Kuala Lumpur experienced steady growth in the residential market with 5,589 new units completed during the quarter, marking a 10.5% rise year on year (Photo by Sam Fong/The Edge)

This article first appeared in City & Country, The Edge Malaysia Weekly on December 23, 2024 - December 29, 2024

The residential property market in Kuala Lumpur and Selangor displayed contrasting trends in terms of supply and transactions in the third quarter, says Savills Malaysia director of research and consultancy Fong Kean Hwa in presenting The Edge Malaysia | Savills Klang Valley Residential Property Monitor 3Q2024.

He says the residential market in KL is experiencing steady growth, with 5,589 new units completed in 3Q2024, marking a 10.5% rise year on year (y-o-y) from 5,057 units. Incoming supply surged by 23.9% y-o-y, reaching 55,667 units during the quarter, compared with 43,047 units in the same period last year.

“The completion of new residential properties is on the rise, signalling strong momentum for the housing market in 2024,” says Fong.

In contrast, he notes that Selangor saw a decline in new residential completions, with 11,537 units finalised in 3Q2024, marking a 26.1% drop y-o-y from the 15,605 units recorded in 3Q2023. Incoming supply decreased 7.3% to 82,373 units in 3Q2024 from 88,834 units in the same period last year.

In terms of residential transactions, KL experienced a decline, with 4,498 units changing hands, compared with 4,830 units in 3Q2023.

“However, the total transaction value contrasts with this drop, increasing from RM4,376 million to RM4,458 million y-o-y. Additionally, the overhang scenario has improved from 8,696 units in 3Q2023 to 8,235 units during the quarter under review, signalling an improvement in the residential sector in KL,” Fong says.

In contrast to KL, Selangor’s residential market saw an increase in transactional activity, with the number of transactions climbing slightly from 14,296 units in 3Q2023 to 14,757 units in 3Q2024. The total transaction values also increased from RM8,486 million to RM8,829 million, he notes.

“This growth underlines increased buyer confidence, fostering an optimistic market sentiment. Furthermore, the overhang units in Selangor saw improvement, dropping from 6,187 units in 3Q2023 to 5,061 units in 3Q2024. This highlights improved market sentiment in the property market. In summary, the residential sector is progressing upwards with reducing unsold inventory, primarily driven by heightened buyer confidence,” he says.

During the quarter, the economy expanded by 5.3% in 3Q2024 (versus 5.9% in 2Q2024), driven by strong investment activity and continued improvement in export activity, says Fong.

“Residential loan applications grew 6.2% y-o-y to RM122.45 billion in 3Q2024, but approval rates fell slightly from 43.2% to 42.6%, reflecting banks’ cautious stance despite strong demand. Bank Negara Malaysia kept the overnight policy rate steady at 3% to support economic growth.”

He adds that the property market is poised for transformation with key policy-driven trends, such as the expansion of the De Rantau digital nomad pass to include a broader range of professionals. “This is expected to drive demand for high-end residential properties in key urban centres, especially in Greater KL as global talents seek modern, flexible housing options.”

The other key trend is the National Policy on Climate Change 2.0. “This emphasises sustainable urban planning, incorporating low-carbon developments, sponge city concepts and transit-oriented developments (TODs). Developers are anticipated to respond by integrating green features, energy-efficient technologies and climate-resilient designs, particularly in TOD-focused projects.

“Together, these initiatives are set to lift interest in both the ownership and rental markets, solidifying the country’s position as a hub for expatriates and sustainable urban living,” he says.

