the people to run it and we rely a lot on our partner. Our partner [TH Su] is 75 years old and he was looking to take something off the table, so he offered the company to us, provided we could match offers from the market.

“We considered it very seriously, but the price was quite high. In the end, we decided not put so much resources into something that’s non-pharmaceutical and that’s why we agreed with him to find a buyer so that we can both exit together,” says Kee.

While the plan was for both Apex and Su to exit Straits entirely, Quadria Capital had required Su to continue to run the business for another five years.

As such, Apex and Su came to an agreement with Quadria Capital to reinvest a substantial portion of their sales proceeds back into the company as minority-stake partners.

“My partner is very keen to continue working with them. Quadria has good connections and networks in the medical device space. Plus, it has the funding and will put in place more procedures for managing the company and driving growth.

“So we expect to continue growing the business over the next few years and exiting together with the remaining stake,” he says.

When asked of his thoughts on acquiring companies following this divestment, Kee says they look at different companies all the time but have not found anything on the horizon for now.

“It must be something that we already have quite significant expertise in managing. Then we can add value to grow,” he says.

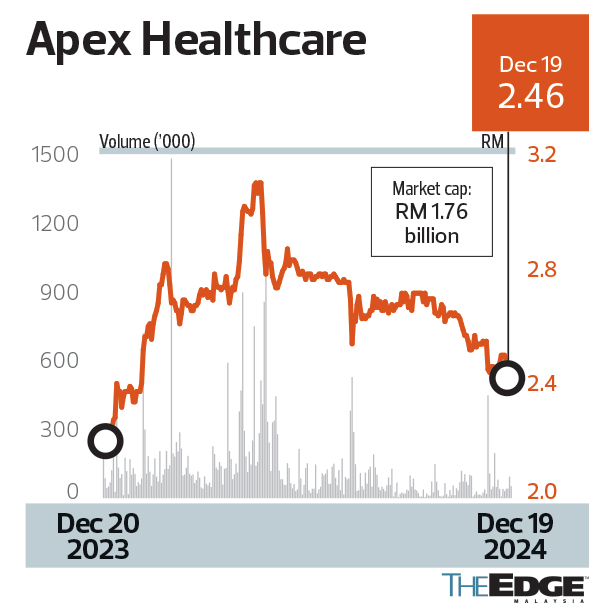

Year to date, Apex has gained 4.54% to close at RM2.46 last Thursday. This puts its market capitalisation at RM1.76 billion.

At a forward price-earnings ratio of 19.92 times, it is slightly higher than peers such as Pharmaniaga Bhd’s (KL:PHARMA) 11.41 times and Duopharma Biotech Bhd’s (KL:DPHARMA) 18.66 times.

There is only one “buy” call on Apex, with two “hold” and one “sell”. The average target price is RM2.77, implying an upside potential of 12.6%.

Save by subscribing to us for your print and/or digital copy.

P/S: The Edge is also available on Apple's App Store and Android's Google Play.

- Global funds hit pause on Indonesia after Prabowo policy changes

- Embattled billionaire Ong Beng Seng to step down from Hotel Properties

- Trump warns tariffs coming for electronics after reprieve

- Jentayu signs 40-year power purchase agreement for RM2.8b 162MW Sabah hydropower project

- Singapore eases monetary policy as expected, sees weaker growth in 2025

- Sony lifts PS5 price in Europe by 25% ahead of a likely US hike

- Anwar to meet Myanmar junta head in Bangkok

- UK rushes to find materials to keep British Steel plant running

- Majujaya files petition to wind up Bina Puri for failure to pay RM30m awarded by court

- Bursa to keep IPO target of 60 listings this year despite tariff turmoil