CBCP could be politically viable because, unlike GST, it directly links a 2% consumption contribution to a flat-rate benefit of RM700 for senior citizens

This article first appeared in Forum, The Edge Malaysia Weekly on September 9, 2024 - September 15, 2024

The “sandwich generation” refers to individuals who simultaneously care for their ageing parents while supporting their own children. This demographic trend is becoming increasingly prevalent in Malaysia because of the ageing population, rising life expectancy and strong cultural expectations that children will care for their elderly parents. As the proportion of senior citizens grows, the responsibilities of the sandwich generation will intensify, placing substantial economic and emotional pressure on working adults.

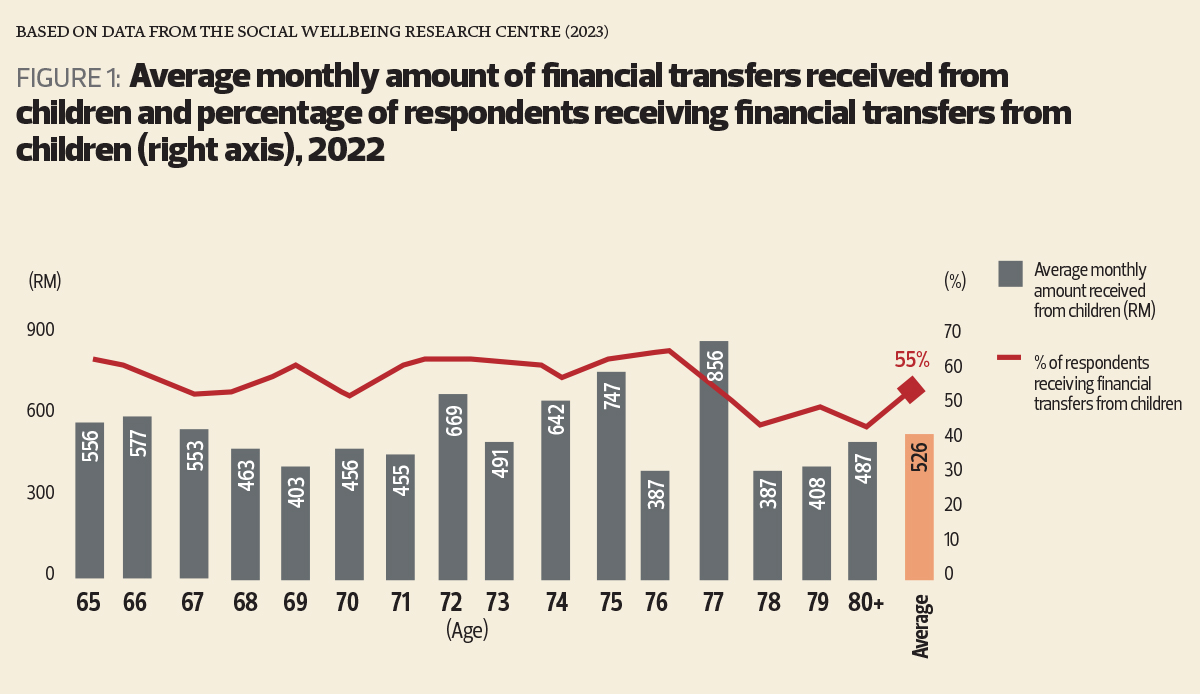

Malaysia’s healthcare and social security systems have proved inadequate in providing comprehensive support for the elderly. As a result, many elderly Malaysians rely heavily on financial assistance from their children. According to the Malaysia Ageing and Retirement Survey (MARS) by the Social Wellbeing Research Centre (SWRC) at Universiti Malaya, more than half of the elderly respondents (55%) depend on financial transfers from their children, averaging RM526 a month (see Figure 1).

This dependency highlights the inadequacies of old-age income arrangements such as the Employees Provident Fund, which often fall short in covering basic living expenses and medical costs for older adults. The MARS data shows that only 5.1% of senior citizens have EPF savings to last beyond the age of 65, exacerbating the financial burden on their children.

The dual role of supporting both ageing parents and dependent children places significant financial strain on the sandwich generation. Balancing the costs of their children’s education with the medical and living expenses of their elderly parents is a daunting challenge. MARS data shows that in 2022, individuals aged 40 to 50 allocated an average of RM234 to their parents, representing 7.4% of the average monthly income for the same year. This burden is further compounded by the rising cost of living in Malaysia. The past decade has seen significant increases in the cost of essential goods and services (cumulative increase of 30.8% since 2010), forcing many middle-aged individuals to prioritise the needs of their immediate family over long-term savings and investments. For instance, the national housing affordability index indicates that housing prices are beyond the reach of the average Malaysian household, with a median multiple of 4.7 times the median annual household income, exceeding the internationally accepted affordability threshold of 3.0 times. This situation forces many sandwich-generation families to allocate a substantial portion of their income to housing expenses, further reducing their capacity to support both their children and ageing parents.