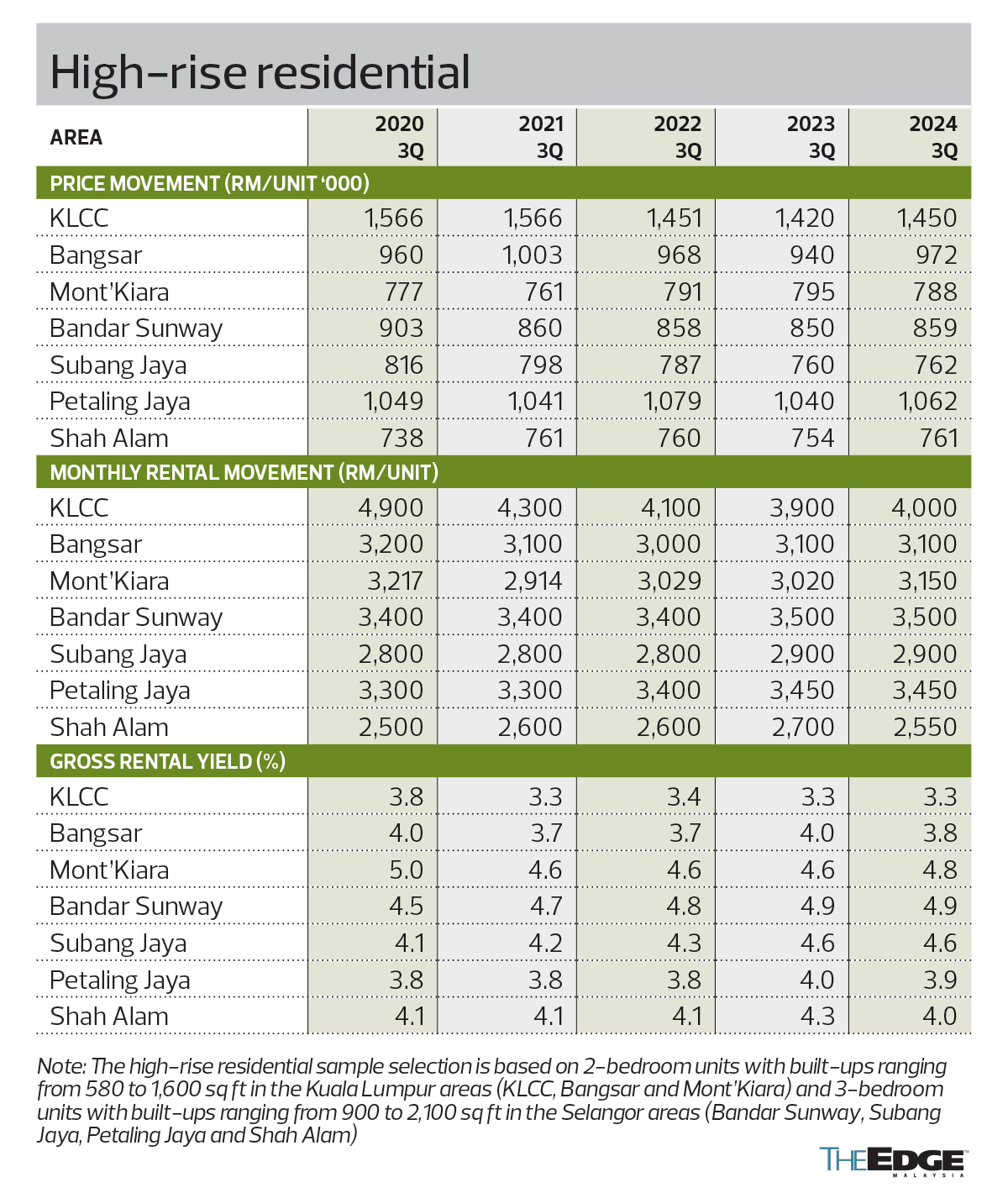

High-rise residential

The sampled two-bedroom units in KL’s submarkets of KLCC and Bangsar saw their average transacted price increase y-o-y by 2.1% and 3.4% respectively to RM1.45 million and RM972,000 during the review quarter, while Mont’Kiara’s declined by 0.9% to RM788,000. Average rents in KLCC and Mont’Kiara rose 2.6% and 4.3% to RM4,000 and RM3,150 monthly, while Bangsar’s remained unchanged at RM3,100 per month.

“There is a continued demand for properties in prime areas. The KLCC and Bangsar markets have seen positive price growth and a more optimistic rental outlook than a year ago. On the other hand, Mont’Kiara experienced a slight decline in transaction prices. Despite the slight retraction, Mont’Kiara continues to offer better rental yields than KLCC and Bangsar,” says Fong.

Several high-rise projects were launched in KL in 3Q2024. One of which is Skyline Embassy (formerly Agile Embassy Garden) in Jalan Ampang by TSLAW Land Sdn Bhd. The project comprises a total of 1,296 serviced apartments in three towers at selling prices ranging from RM650,000 to RM1.25 million. The project is expected to be completed by 2028.

