This article first appeared in Capital, The Edge Malaysia Weekly on December 16, 2024 - December 22, 2024

NOTWITHSTANDING the growth in the electronics manufacturing services (EMS) sector amid improved global demand and the increasing outsourcing trend, EMS companies on Bursa Malaysia have turned in a mixed performance owing to rising costs, high inflation and supply chain disruptions.

The movements in the share prices of closely followed EMS counters have reflected the developments in the companies.

For instance, Johor-based SKP Resources Bhd (KL:SKPRES), V.S. Industry Bhd (KL:VS), Penang-based NationGate Holdings Bhd (KL:NATGATE) and P.I.E. Industrial Bhd (KL:PIE) have seen their share prices soar between 47% and 76% year to date (YTD).

Aurelius Technologies Bhd (KL:AURE) and EG Industries Bhd (KL:EG), both headquartered in Kedah, are up 29% and 51% respectively. But ATA IMS Bhd (KL:ATAIMS) and JHM Consolidation Bhd (KL:JHM) are down 8% and 36% respectively.

“EMS players have corrected over the past year and the market has already adjusted for the weak outlook throughout the year. The market is now looking for recovery in this sector and we believe it will come. It’s a matter of when,” TA Investment Management Bhd chief investment officer Choo Swee Kee tells The Edge.

“EMS players ride the global consumer consumption demand. Hence, if global economic growth continues to chug along, demand for EMS services will be sustained. Other than the basic demand-supply dynamic, the current trend to diversify production due to China+1 or Taiwan+1 will benefit Malaysia’s EMS players and we expect this momentum to pick up in 2025. Overall, we are positive on EMS players in 2025.”

For SKP Resources, a recovery in consumer demand has given the electrical and electronics plastics maker a 27% year-on-year (y-o-y) improvement in its net profit to RM34.35 million for its second quarter ended Sept 30, 2024 (2QFY2025), on 22.2% higher revenue of RM635.29 million from RM519.91 million last year.

The company, which is a contract manufacturer for British consumer goods company Dyson Ltd in Malaysia, however, revealed in a statement that it is operating in a challenging business landscape of high inflation that has been weighing on production costs. In addition, it conceded that it is mindful of its heavy reliance on “a major customer” and is seeking to diversify its customer base.

Dyson recently said it intends to streamline its business in the region, including redeploying 47 employees from its advanced manufacturing facility to the global development campus in Johor. This is a move which TA Securities senior analyst Tony Chan Mun Chun believes could be intended for internal resource restructuring to boost efficiency rather than to cut down on its business here.

“We have confirmed with some local EMS companies that the order visibility from Customer D remains very healthy [with] no sign of slowing down. In fact, Customer D is looking to transfer some products from Mexico to Malaysia as it is planning to scale down the operations there,” Chan tells The Edge.

“Dyson’s move will benefit Dyson’s contractors in Malaysia with more business potential. However, we prefer to look way beyond Dyson for better diversification.”

Battling lower sales on a y-o-y basis as well as beaten down margins due to a softer US dollar, V.S. Industry posted a 37.5% y-o-y decline in net profit to RM30.6 million for the first quarter ended Oct 31, 2024 (1QFY2025).

According to PublicInvest Research’s Dec 9 note, V.S. Industry’s US-based customer was undergoing inventory rationalisation, resulting in a slowdown in production until the end of December.

“V.S. Industry’s management has revised its sales growth target higher to 6%, while net margin is estimated to come in the range of 4.8% to 5%, albeit subject to foreign exchange (forex) movements and labour costs,” said the research house, which is sanguine on the company’s outlook. It believes that stronger sales of RM300 million can be expected from a particular customer after the company bagged a contract for two new models in Malaysia.

“Meanwhile, the majority of V.S. Industry’s customers have given positive feedback on their respective outlook, led by more product launches. There is also the possibility of more products being transferred from Mexico to Malaysia by the said customer as it plans to shut down operations there. The strong earnings recovery is only expected to kick in by the second half,” says PublicInvest Research, which is maintaining its “trading buy” call on the stock with an unchanged target price (TP) of RM1.18 based on 15 times FY2026 forecast earnings per share.

To manage its expectations for the year ahead, RHB Research cut its earnings forecast for V.S. Industry’s financial year ending July 31, 2025 (FY2025) by 14% to RM233 million. But it maintained its forecasts for FY2026 and FY2027 as it viewed the Johor-based player’s job order prospects positively and foresees a recovery in demand and product launches lined up by key customers.

Meanwhile, there has been considerable scrutiny of Cape EMS Bhd’s (KL:CEB) prospects as the ACE Market-listed player’s share price was nearly halved to 41 sen in the first week of August following a slew of margin calls suffered by its group CEO and managing director Christina Tee. Her stake was slashed by more than a third from 38.4% to 11.1%, purportedly on the back of financial misguidance by the management to some institutional investors, leading to the selldown.

Cape EMS’ performance did not help its share price as it slipped into the red with a headline net loss of RM19 million in the third quarter ended Sept 30, 2024 (3Q2024), impacted by a RM12.6 million unrealised forex loss, RM4 million amortisation of intangible asset and RM2.2 million impairment on trade receivables. Following the results announcement, the counter sank further to 36 sen from 39 sen.

Cape EMS’ beaten down share price has reportedly drawn investment interest from the likes of Ekuiti Nasional Bhd (Ekuinas), which is believed to be mulling over a stake in the Johor-based EMS player.

In addition, businessman Chung Chee Yang started to accumulate Cape EMS shares on the open market and emerged as a substantial shareholder on Nov 13. As at Dec 10, he increased his stake to 8.3%, or 82 million shares, in the company.

Meanwhile, the Employees Provident Fund, which had emerged as a substantial shareholder on July 26, ceased to be one on Aug 15 after selling a portion of its shares.