Demographic and labour market challenges

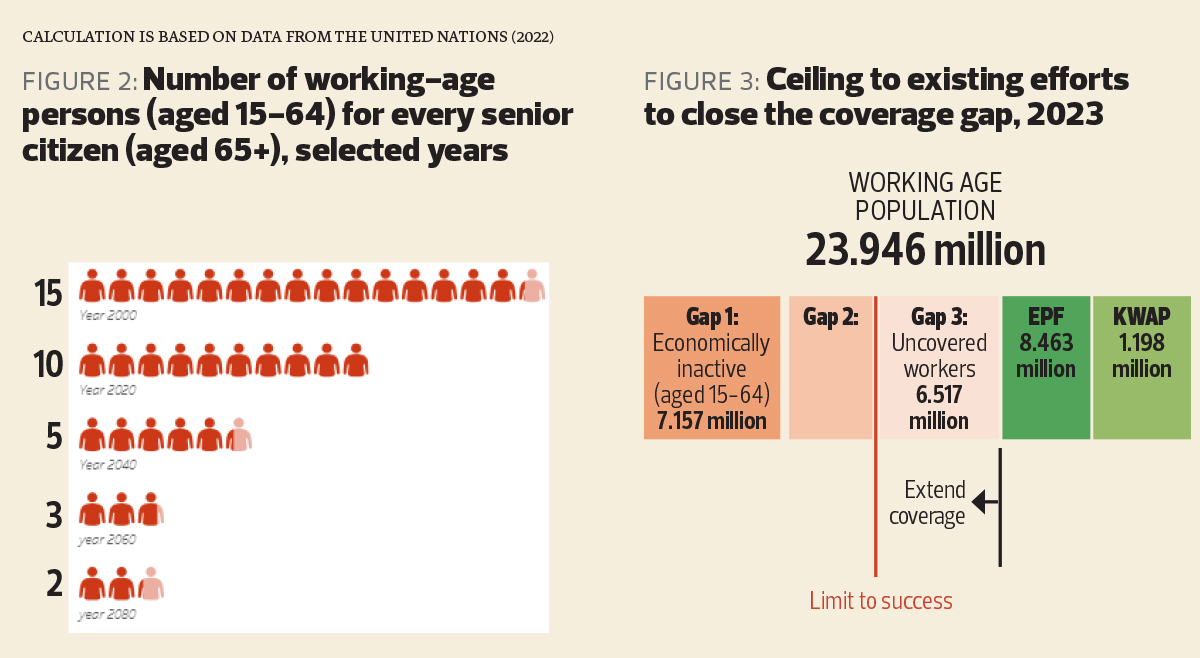

Malaysia’s demographic landscape is undergoing profound changes, with significant implications for economic development, social security and healthcare. The number of working-age persons to support one senior citizen has declined from 15:1 in 2000 to 10:1 in 2020, and is projected to decrease further to 3:1 by 2060 (see Figure 2). This shift places immense pressure on working-age adults to support senior citizens, especially in the absence of comprehensive public income security for seniors.

The Malaysian labour market also faces challenges that exacerbate the pressures on the sandwich generation. One of the most significant issues is the high incidence of low pay, defined as the percentage of the workforce earning less than two-thirds of the median wage. In Malaysia, over 30% of the workforce falls into this category, more than double the Organisation for Economic Co-operation and Development’s 14% low-pay incidence rate. This low-wage structure is coupled with wage disparities along geographical, educational and skill lines. Added to this, the female labour force participation rate, at 55.8% in 2022, is significantly lower than the male participation rate of 81.9%. These disparities contribute to inadequate old-age protection, particularly for vulnerable groups such as women, self-employed workers and low-wage earners.

System gaps and old-age poverty

Malaysia’s reliance on an insurance model based on labour market participation and income level, with limited government intervention, results in lower coverage rates and inadequate benefits for most Malaysians. This situation places significant pressure on the sandwich generation to provide for their ageing parents.

In 2023, 13.735 million working-age individuals, or 57.36% of the population, were not covered by either EPF or Retirement Fund (Inc) (KWAP). These coverage gaps leave many individuals vulnerable to old-age poverty, disproportionately affecting senior citizens.