Radium Development Bhd (KL:RADIUM) has launched Radium Arena, a two 40-storey tower residential project in the Old Klang Road area with a total of 988 condominium units at prices from RM436,000 to RM800,000. The project is slated to complete in 2028.

Mah Sing Group Bhd (KL:MAHSING) has launched M Aspira in Taman Desa during the quarter. The project comprises two towers with 1,613 units in total. Selling prices start from RM448,000.

Also in the third quarter, Mitsui Fudosan (Asia) Malaysia Sdn Bhd — a subsidiary of Mitsui Fudosan Co Ltd — opened Mitsui Serviced Suites Bukit Bintang City Centre (BBCC) for rent. The project has a total of 269 units that are available for a one-year lease with a rental rate, inclusive of utility fee, starting from RM3,500 per month. It also offers rentals on a monthly basis with a minimum of 30 days stay from RM7,200.

In Selangor, high-rise residential prices and rentals continued to grow across most selected submarkets, indicative of a steady demand, Fong observes.

“Areas such as Bandar Sunway, Petaling Jaya and Shah Alam continue to experience moderate price growth, with rental rates stable or slightly increasing, resulting in relatively stable rental yields.”

The sampled three-bedroom units in Bandar Sunway, Subang Jaya and Petaling Jaya saw their average transacted price increase by 1.1%, 0.3% and 2.1% y-o-y respectively to RM859,000, RM762,000 and RM1.062 million, while their average monthly rents have remained unchanged at RM3,500, RM2,900 and RM3,450.

Shah Alam, meanwhile, recorded an average transaction price increase of 0.9% to RM761,000 while the average monthly rental rate decreased by 5.6% to RM2,550 during the quarter, compared with RM2,700 recorded in 3Q2023.

New launches in Selangor during the review quarter include Astrum Shah Alam Phase 1 by Setia Awan Holdings Sdn Bhd. The project comprises 858 condominium units with built-ups from 570 to 1,065 sq ft. Units are priced from RM270,000 to RM793,000.

Mori Park Phase 1 by OSK Property Holdings Bhd was also launched during the quarter. The project, located in Section 13, Shah Alam, features 812 units of serviced apartments with sizes from 550 to 958 sq ft. Units are priced from RM275,000 to RM680,000.

The Lines @ Mutiara Damansara by Boustead Properties Bhd was launched during the review period. The project, located on a parcel formerly known as eCurve in Petaling Jaya, will comprise a total of 999 units that range from 590 to 2,880 sq ft in size. Selling prices are from RM649,000 to RM3.74 million.

Paramount Property Development Sdn Bhd has also launched the second phase of The Atera in Petaling Jaya, which offers 876 serviced apartment units with sizes ranging from 779 to 1,420 sq ft. Units are priced from RM250,000 to RM1.37 million.

All four projects are expected to be completed by 2028.

