This article first appeared in Capital, The Edge Malaysia Weekly on December 16, 2024 - December 22, 2024

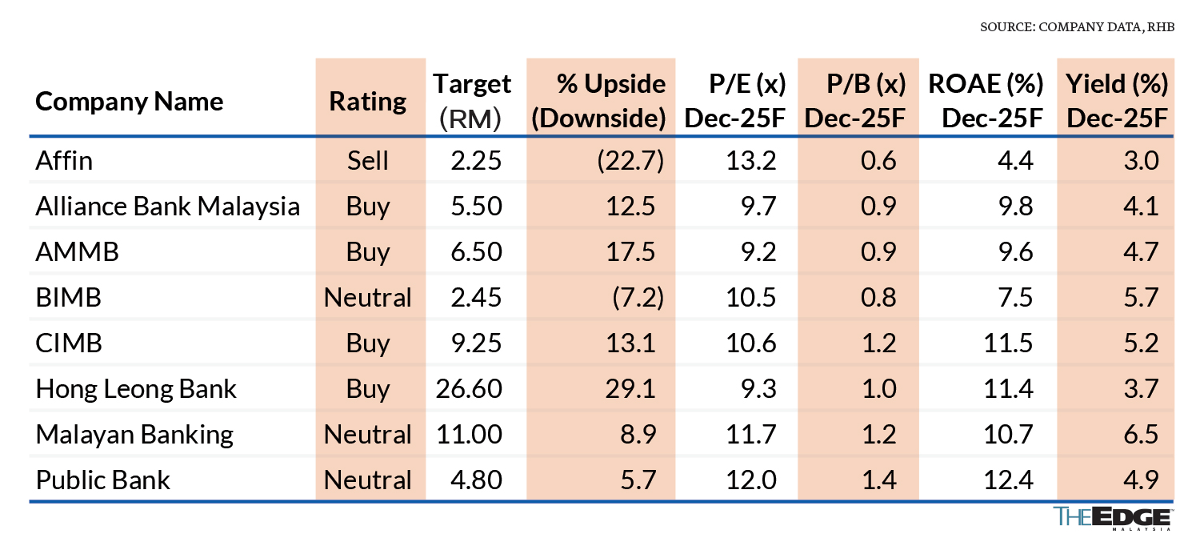

Banks

Overweight (maintain)

RHB RESEARCH (DEC 10): We think market volatility will likely persist amid uncertainties with respect to US policies and the US federal funds rate (FFR) trajectory, among others. Malaysian banks could offer investors a good defensive option to tide themselves through this. Valuations — AMMB Holdings Bhd (KL:AMBANK) and Alliance Bank Malaysia Bhd (KL:ABMB) — and capital management potential — AMMB and CIMB Group Holdings Bhd (KL:CIMB) — underscore our stock-picking framework, while we like Hong Leong Bank Bhd (KL:HLBANK) for its defensiveness.

Sector earnings should prove defensive, with Malaysian banking stocks under our coverage being largely neutral to US FFR cuts and forex movements. In the past, the key drag to sector earnings growth tended to be net interest margin (NIM) and/or credit cost. Banks managed NIM well in 2024 on liquidity and funding cost management, but with the sector loan-to-deposit ratio (LDR) creeping up (latest sector and system LDR are at 93% and 88% respectively), there may not be much room for them to trim deposit rates if loan demand is robust.

With a stable asset quality outlook and a number of banks still holding on to healthy management overlays, there could be continued management overlay reversals to help mitigate potential NIM pressure and support bottom line growth. The sector offers a FY25F dividend yield of over 5%. We think this is attractive, and there could be room for yields to compress further.

Furthermore, amid a stable macroeconomic outlook, better visibility on Basel III reforms, and/or strong capital generation by some banks, these would be positive for dividend payouts and capital management initiatives.

Finally, the sector offers investors leverage to foreign institutional investor (FII) inflows — given that banks, as liquid, large cap stocks, will likely be beneficiaries. Apart from that, some banking groups are set to unveil their mid-term strategic plans next year. We think investors will be watching out for the new return-on-equity targets, with credible ones aiding in the valuation rerating.

