CGS International cuts Inari-Amertron earnings forecast on weak smartphone demand

KUALA LUMPUR (April 25): CGS International has cut its earnings estimate for Inari Amertron Bhd as recent data flagged weakened smartphone demand, according to its research note on Thursday.

The research house lowered its FY2024-FY2026 earnings per share by 3% to 9% as it believes lower smartphone shipment could impact Inari's radio frequency (RF) segment.

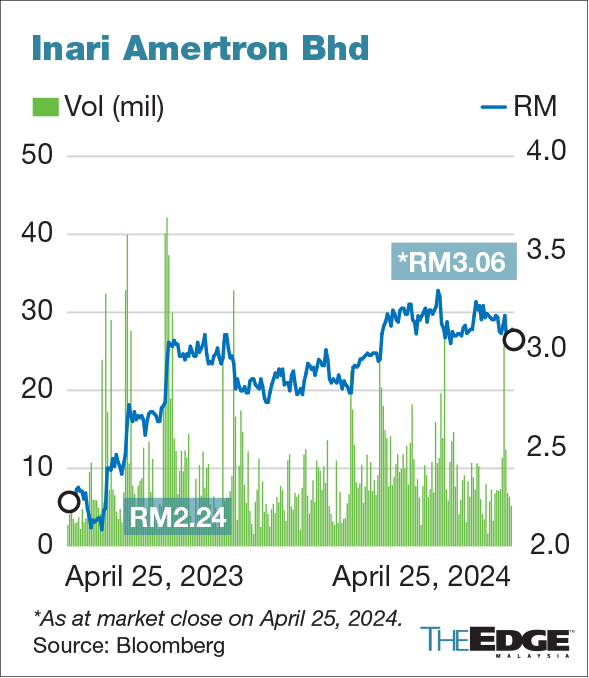

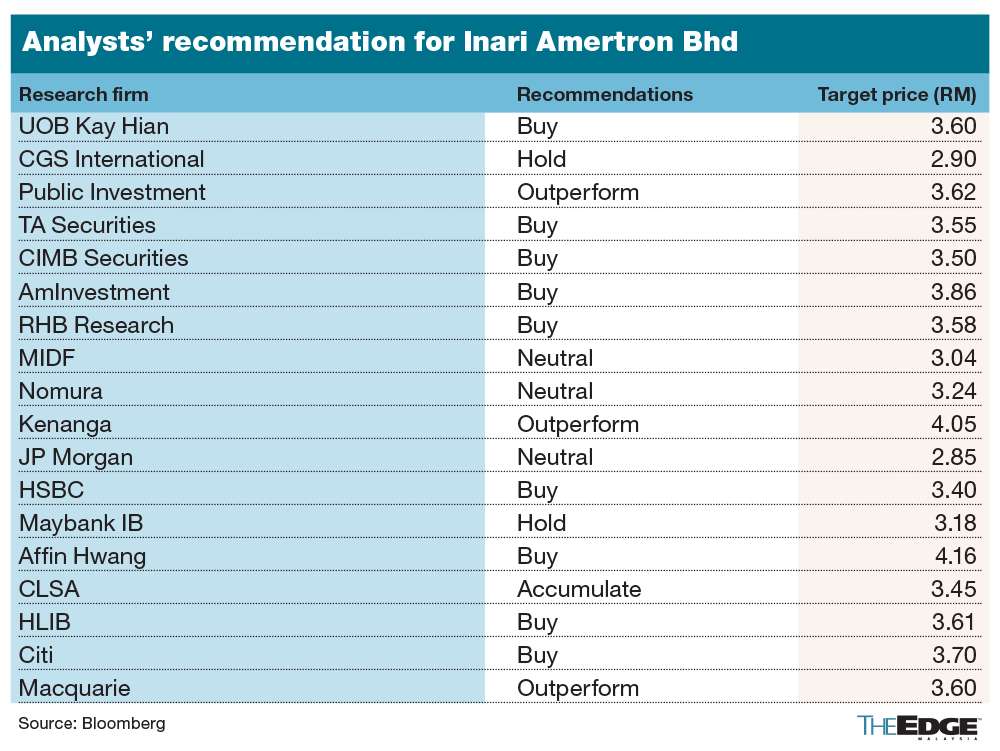

The firm reiterated its "hold" call on Inari with a higher target price of RM2.90, saying that at 28.8 times FY2025F price-to-earnings ratio, the stock looks fairly valued.

It cited International Data Corporation's (IDC) data that showed decelerated smartphone shipment, especially US-branded devices, which fell by 9.6% year-on-year in the March 2024 quarter.

“The mid-2023 introduction of Huawei 5G handsets [has] slowly chipped away [at] the market share of US branded smartphones.

“In our view, this could impact Inari’s RF testing utilisation rate through lower volume loading, partially negating higher service charge per unit due to higher RF content.

CGS also tweaked Inari's earnings before interest, taxes, depreciation, and amortisation margin lower, given the ramp-up of new businesses that carry lower margins vis-à-vis its core businesses.

The house said the group’s other segments should perform relatively better, partially cushioning the near-term RF softness.

Citing key network component supplier Coherent, CGS said 800G components, including switches and transceivers would see a strong ramp-up from 2024 onwards, in line with AI demand growth.

“We understand that Inari’s backend processes for 400G optical transceivers are moving to high-volume manufacturing (HVM), while 800G transceivers recently qualified for low-volume manufacturing for a major global server player.

“This aligns with the group’s expansion plan of its new CK3 plant in the Philippines, which will add circa 230,000 sq ft of floor space by endCY24F,” it said.

Meanwhile, it said the automotive segment should see some stabilisation in the coming months as the group undergoes various stages of qualification for its auto-related sensors and optocouplers.

Its memory business is also ramping up, with the four-stack die moving into HVM with additional production lines by 4QFY2024F, opening an opportunity for new project wins for eight- and 12-stack memory die.

Overall, it expects Inari's non-RF segment revenue to grow marginally by 3% in FY2024F, with strong ramp-up seen by FY2025, together with the ramp-up of its 54%-owned Yiwu Semiconductor in China, as it obtains more qualification for packaging projects.

“The foray into these new growth areas could be margin dilutive in the near term as they go through gestation periods, in our view,” CGS warned.

- FMM: Delay proposed 30% port tariff hikes

- MH370: 11 years on, is closure finally within reach?

- Petros wants strategic partnership with Petronas, says Fadillah

- Police probe video of former MP allegedly defaming PM, home minister

- Gobind: Malaysia needs to develop homegrown AI champions within semiconductor industry

- Trump team is pivoting to no pain, no gain as economic message

- MM2H programme open to applicants from any country, not just Chinese nationals — Tiong

- DBS digital banking, ATM services are disrupted for hours

- ECB’s Schnabel signals inflation concern in rate debate salvo

- Charting the global economy: US tariff launch proves messy; ECB cuts rates