This article first appeared in The Edge Malaysia Weekly on October 14, 2024 - October 20, 2024

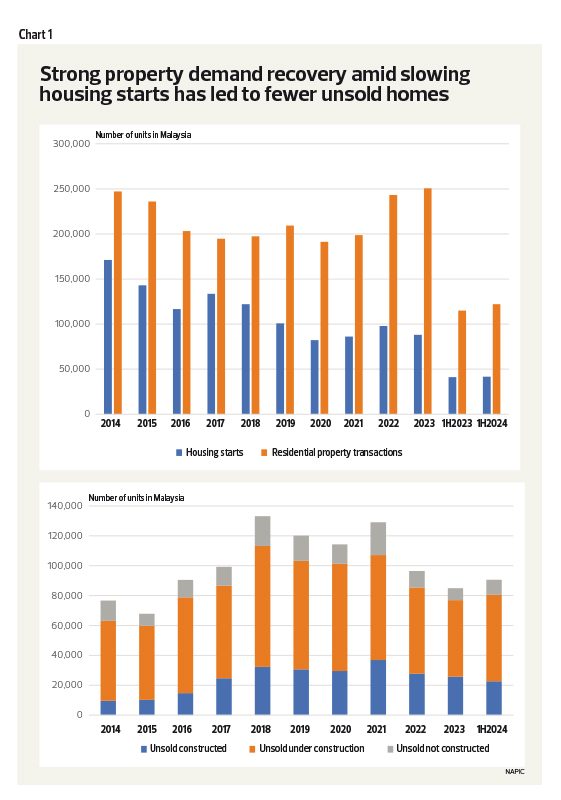

The Malaysian property sector recovery remains intact based on the most recent available statistics. Residential property sales (by value) are rising nationwide, on the back of increases in both volume demand and prices, and — this might come as a shock to many — underpinned by improving home affordability, contrary to popular misconception that is often perpetuated by the media and even government authorities. At the same time, unsold units are decreasing, boosting homebuyer confidence in the sustainability of this recovery and overall sentiment for the sector. All the data are supportive of the property sector’s turnaround after years of sluggish demand and lacklustre outlook following the Developer Interest Bearing Scheme (DIBS) bubble burst.

To briefly recap, the DIBS scheme, introduced in 2009, allowed developers to absorb all the interest costs on mortgages during the construction period. The resulting “free holding cost” during the construction period for homebuyers drove massive speculative activities — buyers bought properties with the intention to flip them on completion — causing prices to surge and making homes rapidly unaffordable. The DIBS scheme was abolished in Budget 2014. That led to a sharp contraction in demand — the number of transactions fell — amid incoming supply. Unsold units piled up, exerting downward pressure on home prices and eroding buyer confidence. Home prices became stagnant, and even fell in some market segments, including high-rise and high-priced properties. It took years for the property market to rebalance and regain its footing. Demand did not start recovering until around 2018 but was interrupted by the Covid-19 pandemic.

