This article first appeared in The Edge Malaysia Weekly on December 16, 2024 - December 22, 2024

IN the same week that Putrajaya said some four million Employees Provident Fund (EPF) members under the age of 55 have withdrawn RM11.6 billion from the newly created Flexible Account 3 in the past seven months, the EPF renewed its attempt to nudge more members to save for retirement earlier by introducing a three-tier savings recommendation that is significantly above its existing basic savings guidance.

Assuring that EPF members are free to withdraw their retirement savings at 55, even though the retirement age was changed to 60 a decade ago, EPF CEO Ahmad Zulqarnain Onn told editors at a briefing last Thursday (Dec 12) that a new retirement savings benchmark has been introduced to guide members towards achieving better retirement by saving earlier and deferring withdrawals.

Instead of a basic savings amount of RM240,000 (RM1,000 per month for 20 years) by 55, that it has kept to since Jan 1, 2019, the EPF said it now recommends that members aim for at least RM390,000 in basic savings by 60. It is even better if members can achieve what it calls “adequate” savings of RM650,000 or “enhanced” savings of RM1.3 million by 60, it added (see table 1).

Even RM1.3 million is not ideal, Ahmad Zulqarnain said, noting that one needs RM1.4 million today to have the purchasing power of RM1 million in 2007, with inflation rendering the amount to only RM712,000 today.

