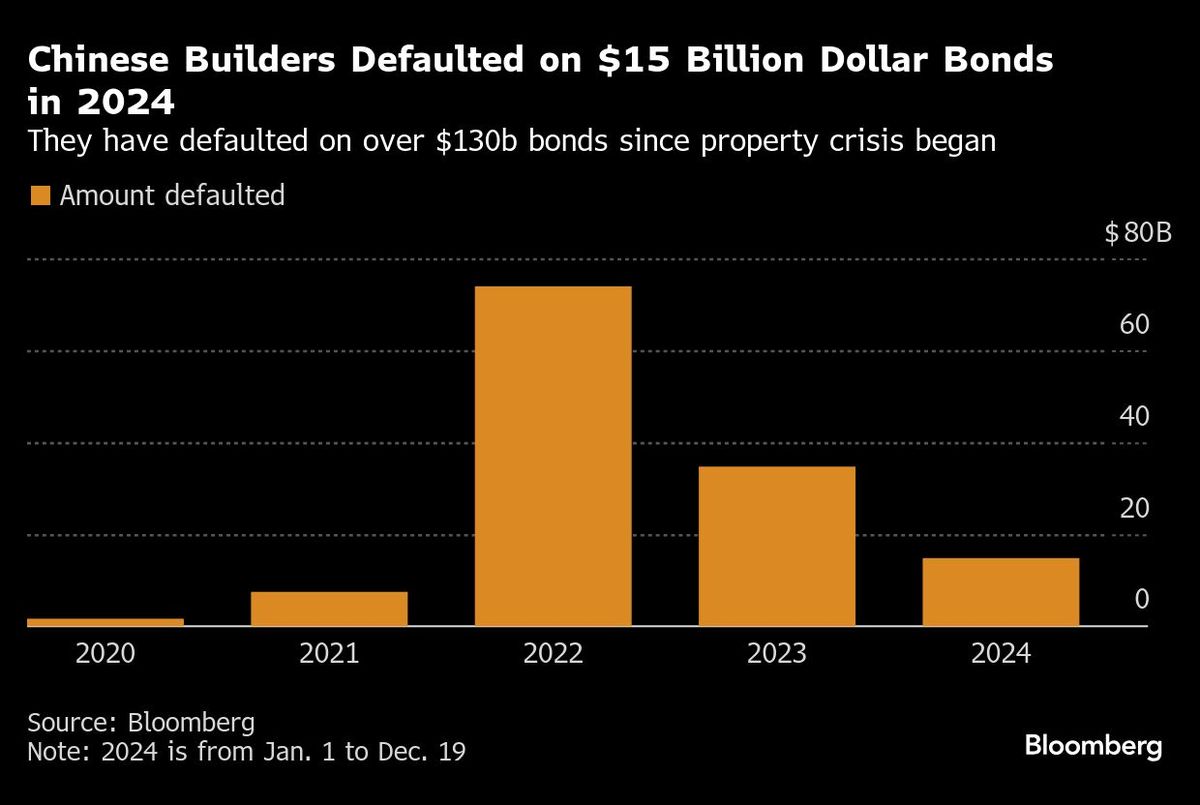

As China’s property debt crisis enters its fifth year, there’s little indication that distressed developers are finding it easier to repay debt, as a slump in home sales continues. Their dollar bonds are still trading at deeply distressed levels, their debt issuance has nearly dried up, and the sector is a notable laggard in stock markets.

Alarm bells went off again in recent weeks, when the banking regulator told top insurers to report their financial exposure to China Vanke Co, Ltd to assess how much support the country’s fourth-largest developer by sales needs to avoid default. Over in Hong Kong, New World Development Co Ltd sought to delay some loan maturities, while Parkview Group put up a landmark commercial complex for sale in Beijing.

The latest signs of stress are adding to concerns that the worst is far from over for the housing sector in the world’s No. 2 economy, once a powerful growth engine and now a big drag on demand for items from furniture to cars. And they are particularly worrying because Vanke’s woes show the liquidity crisis is hurting one of the few big builders that have avoided default so far. The trouble faced by its Hong Kong peers, meanwhile, means the contagion is increasingly felt offshore.

“While recent government policies have helped arrest the speed of decline, it could take another one or two years for the sector to bottom,” said Leonard Law, senior credit analyst at Lucror Analytics. “Against this backdrop, we can’t rule out the possibility of some more defaults next year, albeit the overall default rate should be much lower than before.”

Chinese authorities have stepped up efforts in recent years to ease the country’s unprecedented housing slowdown, including interest rate cuts, slashing purchasing costs and restrictions, as well as state guarantees for bond sales by stronger developers. Top leaders also pledged to stabilise the property market next year at a key economic meeting earlier this month.

However, the rescue measures adopted so far have focused on preventing a collapse in property prices, protecting owners of unfinished apartments, and using state funds to help absorb excess supply. At the same time, policymakers chose to look on as former industry behemoths China Evergrande Group and Country Garden Holdings Co Ltd became defaulters.

This is why the banking regulator’s queries over insurance firms’ exposure to Vanke’s bonds and private debt have drawn much attention. The insurers conducted similar checks in March, as fears grew over the builder’s repayment risks. Separately, Vanke executives have visited several insurers in the past few weeks, urging them not to exercise put options on some private debt that will soon become open to them.

