KUALA LUMPUR (Sept 24): RHB Research advised a selective approach to the non-bank financial sector amid upcoming catalysts, including the anticipated US Federal Reserve rate cut cycle and a civil servant salary revision in Malaysia.

While maintaining a 'neutral' call on the non-bank financial sector, the research firm said not all players stand to benefit from the catalysts equally, as the valuation profiles across companies remain varied.

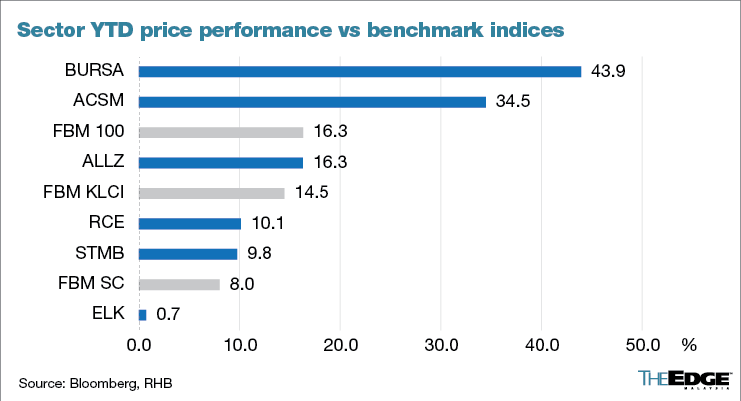

“Valuation profiles are mixed across the sector, so we advocate a more selective approach, prioritising undervalued high-growth stocks and/or companies with potential dividend upsides,” said RHB in a note on Tuesday.

RHB’s top picks within the sector are Bursa Malaysia Bhd (KL:BURSA), with a target price (TP) of RM11.25, and AEON Credit Service (M) Bhd (KL:AEONCR), with a TP of RM8.80.

Meanwhile, the bank noted that results for the quarter ended June 30, 2024 were largely in line with expectations.

Bursa’s strong performance in the first half ended June 30, 2024, with a net profit of RM155.5 million, aligned with RHB’s expectations. The stock is poised to benefit from a strong initial public offering pipeline and domestic trading liquidity, driven by the Fed’s expected rate cuts.

“While no confirmation has been provided by the management, we also note that Bursa has a track record of paying out special dividends in years of record-high securities' average daily trading value, and it is currently holding on to cash in excess of optimal levels,” RHB added.

Meanwhile, AEON Credit is favoured for its undemanding valuation and multiple growth engines, including its digital banking platform.

RHB also flagged underwriting margins for insurers, which had dipped by around three percentage points due to elevated claims and acquisition costs.

Even so, investment returns improved significantly, with a year-on-year increase of over 30% due to marked-to-market (MTM) gains, it added.

RHB prefers Syarikat Takaful Malaysia Keluarga Bhd (KL:TAKAFUL) over Allianz Malaysia Bhd (KL:ALLIANZ) for its smaller portion of participating contracts, allowing it to retain a bigger portion of its investment returns, and its laggard status and undemanding valuation.

The bank believes this trend could continue, particularly as global rate cuts are expected to boost MTM gains further. Nonetheless, the introduction of mandatory co-payment options is not seen as having a meaningful impact in the near term.

Meanwhile, on non-bank lenders, AEON Credit's results aligned with expectations, while RCE Capital Bhd (KL:RCECAP) and ELK-Desa Resources Bhd (KL:ELKDESA) fell short of forecasts due to slower disbursements and higher credit costs respectively.

Year to date, the share price of AEON Credit has risen by RM1.73 or 30.95% to RM7.32, while ELK-Desa declined four sen or 3.20% to RM1.21. Meanwhile, RCE Capital was down by RM1.37 or 44.77% to RM1.69.

Moving forward, key drivers of the sector include high-growth potential of specific stocks and possible dividend upsides, RHB added.