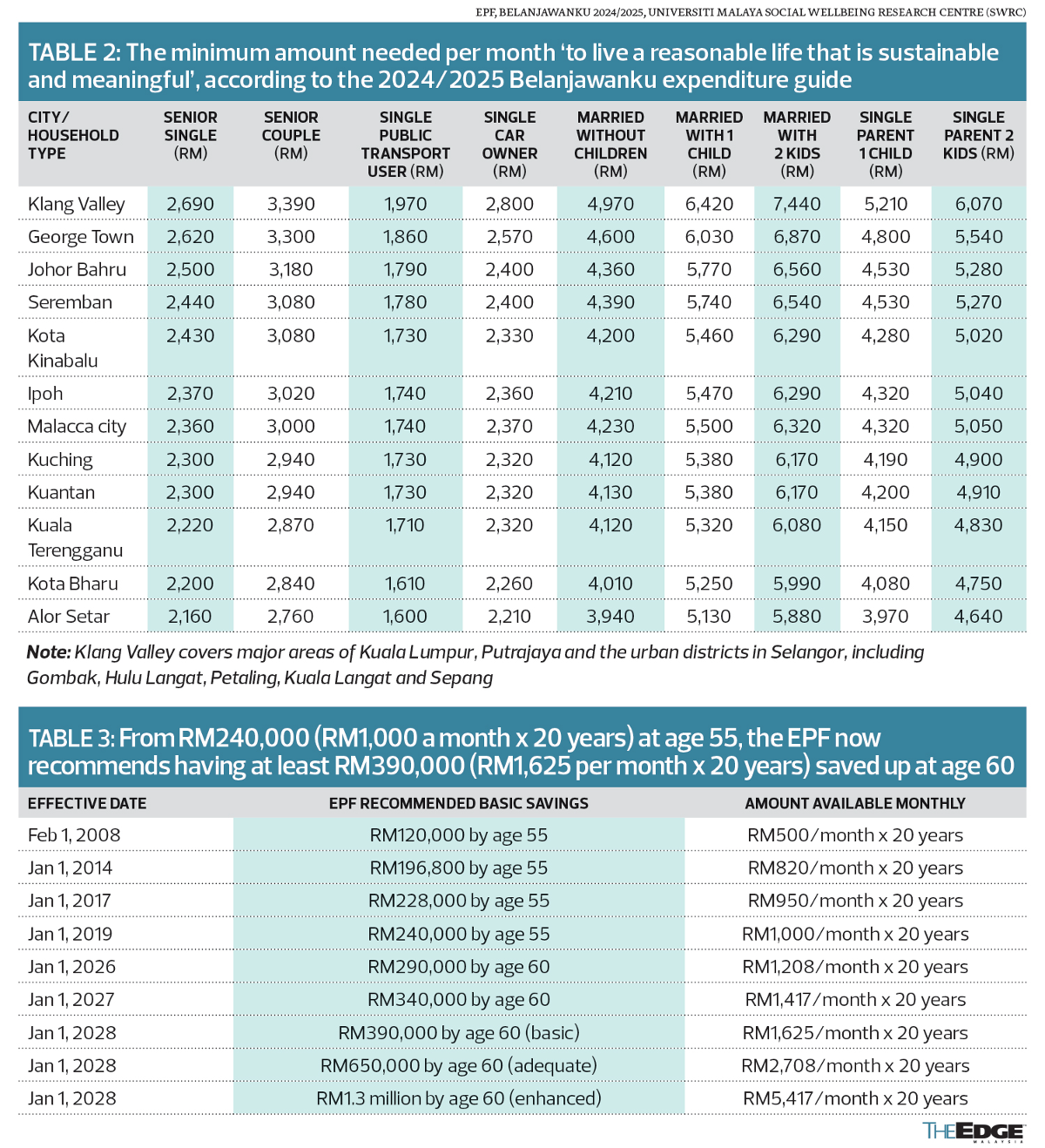

The adequate savings of RM650,000 (which works out to RM2,708 per month for 20 years) is calculated from an updated estimate minimum monthly expenditure of RM2,690 that a single senior citizen living in the Klang Valley would need “to live a reasonable life that is sustainable and meaningful”, according to Prof Datuk Norma Mansor, director of the Universiti Malaya Social Wellbeing Research Centre (SWRC) that produced the Belanjawanku 2024/2025 expenditure guide covering most major cities in collaboration with the EPF.

It’s no surprise that Belanjawanku found that a senior citizen living in the Klang Valley would need the most money to achieve decent living standards at RM2,690 a month, followed closely by RM2,620 in Georgetown, Penang. In third place is Johor at RM2,500 per month while it is cheapest in Alor Setar, Kedah at only RM2,160 (see table 2).

According to Ahmad Zulqarnain, just as a civil service pension is 60% of the last drawn salary, the new recommended basic savings of RM390,000 by age 60 is 60% of the RM650,000 that the EPF sees as adequate savings. The new enhanced savings of RM1.3 million is simply double the adequate amount.

As the new basic savings threshold of RM390,000 by age 60 is too big a jump from RM240,000 by age 55, the threshold will only apply from 2028. In the interim, the EPF will have a transition basic savings of RM290,000 by age 60 from 2026 and RM340,000 by age 60 from 2027.

Because of the five years between age 55 and 60, the power of compounding interest could still work in favour of an EPF member who chooses to withdraw their savings later at 60, instead of 55 when they are allowed to. The EPF’s head of policy and strategy Balqais Yusoff said the number of EPF members who can achieve the new basic savings threshold at 60 will only drop to 35% compared with around 36% of active formal EPF members who meet the existing RM240,000 basic savings threshold at 55.

“While this percentage may be impacted with the new benchmarks in the medium term, the adjustments are essential to help members’ savings keep pace with the rising cost of living and the current retirement age in Malaysia,” Ahmad Zulqarnain said in a statement.

At press time, the EPF had yet to say how many members would have RM294,000 by age 55 to have a chance of attaining RM390,000 by age 60 (see table 3). Simple logic dictates that the number will be lower than 35%.

EPF data show only 663,631 or 7.8% of its 8.5 million active members having more than RM300,000 in savings as at end-2023, excluding dividends for that year.

EPF data also show half of its 107,311 active members at age 54 having less than RM154,366 savings, even though a simple average shows each of them having RM275,945 savings, on average — likely due to a concentration of higher balances among top savers.