Another player attracting interest is Penang-based EMS provider NationGate because of its improved bottom line. For the third quarter ended Sept 30, 2024, it saw a net profit of RM46.6 million on the back of RM1.4 billion in turnover, primarily driven by its data computing segment.

Interestingly, there have been concerns about the company’s future profitability as its net profit was heavily influenced by unrealised forex gains amounting to RM76.2 million for the quarter and RM142 million for the first nine months of the year. Had it not been for the forex gains, the company’s core operations might have faced a net loss.

Nevertheless, Kenanga Research believes the group is well positioned to benefit from the strong artificial intelligence (AI) server demand in the data computing segment and is poised for a recovery in its networking and telco divisions in FY2025. The research house has an “outperform call” on the counter with a TP of RM2.30 based on an unchanged FY2025F PER of 25 times.

“This represents a 30% premium to peers’ forward mean, justified by the group’s favourable exposure to the fast-growing networking product segment and its advanced capabilities, which yield better margins as well as enhance customer stickiness,” it says.

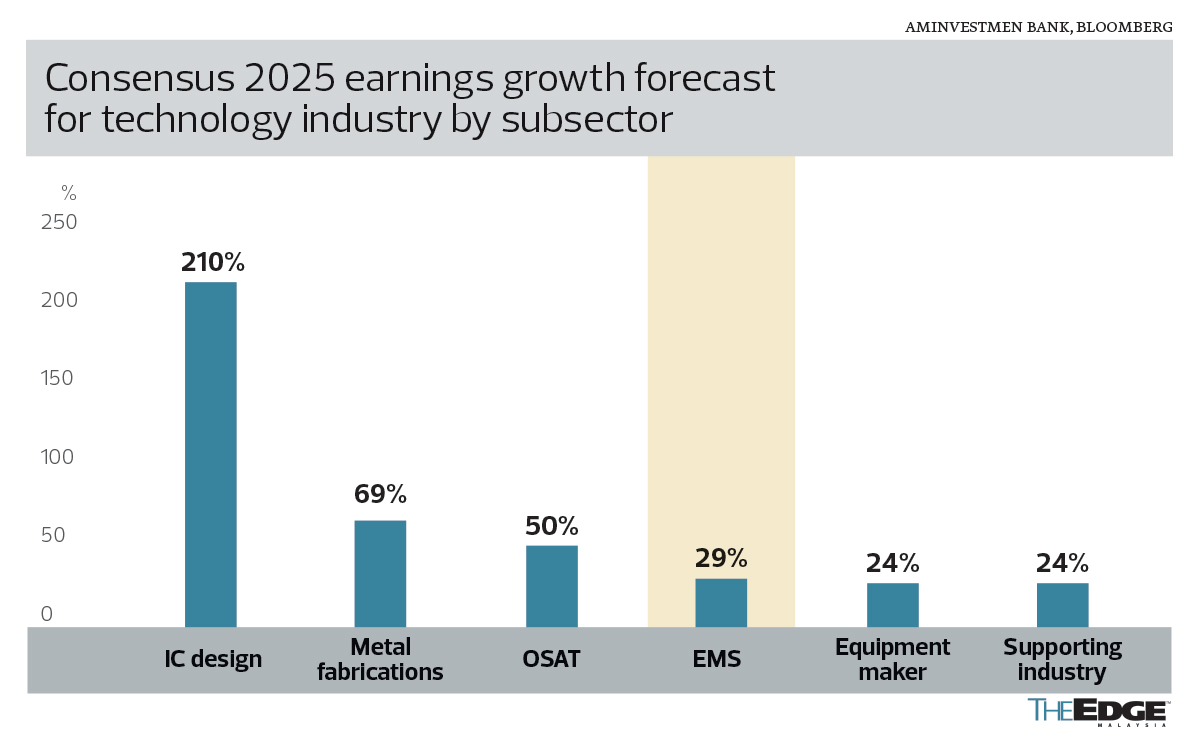

EMS players part of tech up cycle

Analysts have predicted for some time that the technology sector is poised for an up cycle starting in the second half of this year.

AmInvestment Bank Research said in a Dec 4 report that “interest will return to Malaysia Tech in 2025, given its relatively low holdings in investor portfolios, reasonable valuations and still positive long-term structural prospects”.

“While there is value, we advise investors to be selective, as high earnings expectations remain a key risk. We favour stocks with earnings certainty (via secured orders) or those that have been oversold, provided they have a clear strategy and long-term vision. The conclusion of the US elections and prospects of higher tariffs are a structural tailwind for Malaysia as local companies can benefit from supply chain relocation activities,” said the research house, which is “overweight” on the technology sector.

It has “buy” calls on ViTrox Corp Bhd (KL:VITROX), V.S. Industry, Malaysian Pacific Industries Bhd (KL:MPI) and Greatech Technology Bhd (KL:GREATEC), with TPs of RM4.75, RM1.45 (from RM1.05), RM33.10 (from RM38) and RM2.60 (from RM5.53) respectively. It has “hold” calls for Pentamaster Corp Bhd (KL:PENTA) and Inari Amertron Bhd (KL:INARI), with TPs of RM3.50 and RM2.40 (from RM4.36) respectively.

As for the susceptibility of consumer-centric EMS companies to a potential economic slowdown on the back of weaker consumer sentiment, Choo says: “Our base case scenario is that with [US president-elect Donald] Trump in office, there will not be a US recession in 2025 and consumer demand should remain sustained. We are positive on the EMS sector due to its potential business recovery, corrected share price and the added factor of taking market share from China and Taiwan contractors.”

Save by subscribing to us for your print and/or digital copy.

P/S: The Edge is also available on Apple's App Store and Android's Google Play.