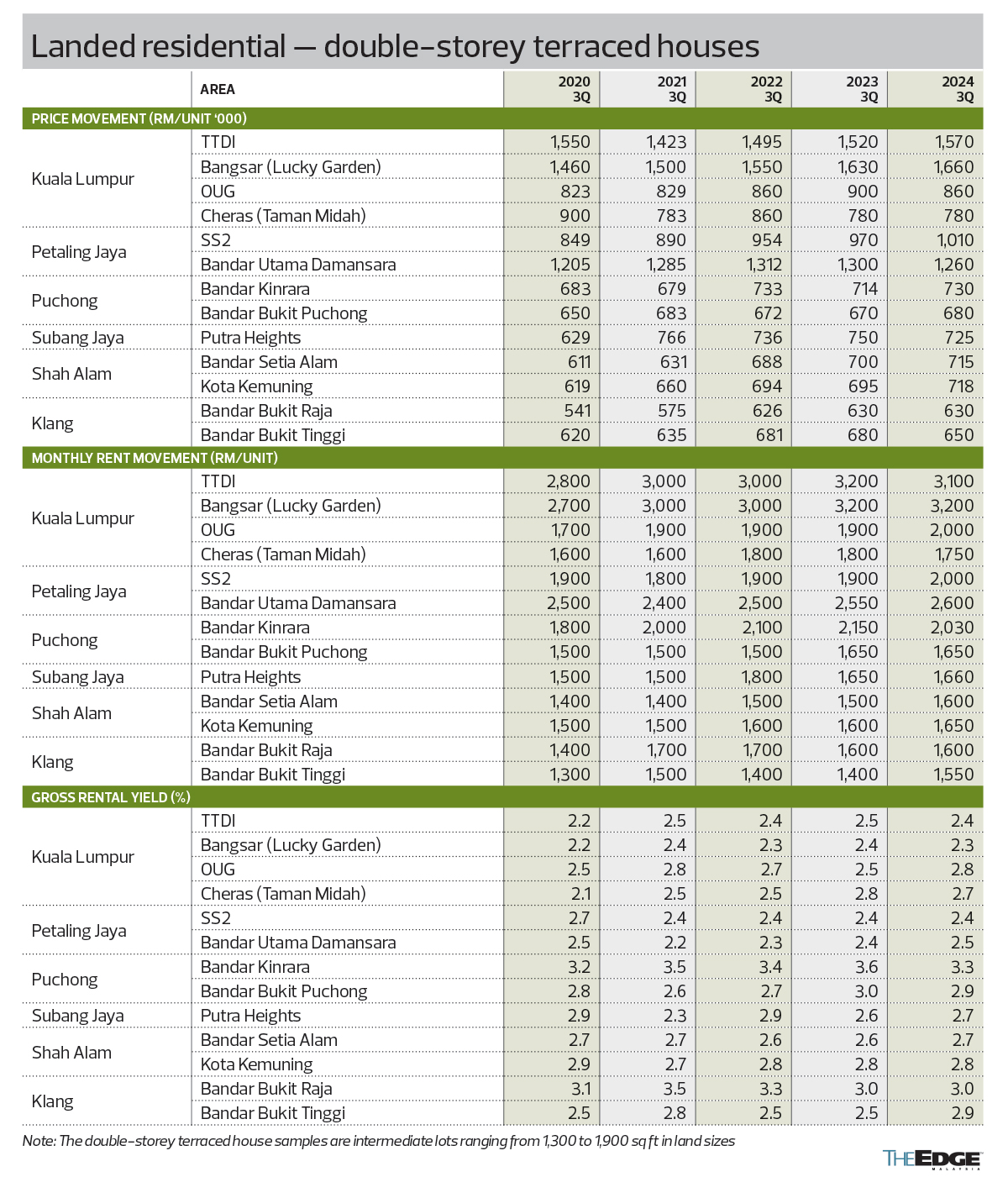

Double-storey terraced houses

The 2-storey terraced house markets in KL and Selangor displayed mixed trends, Fong notes.

“Some areas like Taman Tun Dr Ismail (TTDI) and Bangsar saw price increases while others, such as OUG and Bandar Bukit Tinggi, experienced price declines. However, rental yields remain stable or improving in many locations, especially in well-established neighbourhoods with good amenities such as SS2 in Petaling Jaya (PJ) and Kota Kemuning in Shah Alam.”

In TTDI, the average transacted price grew 3.3% y-o-y to RM1.57 million while average rent declined 3.1% to RM3,100 monthly.

In Bangsar’s Lucky Garden, the average price increased by 1.8% y-o-y to RM1.66 million while average rent held steady at RM3,200 per month.

OUG saw a y-o-y decline in average price by 4.4% to RM860,000 while the average rent increased 5.3% to RM2,000 per month.

In Taman Midah, Cheras, the average price remained stable y-o-y at RM780,000 while average monthly rent decreased by 2.8% to RM1,750.

In Selangor, the 2-storey terraced houses sampled in SS2, Petaling Jaya, saw a 4.1% increase y-o-y in average price to RM1.01 million while the average monthly rent increased by 5.3% to RM2,000.

“Although an old neighbourhood, the 2-storey terraced houses in SS2 remained in high demand, attributed to its amenity-rich location and excellent accessibility,” says Fong.

In Bandar Utama, PJ, the average price declined 3.1% y-o-y to RM1.26 million while rents rose 2% to RM2,600 per month.