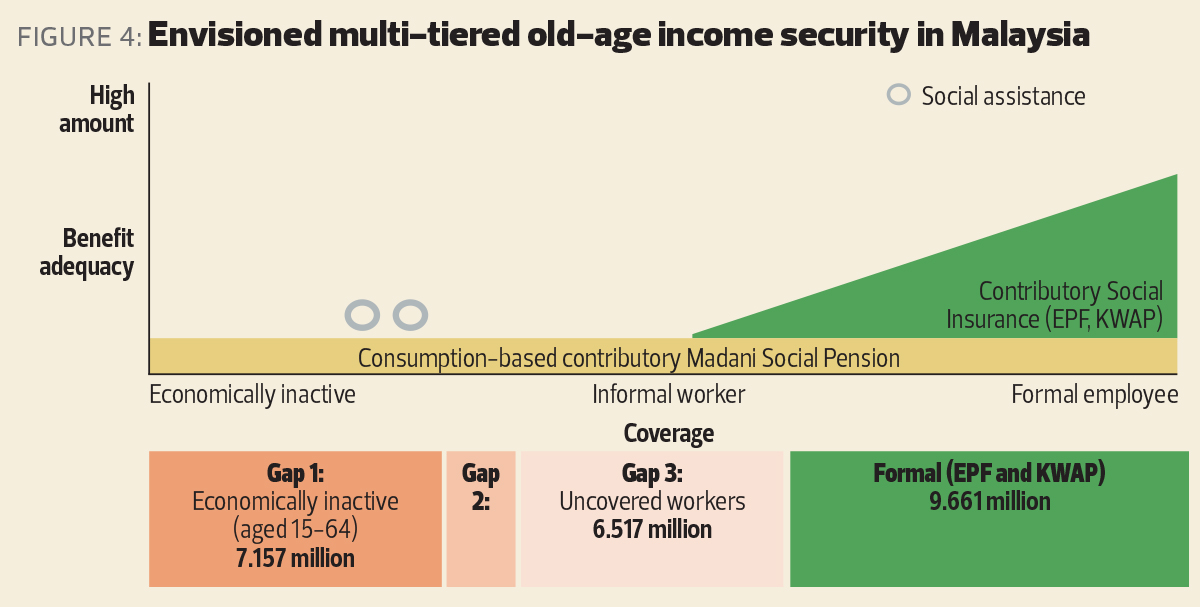

Closing the coverage gap, therefore, is essential to alleviating the financial strain on the sandwich generation. Effective policy formulation requires a detailed examination of the various segments within the working-age population, acknowledging the specific factors contributing to each gap. For example, EPF’s initiatives, such as i-Saraan, aim to extend coverage to the informal sector and gig economy (addressing gap 3 in Figure 3) but fall short in addressing gap 2 (unemployed individuals) and gap 1 (those not in the labour market, particularly women with family responsibilities). These groups risk reaching retirement age without sufficient accumulated savings for old-age income security, leaving them vulnerable to poverty in their senior years and dependent on their children for support. Addressing these gaps comprehensively is crucial for ensuring equitable old-age security across all segments of society.

Pension adequacy is another significant weakness in Malaysia’s current system. EPF statistics show that more than one-third of contributors withdraw their retirement savings as a lump sum at retirement, currently set at age 55. However, the median savings amount at age 54 is only RM44,025, equivalent to just nine months of per capita income as at 2023. This median savings obscures the fact that female members have a median savings of only RM29,975 compared to RM63,351 for male members, highlighting the compounded financial vulnerability faced by women in retirement.

The case for a consumption-based contributory pension

Given the pressing challenges faced by the sandwich generation, the introduction of a consumption-based contributory pension (CBCP) offers a sustainable and equitable solution. Unlike traditional pension schemes that rely on direct payments from labour income, CBCP introduces a 2% contribution linked directly to consumption, harnessing the economic activity of all residents, regardless of employment status. By extending coverage to all senior citizens, including those without employment records, CBCP would particularly benefit women and individuals in unstable forms of employment who are currently excluded from old-age income security.

CBCP offers a distinct advantage by directly linking contributions to a tangible social benefit — a flat-rate pension of RM700 a month for senior citizens. This direct connection could make CBCP more palatable to the public, positioning it as a progressive policy that not only addresses old-age income security but also alleviates the financial pressures on the sandwich generation.

Integrating CBCP into Malaysia’s pension system

Integrating a flat CBCP as a foundational pillar within Malaysia’s pension system would provide a vital complement to existing earnings-related tiers, such as EPF (see Figure 4). This strategic approach would significantly broaden the pension system’s reach, encompassing informal and self-employed workers who are often left out of traditional pension schemes, as well as individuals outside the labour force. By ensuring that all senior citizens, regardless of their labour force participation, have access to a guaranteed minimum level of income security, this integration would create a more inclusive and equitable pension framework, addressing critical gaps and enhancing overall social protection.

By coordinating CBCP with existing old-age income security measures and emphasising synergies, the integrated system can effectively reduce inequality and enhance economic security for the elderly population. This approach also maintains incentives for saving in higher level protection, such as EPF and private sector saving, and labour market participation within Malaysia’s overall fiscal framework.