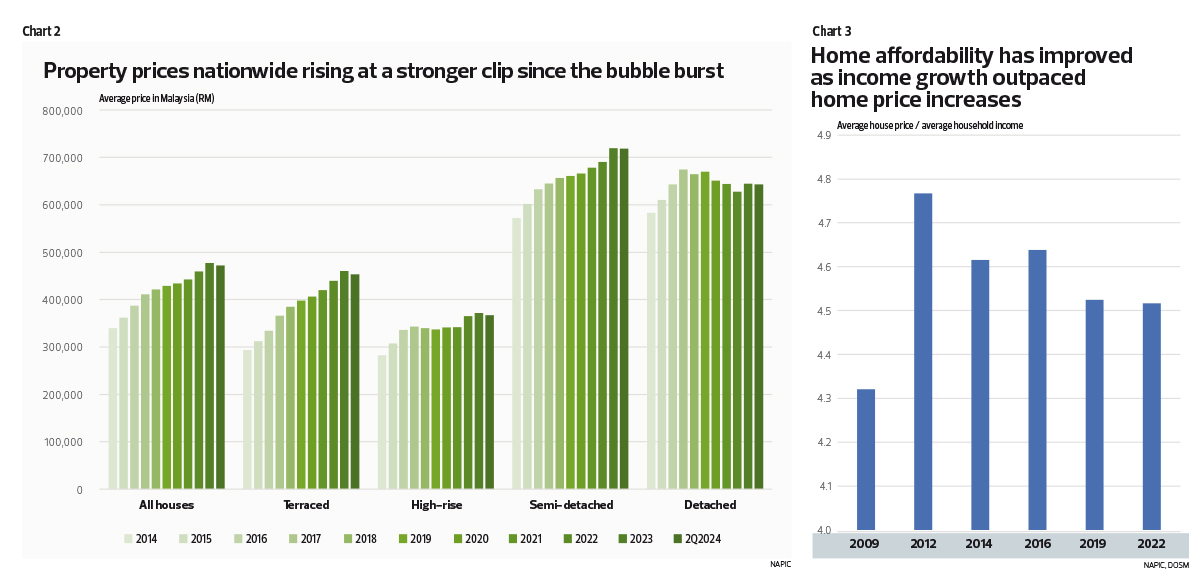

The post-pandemic property sales in 2022-2023 have been strong, even after taking into account effects of pent-up demand (that would taper off) — y-o-y growth remains positive in 1Q2024. Developers have also been generally more disciplined in launching new projects. As a result, unsold stock across the country fell on the back of the recovering demand and fewer housing starts (see Chart 1). And home prices are rising now at a faster clip across all market segments (see Chart 2) — not just because of stronger demand but also due to rising costs, including wages.