“If there is no turnaround in property sales, asset disposals remain slow in a weak property market, and financial institutions become more cautious and require additional collateral, we believe Vanke could see a liquidity shortage sooner than expected,” Jefferies Financial Group Inc analysts including Shujin Chen wrote in a note. “We still put the likelihood of a government bailout at below 50%.”

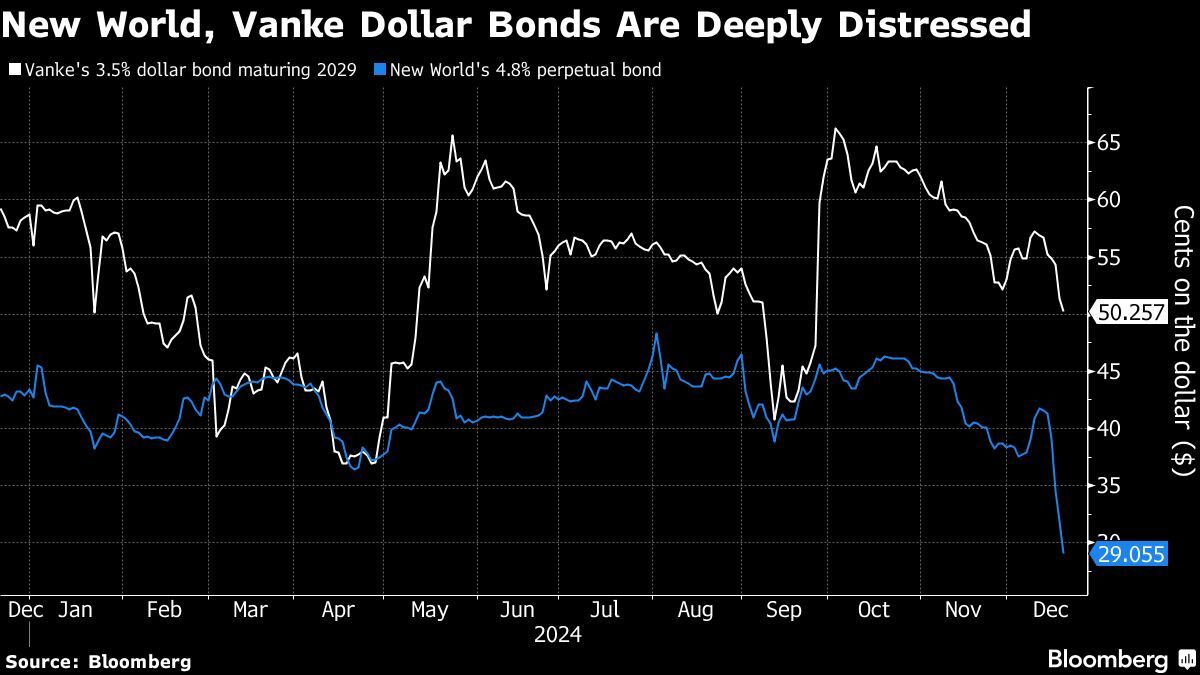

Vanke’s dollar bond due May 2025 dropped about 10 cents in the past week to around 80 cents on the dollar, the biggest weekly decline in more than a year. Its 2027 note also slumped to 49 cents, signalling investor doubts about full redemption.

Vanke’s woes come at a time when capital markets continue to show weak investor confidence in the sector: Mainland Chinese and Hong Kong developers have issued US$67.3 billion (RM303.41 billion) of bonds this year, putting the market on track for its smallest annual issuance in at least in a decade, Bloomberg-compiled data show. Meanwhile, a Bloomberg stock gauge of Chinese builders has risen 3.7% this year, versus 24% for a broader index tracking the country’s firms listed in Hong Kong.

In another worrying development, distressed Hong Kong builder New World Development is asking banks to postpone the due dates of some bilateral loans, a move that deepens concerns over its ability to service one of the heaviest debt loads of its kind. Controlled by the family empire of tycoon Henry Cheng, the developer had total liabilities of HK$220 billion (US$28.3 billion) at the end of June and recorded its first annual loss in two decades.

New World Development’s debt struggle is an ominous sign that China’s property woes are spreading overseas. According to its 2024 annual report, the builder derived 73% of its property development and investment revenue from mainland China.

Some perpetual notes from the developer of projects, including the K11 Art Mall in Hong Kong’s shopping district of Tsim Sha Tsui, have recently fallen to a record low of around 30 cents. Its shares are down 57% this year.

Meanwhile, Parkview Group, a Hong Kong-based high-end developer whose founding family hails from Taiwan, is seeking buyers for an iconic commercial complex in Beijing’s central business district, as it grapples with high loan servicing costs and low occupancy rates. A Chinese state-owned firm is said to be interested in purchasing the asset, which is known for its unique pyramid-shaped structure and includes a shopping mall, hotel, office towers, and an arts hub.

“Hong Kong developers are facing a double-whammy in the current down cycle,” said Daniel Fan, credit analyst at Bloomberg Intelligence. “China’s property market, where many of them are involved, shows no sign of a strong recovery, while Hong Kong’s market correction is still ongoing.”

Uploaded by Liza Shireen Koshy