New RM1.3 mil threshold

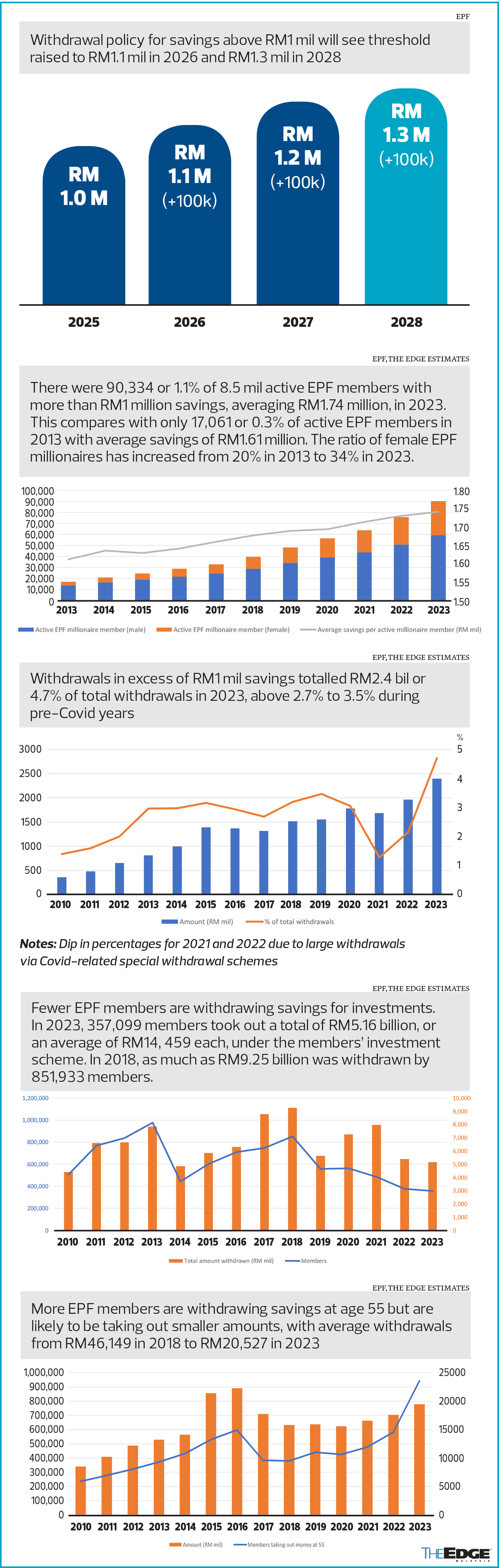

With the introduction of its enhanced savings threshold of RM1.3 million, the EPF will also increase the threshold at which EPF members can take out excess savings at any time from the current RM1 million to RM1.1 million from Jan 1, 2026, RM1.2 million from 2027, and RM1.3 million from 2028.

Among its 8.5 million active members, only 90,334 or 1.1% have more than RM1 million savings as at end-2023, according to EPF data. Some 31,059 or 34% are women while 59,275 or 66% are men. They collectively have 18.1% of the RM867 million savings with active members, which translates to a simple average of RM1.74 million per EPF millionaire who are active members.

There are also EPF millionaires who are not active members, meaning those who have not made any contributions in the past year. Ahmad Zulqarnain told editors that there are “about 100,000” EPF members who have more than RM1 million in savings.

In 2013, there were only 17,061 or 0.3% of active EPF members who had more than RM1 million savings. Some 80% were men.

It remains to be seen if there will be a spike in withdrawals above RM1 million in 2025 before the threshold is raised.

EPF data show 63,273 withdrawals made under the “above RM1 million” category in 2023 amounted to RM2.4 billion or 4.7% of total withdrawals last year. Total withdrawals under this category crossed RM500 million in 2012, RM1 billion in 2015, and RM2 billion in 2023, The Edge’s compilation of EPF data shows.

Investment-related withdrawals

The change in recommended basic savings also affects EPF members who withdraw money under the “members’ investment scheme” that allows them to transfer up to 30% of their excess basic savings by age from their retirement account 1 to approved investments.

The amount that can be withdrawn for this purpose might be lower for some members due to a higher basic savings threshold by age with the change in recommended basic savings from Jan 1, 2026.

EPF data show the amount being taken out under the “members’ investment scheme” had already been trending lower even before this change. Only 357,099 EPF members took out a total of RM5.16 billion last year, translating to a simple average of only RM14,459. In 2018, as much as RM9.25 billion was withdrawn by 851,933 members under this scheme, our compilation of EPF data shows.

Low average age 55 withdrawals

Meanwhile, the total amount withdrawn by EPF members at 50, 55 and 60 shows that lower amounts are being taken out, on average, in 2023 compared with prior years. It is not immediately known if that was due to the RM145 billion that had been prematurely withdrawn from the EPF between 2020 and 2023 via the four Covid-related special withdrawals.

It is also not known yet whether more EPF members realise they need to keep their savings compounding for longer, given that the amount withdrawn from the EPF’s Flexible Account 3 between May and November this year of RM11.6 billion is lower than the RM25 billion that the EPF had expected to be taken out when introducing the third account. The RM11.6 billion plus the RM7.4 billion remaining in Account 3 as at Nov 27 this year, that can be taken out in the same no-questions-asked manner, totalled only RM19 billion. This sum is only one-third of the RM57 billion that the EPF had said could be taken out from Flexible Account 3 if every member below 55 had chosen to do so by Aug 31 this year.

At the editors’ briefing, Ahmad Zulqarnain showed examples of how RM1 million in savings can be within reach by 60, mathematically, even if one were to start with a monthly wage of RM1,700.

“It is about persistence and not withdrawing [prematurely savings from the EPF],” he said, asking that more members start saving early and defer withdrawals until after age 60 to harness the power of compounding interest.

Saving early would indeed be ideal. Rather than relying on self-discipline, however, policymakers can make the job a tad easier by adjusting the EPF withdrawal age to match the retirement age — at least for those who have yet to enter the workforce and have ample time to plan their retirement.

Save by subscribing to us for your print and/or digital copy.

P/S: The Edge is also available on Apple's App Store and Android's Google Play.

- Short selling in five counters suspended amid market rout

- Market plunge drags FBM KLCI down over 5%, as East Asian markets sink on trade war concerns

- Asian stock benchmarks drop most in 14 years on tariff concerns

- China has already trade-war-proofed its economy

- Trump team rejects market fears, shows defiance on tariffs

- Trump's tariff 'medicine' injects turmoil into global markets

- Gold drops to 3½-week low as market sell-off hits bullion

- Housing Ministry blacklists 109 property developers for non-compliance, says Nga

- Google Cloud appoints Hana Raja as new country manager

- Anwar: Malaysia must improve its preparedness in facing global economic uncertainties