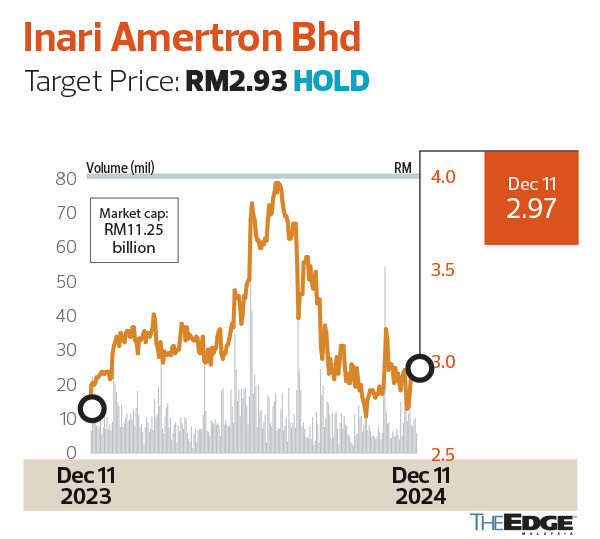

Inari Amertron Bhd

Target Price: RM2.93 HOLD

MAYBANK IB (DEC 10): We assess the risk of Inari (KL:INARI) potentially losing its bread-and-butter radio frequency (RF) business as its main end-customer contemplates in-housing production of its cellular/connectivity chipsets in the future. Although our findings point to the risk being relatively contained at this juncture, we maintain that Inari’s near-term prospects remain challenging due to margin pressures from lower volume loads. Reiterate “hold” with an unchanged target price of RM2.93 (29 times FY26E).

Bloomberg reported on Dec 4 that Apple is finally ready to launch inhouse cellular modems (Sinope) for its low-cost smartphone range in 2025. Apple’s primary supplier for its smartphones’ cellular chipsets (modems/transceivers) is Qualcomm while connectivity chips (FBAR filters) are supplied by Broadcom. We believe the latter is Inari’s key RF customer and accounts for about 70% of its annual group turnover. Despite Bloomberg’s assertion that Sinope will likely be fully utilised in all iPhone ranges by 2027, we opine that Apple is unlikely to in-house radio frequency front end (RFFE) connectivity components in the future due to: (i) low procurement costs and (ii) the risk of IP infringement lawsuits from Broadcom.

While it may seem logical for Apple to in-house the production of its cellular modem (the costliest externally-sourced component), it makes little economic sense for Apple to also in-house RF chipsets. In the medium term, we expect Inari’s RF segment sales to remain resilient on higher content growth, despite the softness in end-demand from slowing iPhone sales in China.

