KUALA LUMPUR (Dec 16): Yinson Holdings Bhd (KL:YINSON), whose share price dropped nine sen in the morning session on Monday, is expected to see strong earnings ahead, as it gears up to deliver multiple major floating production storage and offloading (FPSO) units, with new opportunities on the horizon, said analysts.

“Profit wise, we think that the worst is over,” said Maybank Investment Bank, adding that FPSO Atlanta is anticipated to begin earning maiden charter revenues by the end of this month, followed by FPSO Agogo, slated for first oil in the fourth financial quarter ending Jan 31, 2026 (4QFY2026E).

The transition away from heavy capital expenditure cycles marks a significant inflection point for Yinson, with Maybank describing this as a “re-rating catalyst,” reducing risks associated with construction, cost overruns, and delivery delays.

Maybank noted that the FPSO market is experiencing a “golden age,” with 13 global tender awards expected in the next 12 months. It said in the research note that Yinson reportedly targeted at least one new mid-sized project in the financial year ending Jan 31, 2026 (FY2026), focusing on bankable opportunities with high upfront payments from clients.

However, Yinson’s core net profit for the nine-month period ended Oct 31, 2024 (9MFY2025) came below both Maybank and CIMB Securities Sdn Bhd’s expectations due to a dip in engineering, procurement, construction, installation & commissioning (EPCIC) earnings. In view of that, both Maybank and CIMB Securities have revised downwards their earnings forecasts to account for lower EPCIC revenue and profit assumptions, while maintaining a “buy” call for the stock.

CIMB opined that the FPSO operator, among the top players in the world, is expecting to see FPSO Atlanta slated to achieve first oil by next month, after FPSO Maria Quiteria which saw first oil in October, with projected revenue and net profit to be around RM240 million-RM250 million, and RM70 million-RM75 million, respectively.

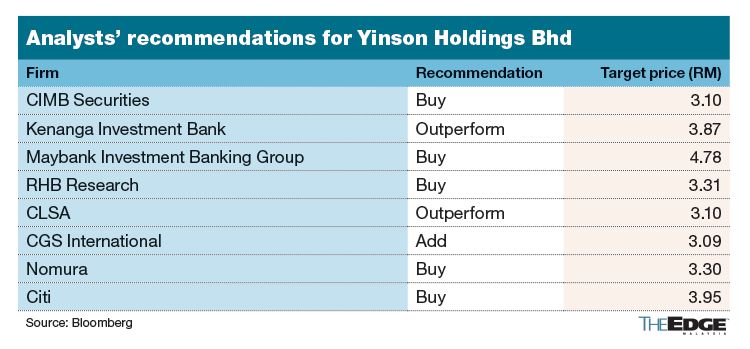

Analysts remain bullish on Yinson. Seven analysts tracking the group have either “buy” or “outperform” calls on the stock. The consensus 12-month target price is RM3.60, according to Bloomberg, implying a potential return of 35.8% from the current price of RM2.65. The record high of Yinson’s share price was at RM2.96 in February 2020.

CIMB, while lowering its target price to RM3.10 from RM3.16, also trimmed Yinson’s core net profit forecast for FY2025 and FY2026 by 19.4% and 13.7%, respectively.

However, the research house projected a robust 56.9% year-on-year core net profit growth in FY2027, underpinned by full-year contributions from FPSO Agogo.

While Yinson’s order book currently stands at US$22.1 billion, stretching to 2048, CIMB cautioned that potential delays in FPSO conversions and cost overruns remain key risks, but successful asset monetisation, or timely delivery of first oil from its FPSOs could act as critical catalysts for further stock re-rating.

Kenanga Research, however, raised its target price and earnings forecasts.

In a financial result review, Kenanga Research, which has retained an “outperform” call on the stock, cited that Yinson’s 9MFY2025 results came in better than expected, while revising its target price upwards by 8% to RM3.87.

The research unit raised the earnings forecast for FY2025/FY2026F by 14%, to reflect higher lease income from FPSO Maria Quiteria and FPSO Abigail Joseph.

“The outperformance was primarily driven by rate escalation from FPSO Abigail Joseph,” said Kenanga, who noted on Yinson’s single interim dividend announcement of one sen per share.

Looking ahead, Yinson may be eyeing to secure one- to two mid-sized FPSO projects within the next year, with projected capital expenditures of US$1 billion to US$2 billion, focusing on Africa and Asia, said CIMB.

Key projects include Baleine (Eni) and Paon (Murphy Oil) in Ivory Coast, PTTEP’s Kikeh project in Malaysia, and Namibia’s Orange Basin PEL 83 project (Galp Energia).

Yinson saw 3.29 million shares exchanged hands on Monday as the counter fell eight sen to RM2.60 at market close, valuing the group at RM8.33 billion.