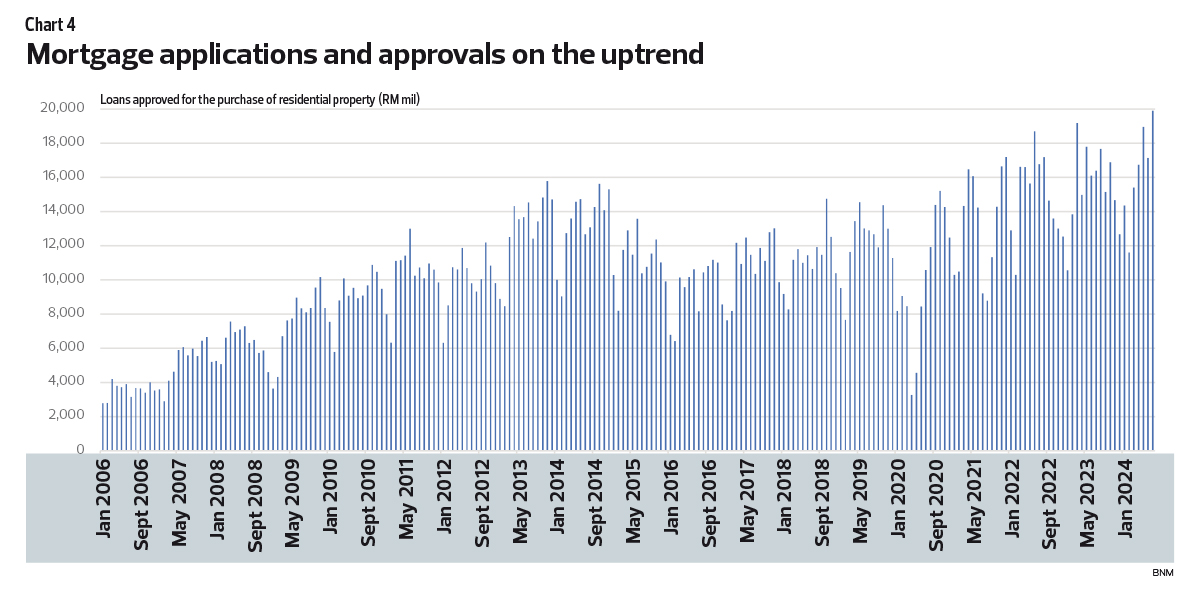

As we said, home prices have stayed somewhat flattish for years after the DIBS bubble burst. While this has affected buyer confidence and resulted in a lacklustre property market, it has also allowed income to catch up with the DIBS-driven price surge (in 2009-2012). Household income grew faster than house prices from 2012 to 2022. As a result, home ownership affordability in Malaysia, on average, improved over this period — that is, the ratio of average home price to average household income fell (see Chart 3). Improving affordability underpinned the rise in mortgage applications and loan approvals — loan approvals continued to trend higher, up to the latest June 2024 figures (see Chart 4).

All of the above data supports our belief, which we articulated back in February, that the worst is over for the residential property market. We think demand and prices will continue to trend higher going forward, supported by Malaysia’s favourable demographics including a growing population and the number of households. Of course, there will be some differences in terms of the degree of improvement among the states.

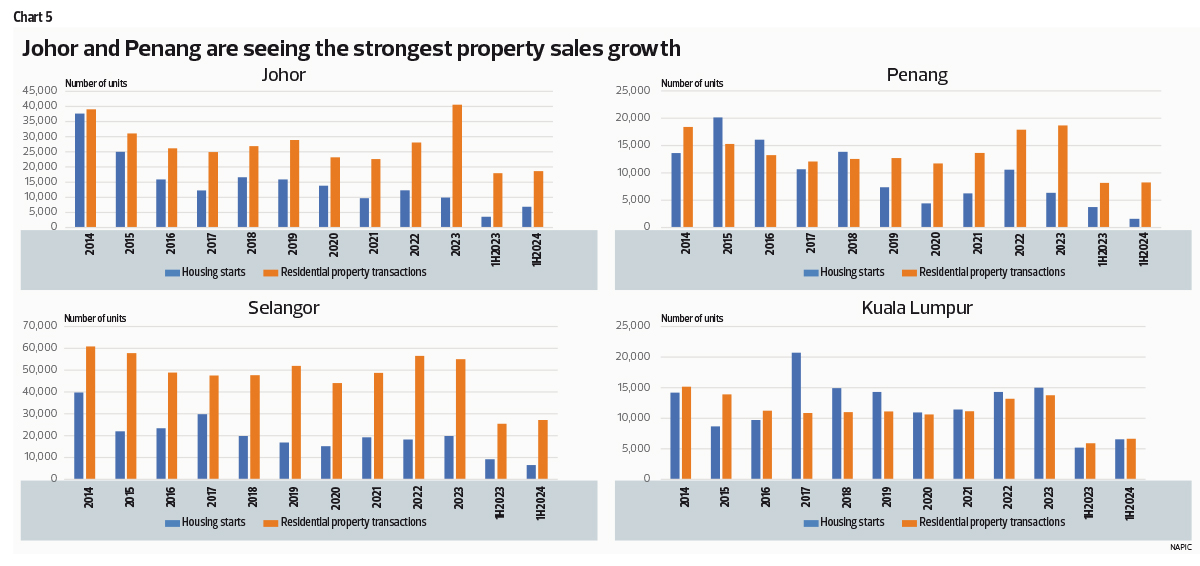

We took a closer look at the property data by states. The demand recovery appears to be strongest in Johor (75% increase in residential transactions between 2020 and 2023), followed by Penang (+59%) while that in KL (+30%) and Selangor (+25%) are comparatively slower, but still relatively robust (see Chart 5).

This is perhaps not surprising given the positivity surrounding the Rapid Transit System (currently under construction and slated for completion by end-2026) and the potential for greater economic integration between Johor and Singapore spurring renewed interest from homebuyers, including Singaporeans. Penang too is drawing buyers on the promise of increased investments and stronger growth in the electrical and electronics (E&E) sector. The state is developing a number of new industrial parks such as Bandar Cassia Technology Park (155ha), Batu Kawan Industrial Park 3 (252ha) and Penang Science Park South (71ha), with a total investment cost of RM3.2 billion — and is attracting more than its fair share of foreign direct investment (FDI).