In Puchong, average prices in Bandar Kinrara and Bandar Bukit Puchong increased by 2.2% and 1.5% y-o-y respectively. The average monthly rent in Bandar Kinrara declined 5.6% to RM2,030 while Bandar Bukit Puchong’s remained unchanged at RM1,650.

The 2-storey houses in Putra Heights saw an average price decline y-o-y of 3.3% during the quarter, bringing the average price to RM725,000. Despite this, its average rent rose slightly by 0.6% to RM1,660 monthly.

The sampled 2-storey terraced property in Shah Alam saw growth in prices and rents during the quarter. The average price in Bandar Setia Alam increased by 2.1% to RM715,000 while average monthly rent rose 6.7% to RM1,600 monthly.

“Strong demand for housing in Setia Alam is supported by its well-established amenities, including Setia City Mall with a convention centre, a government hospital, schools, offices and others,” says Fong.

Similarly in Kota Kemuning, the average price rose 3.3% to RM718,000 while average rent increased by 3.1% to RM1,650 monthly.

“As a mature township with limited land for new developments, this price growth underscores the resilience of well-established areas with excellent amenities and connectivity, suggesting that demand will remain steady in this locality,” he says.

In Klang, the average price and monthly rent of 2-storey homes in Bandar Bukit Raja remained unchanged at RM630,000 and RM1,600 respectively, while in Bandar Bukit Tinggi the average price declined 4.4% to RM650,000 but average rent grew 10.7% to RM1,550 per month.

During the quarter, S P Setia Bhd (KL:SPSETIA) launched Ferrous 3, the third phase of its Ferrous 2-storey landed homes series in Setia Alam Impian, Shah Alam. The phase features 101 freehold homes with built-ups ranging from 1,950 to 2,204 sq ft at selling prices ranging from RM915,000 to RM1.42 million. The project is expected to be completed by August 2026.