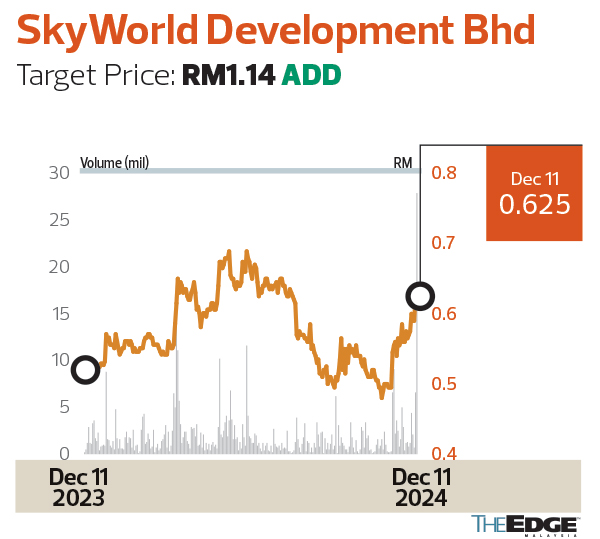

SkyWorld Development Bhd

Target Price: RM1.14 ADD

Kenanga Research (DEC 11): SkyWorld (KL:SKYWLD), whose forte is city high-rise projects, will be venturing into an affordable homes development in Penang with an estimated gross development value (GDV) of RM13 billion — the largest in the country. Though the project will only commence in 2026, investors may react positively to the news as it greatly bolsters the company’s long-term project pipeline and lifts it by end-FY26 out of an otherwise lacklustre earnings phase, which should still endure for a few more quarters. We call “add” with a fair value of RM1.14 with a 30% revalued net asset value discount, which is at par with our applied discount on Mah Sing Group Bhd (KL:MAHSING). Our target price implies a PER of 13 times for FY26, a 30% discount to the average of 19 times forward PER for its peers.

SkyWorld signed a joint development agreement with the Penang Development Corporation (landowner) and its subsidiary PDC Properties in relation to the development of: (i) a 161.5-acre plot in Batu Kawan, and (ii) a 31.3-acre plot in Seberang Jaya. Presently, the group’s project pipeline consists of only four ongoing projects with a total remaining GDV of RM907 million. We opine that with the group’s operations being predominantly Klang Valley-based and wholly dependent on subcontractors for development, the rollout of launches during the early phases of the Penang project would be relatively light, before picking up more substantially over the course of its 15-year development period.

Dialog Group Bhd

Target Price: RM2.61 ADD

CGS INTERNATIONAL (DEC 9): Indonesia-based petrochemical producer ChemOne, the sponsor of the Pengerang Energy Complex (PEC) project at Pengerang, Johor, posted on LinkedIn on Dec 6 that it had hosted financiers from around the world in Kuala Lumpur to “finalise the project financing” for the PEC project, with “strong support from the senior financiers” including the Export-Import Bank of Malaysia Bhd. ChemOne said that it hoped to “achieve financial close for the PEC project by 1Q2025”.

The PEC refinery, if it is built, will be positive for Dialog’s (KL:DIALOG) Pengerang Deepwater Terminal (PDT), as the company will most likely enter into a new long-term take-or-pay tank terminal leasing contract with ChemOne. We think Dialog may build at least 0.45 million cu m (cbm) of new tanks for PEC in PDT’s Phase 3, about one-third of PDT Phase 2’s 1.3 million cbm that is dedicated to PRC and PPC. Separately, we also expect Dialog to announce a new long-term take-or-pay tank terminal leasing contract with the new 12,500 bpd biorefinery that is being built by the joint venture between Petronas, Italian oil major Eni and Japanese biotech firm Euglena. The JV targets the biorefinery to be operational by 2H28F.

In total, the above 0.63 million cbm of additional tanks represent 12% of Dialog’s 5.3 million cbm tank terminal capacity across Kertih, Terengganu, and Tanjung Langsat and Pengerang in Johor.

We expect Dialog’s January-June 2025F (2HFY25F) profits to improve, due to several refinery and petrochemical plant turnaround jobs scheduled, relative to the quieter 1HFY25F. Downside risks include any unexpected dragging out of engineering, procurement, construction and commissioning losses.

Save by subscribing to us for your print and/or digital copy.

P/S: The Edge is also available on Apple's App Store and Android's Google Play.

- China amplifies rebuke of Li Ka-shing’s Panama Port deal with BlackRock

- Batik Air throws support behind Subang Airport's expansion, urges faster slot allocation following AirAsia’s departure

- Forest City expands transportation infrastructure to support SFZ and JS-SEZ

- Gold counters on Bursa Malaysia surge as safe haven demand rises amid concerns over US economy

- Donald Trump makes Chinese stocks great again

- Khazanah-backed TT Vision Holdings says not aware of reason for unusual market activity

- Chemlite closes IPO applications with 28 times oversubscription

- Khazanah to acquire INCJ's stake in tower firm Edotco Group

- Sunway Uni being there for your past, present and future

- Kremlin says Putin sent Trump a message on Ukraine ceasefire idea, talks of 'cautious optimism'