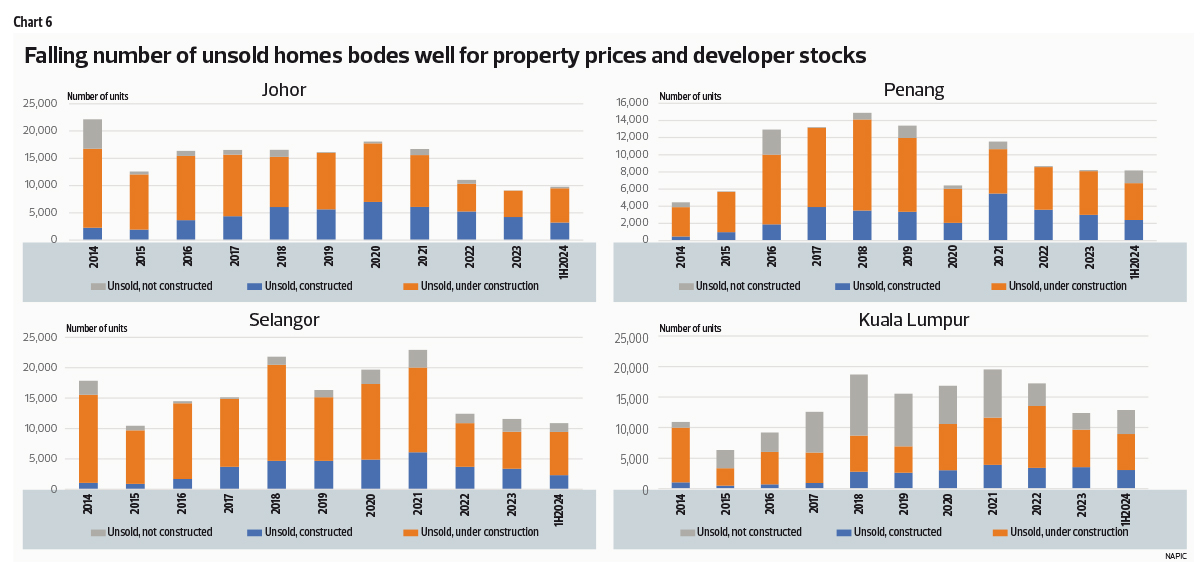

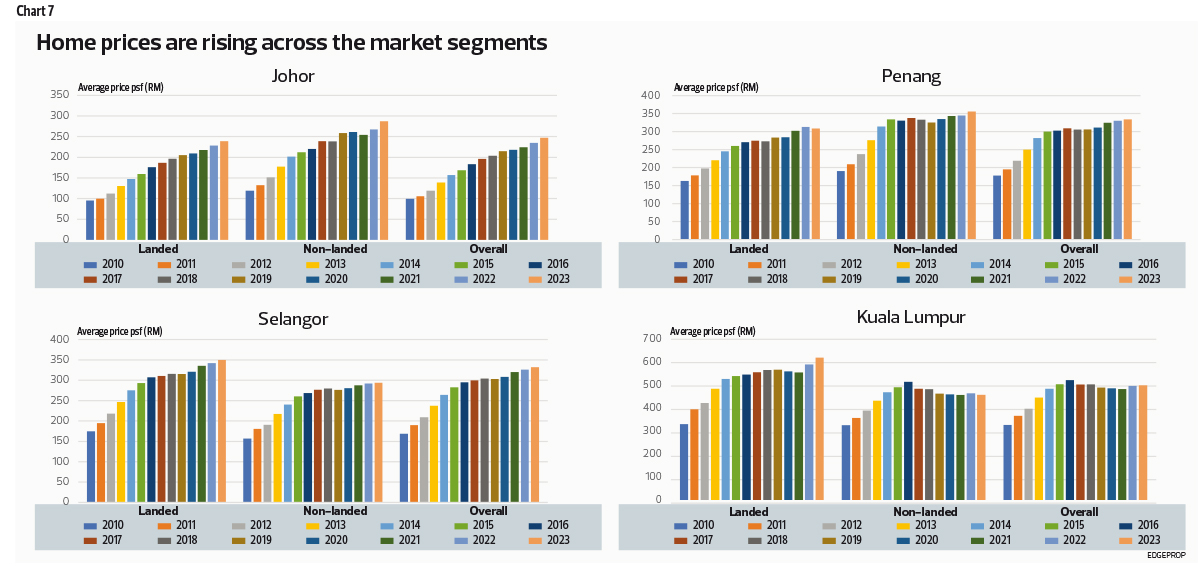

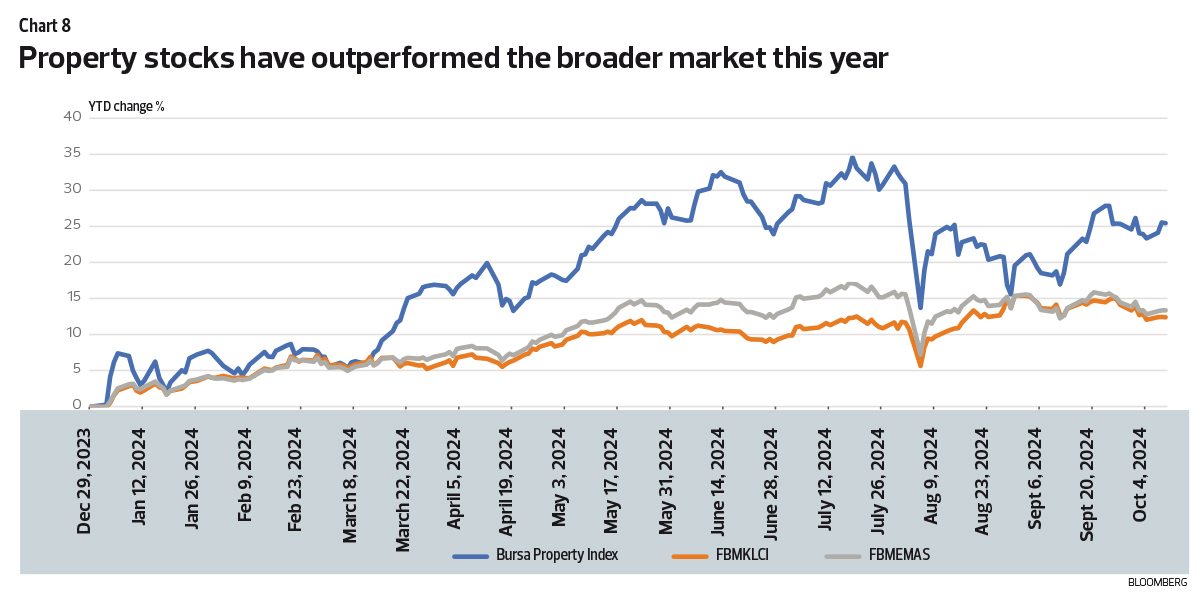

At the same time, the number of new housing starts in Johor and Penang too have fallen the steepest from the highs in 2014-2015, leading to lower unsold homes (see Chart 6) — and prices are rising across all market segments (see Chart 7). Stocks for property developers — especially those with exposure to the two states — as well as the large construction companies have already rallied strongly in anticipation of a more buoyant Malaysian residential property market going forward (see Chart 8).

The Absolute Returns Portfolio fell 1.8% for the week ended Oct 9, paring total returns since inception to 12.9%. The top gainers for the week were CrowdStrike (+6.5%), DBS Group Holdings (+1.5%) and CRH (+0.6%), while the top losers were Tencent Holdings (-7.7%), Swire Properties (-6.7%) and Itochu (-3.7%).

