This article first appeared in The Edge Malaysia Weekly on June 17, 2024 - June 23, 2024

CYL Corp Bhd (KL:CYL), a long-standing player in the plastic packaging industry, is embarking on a strategic diversification plan as it ventures into property development amid the challenging operating environment for plastic packaging manufacturers.

“Recognising the current demand for industrial property, especially in this area, we decided to utilise this land for a semi-detached factory project catering to industrial businesses,” CYL executive director Chen Teck Shin tells The Edge.

Chen is referring to a 1.28-acre plot — adjacent to the company’s factory in Shah Alam — that was originally acquired in 2001 for “potential capacity expansion”.

To address margin erosion caused by rising resin costs, labour expenses and electricity tariffs, CYL announced in late May that it was diversifying its business portfolio.

Founded in 1980, the company is a key supplier of bottled plastics for various sectors, including automotive lubricants, toiletries, pharmaceuticals and dairy products, through its subsidiary Perusahaan Jaya Plastik (M) Sdn Bhd (PJP).

But after more than four decades, it has decided that conditions necessitate a diversification into property development. “The plastic industry is very saturated, especially in the consumer space. For the business to grow, we need the volume, and that is tied to population growth,” says Chen.

Pending a pick-up in business, CYL proposes to put its idle land to better use. “We believe it offers a more strategic value creation opportunity compared to simply disposing of the land,” Chen says. The plot has been earmarked for semi-detached factories that cater to medium and light industrial businesses.

The project, with an estimated gross development value (GDV) of RM38 million, will be financed by internally generated funds and bank borrowings.

“The proposed development is strategically located in a mature industrial area, where the immediate developments are generally made up of industrial properties consisting of terraced factories, semi-detached factories and detached factories. If all goes as planned, we estimate the project to be completed in the fourth quarter of 2026 and to contribute about RM10.5 million in earnings,” he says.

Construction is expected to start by the end of this year pending approval from the authorities. Chen says the company is already on the lookout for more land for industrial property development.

Still very much a family-controlled company, the Chens collectively own about 57% of CYL, which was founded by Chen’s father, Chen Yat Lee, from whom the initials of the company were derived.

The 83-year-old patriarch is the company’s managing director and largest shareholder with a 33.97% stake. Chen, 45, holds 19.67% and his sister Chen Wai Ling, who is also an executive director, has 3%.

Chen started his career in tax services with Deloitte before joining CYL in 2004. He was appointed an executive director in 2017.

Challenging operating environment in plastic industry

For the financial year ended Jan 31, 2024 (FY2024), CYL’s net loss widened to RM1.53 million, from RM139,000 a year earlier, on the back of a 4.3% decrease in revenue to RM42.89 million from RM44.77 million previously. The group attributed it to an increase in labour costs and higher utility tariffs during the year in review.

Conditions are expected to remain challenging given the volatility in global resin prices, rising labour costs and impending subsidy rationalisation.

“When the war between Ukraine and Russia started in February 2022, we saw resin prices spike to their highest in 40 years. Although resin prices have stabilised, it is a challenge for our operation to cope with the fluctuation in resin prices,” says Chen.

“We can pass the cost on to clients, but there is a time difference between when we buy the raw materials and when we secure the contracts,” he explains but declines to elaborate on the cost structure.

Having said that, Chen says CYL is seeing improvement in its sales, driven by the growing economy and improving consumer sentiment. Its manufacturing plant is able to produce between 4,000 and 4,500 tonnes of plastic packaging and is currently running at a utilisation rate of 70%.

“There is more room for us to increase our sales. But we also need to look for ways to improve our margins, including venturing into property development, as well as managing our costs through factory automation,” he says.

Previously a takeover target?

Previously, CYL’s clean balance sheet made it an attractive takeover target, according to a corporate observer. “The company’s clean balance sheet attracted a lot of suitors in the past. However, the founder wants to pass the company to the next generation,” the observer says of CYL, which has no debt and is currently sitting on RM7.29 million cash (as at Jan 31).

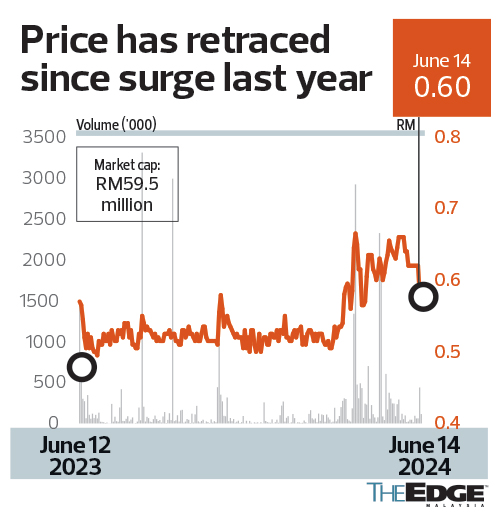

In January last year, CYL’s share price surged as high as RM1.18, even though it had slipped into the red. Market observers attributed the interest to a potential buyout, although Chen denies there was such an approach.

“I’m not aware. As of now, the company is working on new opportunities in property development. We are also looking for ways to expand the sales of our core business,” he says.

“So far, we don’t see any alternative in the plastic packaging sector. As such, the core business is still viable and we expect more demand moving forward.”

CYL’s share price had since retraced to 60 sen last Friday, giving the company a market capitalisation of RM59.5 million. The shares are highly illiquid as 57% of the company is held by the Chen family, with the free float at 21%. Year to date, the average daily trading volume stands at 204,000 shares.

Save by subscribing to us for your print and/or digital copy.

P/S: The Edge is also available on Apple's App Store and Android's Google Play.