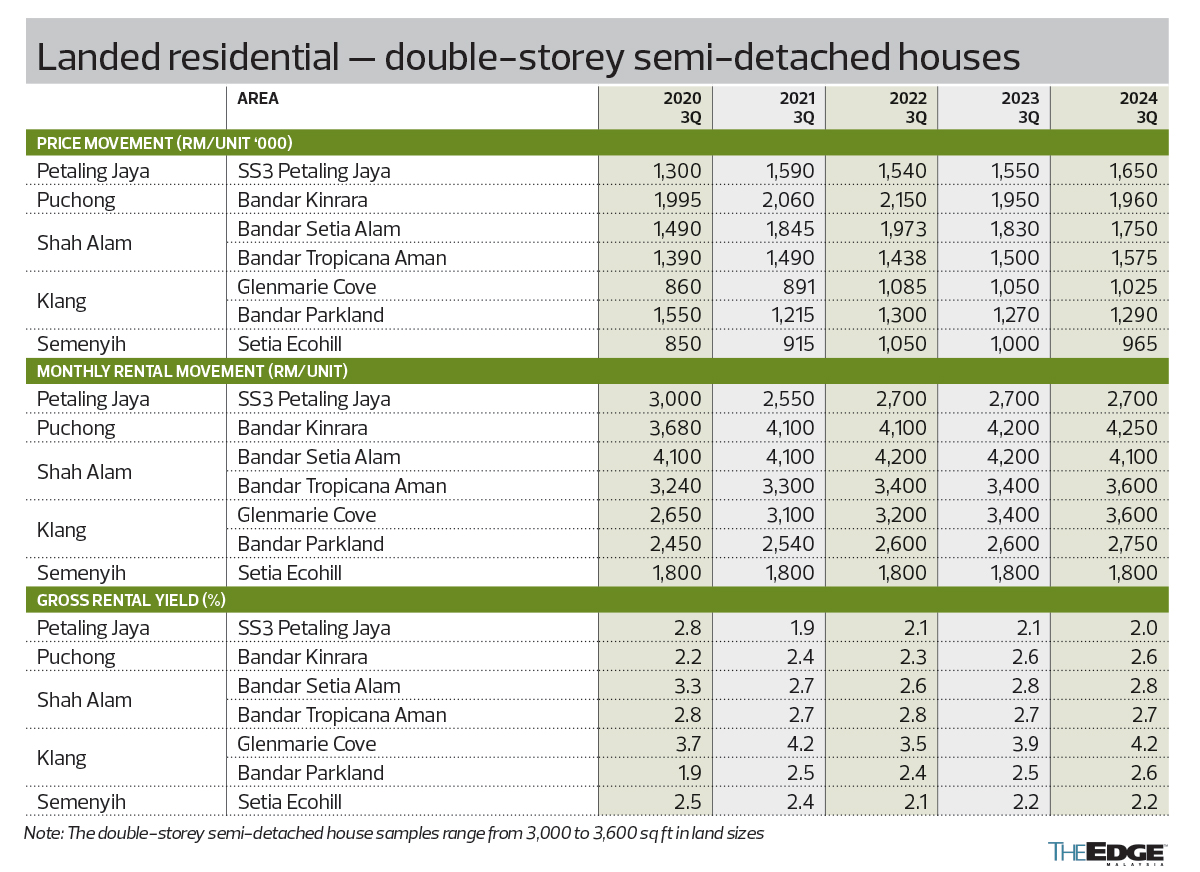

Double-storey semidees

The market for 2-storey semidees in Selangor also showed mixed trends, Fong observes.

“Areas like SS3 in PJ and Bandar Tropicana Aman in Shah Alam, saw strong price growth while Bandar Kinrara and Setia Alam experienced minimal increases or declines. Klang offers good rental yields, while Semenyih shows potential due to upcoming developments.”

SS3 in Petaling Jaya’s average price surged by 6.5% y-o-y to RM1.65 million while the average rent remained unchanged at RM2,700 monthly.

In Bandar Kinrara, Puchong, the average price and rent increased 0.5% and 1.2% y-o-y respectively to RM1.96 million and RM4,250 monthly.

In Shah Alam, the average price and monthly rent in Bandar Setia Alam declined y-o-y by 4.4% and 2.4% respectively to RM1.75 million and RM4,100, whereas those in Bandar Tropicana Aman increased by 5% and 5.9% respectively to RM1.575 million and RM3,600 monthly.

In Klang, Glenmarie Cove saw the average price fall y-o-y by 2.4% to RM1.025 million while monthly rent grew 5.9% to RM3,600. Bandar Parkland’s average price and monthly rent increased by 1.6% and 5.8% respectively to RM1.29 million and RM2,750 monthly.

Setia Ecohill in Semenyih saw a 3.5% decline y-o-y in average price to RM965,000 while the average monthly rent remained stable at RM1,800.

Semenyih has seen several major transactions during the quarter, Fong notes.

“In August, Mah Sing completed its acquisition of a 500-acre freehold parcel from Petaling Garden Sdn Bhd (a subsidiary of S P Setia) for RM392.04 million. With an estimated gross development value of RM3.3 billion, the land will be developed into a township development named Glengowrie Estate and will be Mah Sing’s largest township in the Klang Valley, which will primarily comprise 2-storey landed homes.

“Eco World Development Group Bhd (KL:ECOWLD), through its 81% owned subsidiary Mutiara Balau Sdn Bhd, is purchasing 10 parcels totalling 847.25 acres in Semenyih for RM742.41 million in cash. The land will be used for a new mixed-use development, Eco Forest 2, with an estimated GDV of RM4.6 billion. EcoWorld Malaysia expects the acquisition to be completed by 1H2025.

“While the overall performance of the areas monitored has been mixed, they mostly indicate a positive and stable trend across both landed and high-rise properties,” he says.

Save by subscribing to us for your print and/or digital copy.

P/S: The Edge is also available on Apple's App Store and Android's Google Play.

- Mr DIY founder Tan Yu Yeh relinquishes vice chairman post, to serve as adviser

- China hits back at Trump with tariffs, limits on key exports

- Malaysia refutes 47% US import tariff claim, takes measures to prioritise well-being of businesses and people

- 50,000 Malaysian jobs at risk, business chamber warns as it calls for urgent US tariff mitigation council

- Trump hits China tariff retaliation, says policy will remain

- ‘Worst-case scenario’ for tech wipes $1.4 trillion from Nasdaq

- Anwar says impact of latest US tariff on nation's economy still being assessed

- Tok Mat, Rubio discuss bilateral relations, Asean-US Special Summit date

- US solar’s hoarding habit will help blunt sting from Trump tariffs

- Wall Street rout drags Nasdaq near bear market