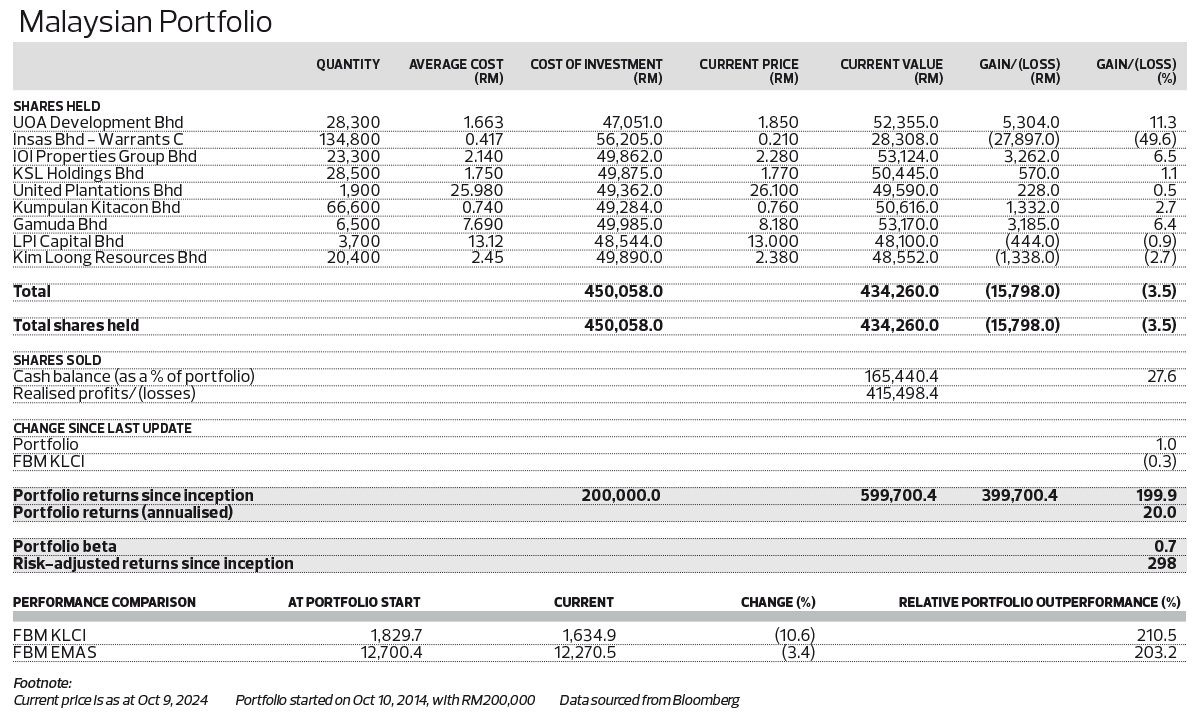

The Malaysian Portfolio gained 1.0%, performing better than the benchmark FBM KLCI, which fell 0.3%. IOI Properties Group (8.1%), Kim Loong Resources (3.5%) and Gamuda (2.9%) were the top gainers for the week; while the biggest losers were KSL Holdings (-0.7%) and LPI Capital (-5.3%). Total portfolio returns now stand at 199.9% since inception. This portfolio is outperforming the FBM KLCI, which is down 10.6% over the same period, by a long, long way.

Disclaimer: This is a personal portfolio for information purposes only and does not constitute a recommendation or solicitation or expression of views to influence readers to buy/sell stocks. Our shareholders, directors and employees may have positions in or may be materially interested in any of the stocks. We may also have or have had dealings with or may provide or have provided content services to the companies mentioned in the reports.

‘Unintelligent’ prescription might end up killing the patient

As we were doing research for our main article on the Malaysian property sector, this headline caught our attention. The writer, Ashraf Abdullah, a former group managing editor of Media Prima TV Networks, articulated the reasons why the government must impose an indefinite moratorium on the construction of high-end houses and compel developers to build affordable homes — as the way to help Malaysians achieve their dream of homeownership.

“Malaysia has witnessed a troubling trend in its housing market: an oversupply of high-cost houses juxtaposed with a glaring shortage of affordable homes. A moratorium on the construction of more high-cost houses is prudent. It will enable the market to absorb the existing inventory, ensuring that property prices not only stabilise but also stop declining.”