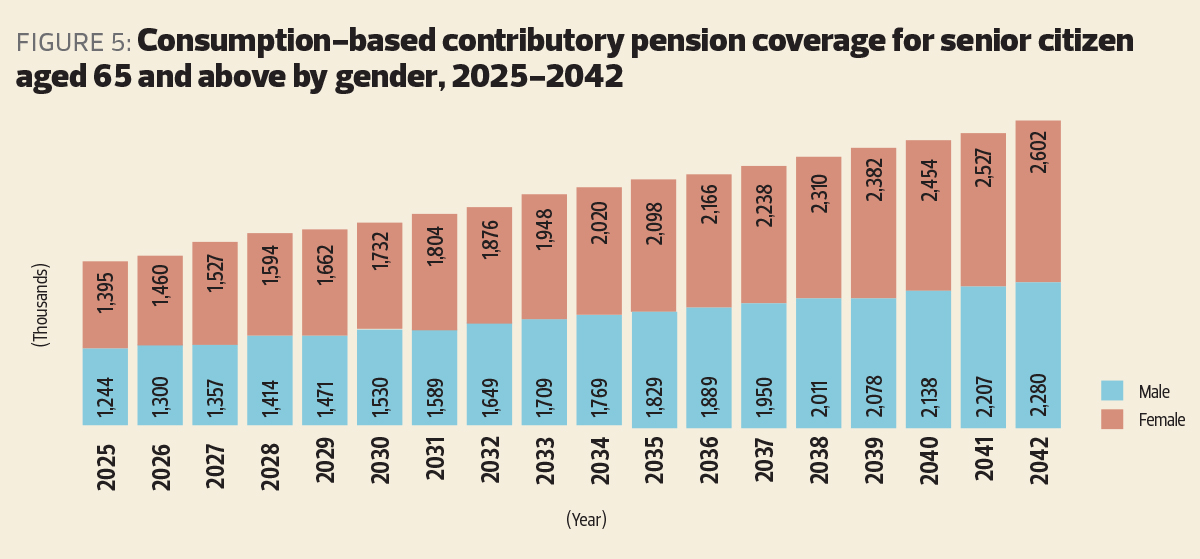

The proposed CBCP, providing RM700 per month to senior citizens aged 65 and above, would correct the discriminatory labour market, benefiting women more than men, as they tend to live longer (see Figure 5).

The overall cost of CBCP is projected to range from 1.019% to 1.063% of gross domestic product by 2045, with a 2% consumption-based contribution generating sufficient revenue (1.08% of GDP annually) to cover these costs.

CBCP is technically sound and politically feasible

Social pensions have significantly reduced old-age poverty and influenced political outcomes in various countries, often benefiting ruling parties electorally. However, implementing a consumption-based contribution in Malaysia faces political challenges, particularly because of past negative experience with consumption-based taxes such as the Goods and Services Tax. Introduced in 2015, GST was unpopular for its regressive impact, leading to its repeal in 2018.

Despite these concerns, CBCP could be politically viable because, unlike GST, it directly links a 2% consumption contribution to a flat-rate benefit of RM700 for senior citizens. This connection between contributions and social benefits may make CBCP more acceptable to the public, as it supports the elderly, especially those financially dependent on their children.

To further ease CBCP’s implementation, we suggest reducing workers’ EPF contributions by 2%, which would lead to an increase in real wage and offset the impact of the new contribution.

Evidence from other countries shows that well-designed social pensions can garner significant public support and become a political asset for governments. For example, the universal old-age pension introduced in Lesotho in 2004 helped the government win subsequent elections, while Peru’s “Pensión 65” programme, launched in 2011, significantly boosted electoral success. Similar evidence was seen in Georgia, Kenya, Bolivia, Brazil and Mauritius. These examples demonstrate the strong appeal of social pensions to the electorate, particularly the sandwich generation.

The introduction of CBCP in Malaysia offers a viable solution to the financial and emotional pressures faced by the sandwich generation. By extending coverage to all senior citizens, particularly those excluded from traditional pension schemes, CBCP would alleviate the burden on working adults while providing a more inclusive and sustainable social protection system. CBCP represents a forward-thinking policy that addresses the challenges of an ageing population and strengthens the fabric of Malaysian society.

Dr Amjad Rabi is a visiting expert at Universiti Malaya’s Social Wellbeing Research Centre. Emeritus Prof Datuk Norma Mansor is the director of SWRC.

Save by subscribing to us for your print and/or digital copy.

P/S: The Edge is also available on Apple's App Store and Android's Google Play.

- Trump says Ukraine talks may be going OK, but there is a time 'to put up or shut up'

- Iran, US hold 'positive' talks in Oman, agree to resume next week

- Central banks prepare first G-7 responses to US chaos

- Apple, Nvidia score relief from US tariffs with exemptions

- Apple was on brink of crisis before tariff concession from Trump