As our readers well know, we are data-driven analysts. Hence, we were perplexed. Our first reaction was, is there an oversupply in high-cost houses and shortage in affordable homes? Here is what the data tells us. Chart 1 shows the number of unsold residential houses as at 1Q2024, broken down by price range. It is very clear that the highest percentage of total unsold units are in fact those priced under RM300,000, followed by those priced between RM300,001 to RM500,000. Even more so, most of these unsold affordable homes are recent launches. By comparison, many unsold high-priced units are “old stock” from before the DIBS bubble burst.

Hence, contrary to Ashraf’s claim, there is ample supply of affordable homes in the market. Developers are building lower-priced homes — the problem is they are not selling. The perception that developers are not building what the market needs could not be more wrong. Private sector property developers are profit-maximising entities. Of course they are and nobody would expect otherwise. But property developers don’t profit from simply building the homes, they only make a profit when the homes sell! A 30% margin on zero sales = zero profit (in fact, worse as they would be saddled with unsold stock). Hence, to say that developers only build high-margin luxury homes even when there is no demand makes zero sense. In fact, it is “unintelligent”.

Yes, we must address the issue of homeownership. It is the right of every individual to own a home, if they so wish. But the correct question should be, why aren’t more people buying these unsold affordable homes? Is it because of the location, quality, facilities and amenities, logistics or is it the fact that there are segments of the population, the low-income or first-time young buyers, who simply cannot afford commercially built homes? More in-depth research and analysis is required to truly understand the root cause — so that the correct policies can be implemented. Don’t prescribe medication without knowing the real cause of the illness — you might kill the patient!

We feel compelled to point out that Ashraf’s claims that the number of unsold residential properties (26,286 units in 2Q2023) would have risen significantly by now and likely continue to escalate, leading to declining property prices and thus, raising the risks to developers, the financial system and Malaysian economy, are also wrong. The fact is that unsold residential properties have been decreasing since hitting a peak of 36,863 units in 4Q2021. There were 24,208 unsold homes as at 1Q2024 (see Chart 2). And the Malaysia House Price Index has been rising over the past 10 years — home prices are broadly higher across market segments. This is why we are upbeat on the property sector, as articulated in the main article.

A budget 2025 proposal: Providing at least 80,000 families every year with grants to own their first homes

Homeownership and affordability is a pressing issue in many countries across the world today. As we have written time and again, the ability to own a home is a fundamental human right, not a privilege. On a positive note, for the majority of Malaysians, affordability is not an issue with the homeownership rate at a reasonable 77%. Nonetheless, we should always aim to do better — to help the segment of the population where homeownership is currently still beyond their reach. Here is our proposal to help at least 80,000 families own their first homes each year — with a housing grant.

Prevailing misconceptions on homeownership affordability

We have established that developers are building affordable homes and there is no shortage. It is not a matter of the developers not meeting market demand. The fact is affordable homes (those priced below RM300,000) make up the bulk of unsold residential homes. See Chart 1 in “Unintelligent prescription might end up killing the patient”.

Another misconception that has been gaining traction in recent years is that renting is better than owning, on the basis that Malaysian households are already over-leveraged. This proposition could not be more wrong! There are good debts and bad debts. Borrowed money used to buy assets that depreciate in value are bad debts. Taking a mortgage to buy a home is good debt — it is a form of forced savings. Homeowners are building equity (wealth) for the longer term. Rental is an expense. Furthermore, homeownership is good for democracy. It also expands the middle class and the number of taxpayers over time.

The real reasons why some Malaysians cannot afford to own homes

In fact, housing in general in Malaysia is NOT unaffordable. Banks will typically lend the equivalent of up to 30% of a person’s gross income to service the monthly payments towards home mortgages. Based on this criteria, the minimum monthly household income to qualify for a mortgage to buy a RM200,000 home is RM2,840, a RM250,000 home is RM3,550 and a RM300,000 home is RM4,260. The median household income in Malaysia was RM6,338 in 2022 while nearly 90% of households earned more than RM2,840 a month. So why are some Malaysians still finding it difficult to buy a home?

To be sure, some cannot qualify for a mortgage because they have inconsistent income or insufficient proof of a steady income, poor credit card repayment track record and so on. But one of the main reasons is that many simply don’t have the lump sum savings to pay for the 10% deposit on a new home, whether because they have little income left over to save after cost of living (including paying rental) expenses, lack the discipline to consistently save a percentage of their disposable income, or have just started working (the younger generation).

Additionally, homebuyers would have to start servicing the mortgage drawdowns during the three-year construction period — while still having to pay rent on their existing rented premises. In effect, they would be paying double for the cost of housing for up to three years.

The solution

Give a “once-in-a-lifetime, first-time homebuyer” grant to pay the 10% deposit on a home — up to RM30,000 per married couple (for a RM300,000 home) or RM15,000 for single Malaysian citizen. To qualify for the grant, the monthly household income must be less than RM5,000. And subject to the homebuyer successfully getting a mortgage from a bank as well as completing a financial literacy course. A society where the population is financially literate will go a long way in ensuring a sustainable and resilient economy.

Additionally, to address the double payment for cost of housing during the construction period, defer all interest payments on the mortgage until the home is completed. These deferred interest payments can easily be added to the principal amount, and repayment spread over the life of the mortgage, serviceable upon completion of the home. The resulting increase in the monthly mortgage payments is relatively small and manageable (RM60 per month based on our simulation in Table 1).

Funding for the grant scheme

Of course, the grant scheme must be funded, to avoid raising the budget deficit further. How?

Levy a 1% transaction tax on all property transactions, which totalled RM200 billion in 2023. This will raise RM2 billion annually, to be channelled into a special purpose vehicle (SPV) for the housing grant. Assuming an average grant of RM25,000, this plan will support at least 80,000 families to become homeowners each year. To avoid burdening the home sellers, legislate agent commission (currently ranging between 2% and 5%) to a maximum 2% by limiting tax deductibility. This will also reduce current unscrupulous “overselling”, which ultimately is paid for by buyers.

Notably, a “transaction tax” is not wealth or income tax. And developers should not be unhappy since the expected increase in sales will clear the backlog of unsold homes. Furthermore, new residential home sales account for only RM25 billion of the total RM200 billion in annual property transaction value.

Summary

This housing grant scheme will make homeownership affordable for at least 80,000 families each year. It is simple and efficient. The government should NOT build affordable homes (lesson: the failure of PR1MA) or lend money to B40 to fund their homes (lesson: repayment issues now facing PTPTN). Leave the property developers and banks to do what they do best, building homes and lending to the people.

Giving grants to help raise homeownership is a growing global trend. The Singapore government gives up to S$120,000 housing grants for eligible first-timer families and up to S$60,000 for first-timer singles. In the US, Democratic presidential nominee Kamala Harris has proposed a housing plan that gives up to US$25,000 in downpayment assistance for first-time homebuyers. Malaysia can do the same to further raise the homeownership rate.

Save by subscribing to us for your print and/or digital copy.

P/S: The Edge is also available on Apple's App Store and Android's Google Play.

- Gas pipeline blaze: MIDF flags potential RM18m impact to Petronas Gas

- Gas pipeline blaze: Petronas Gas, Gas Malaysia’s shares open marginally lower after trading halt

- T7 Global drops to two-year low, triggers short-selling halt after deputy chairman's departure

- Digital banks in Malaysia urged to re-examine strategies to better serve B40 segment

- Yinson's shares slip, analysts tell investors to look past underwhelming results

- Gas pipeline fire: No abnormalities detected by air quality monitoring stations — DOE

- A supply chain quirk helped Air India get 50 Boeing jets made for Chinese carriers

- Police to investigate contractor in connection with gas pipeline fire at Putra Heights

- New law subjects 17 Singapore transport firms to greater govt scrutiny

- India's March palm oil imports rise but stay below normal levels, dealers say