KUALA LUMPUR (April 25): Members of the Employees Provident Fund (EPF) who are below 55 years old will have an Account 3 starting from May 11, from which they can make withdrawals at any time for any purpose — subject to a minimum withdrawal amount of RM50. This is on top of the two existing accounts they currently have for retirement savings.

Hence, members’ contributions will be divided in the portions of 75:15:10 into Account 1 (Retirement Account), Account 2 (Sejahtera Account) and Account 3 (Flexible Account) respectively, according to EPF’s statement issued on Thursday.

EPF members’ monthly contributions are currently split in the ratio of 70:30 into Account 1 and Account 2.

The balances in Account 1 and Account 2 will remain, while Account 3 will start with a zero balance.

For members above the age of 55, all savings in those three accounts will be merged into “Akaun 55”, while new contributions from this age group members will be credited into “Akaun Emas”.

Account 3 will start with new contributions that will be credited into the member's account after the implementation date.

"If the member chooses to opt-in with an initial amount, the transfer of the initial amount to Account 3 and other accounts [if applicable] is based on the balance in the member's Account 2 on the date the opt-in application is made," the EPF said.

The transfer method will be according to this breakdown (also see chart):

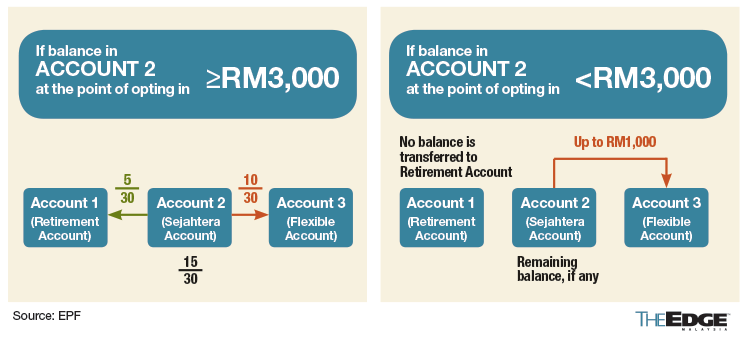

a) If the balance in Account 2 is RM3,000 and above

A third or 10/30 of the balance in Account Sejahtera (Account 2) will be transferred to Account 3, while 5/30 of the balance in Account 2 will be transferred to Account 1; the balance 15/30 will be retained in Account 2.

b) If the balance in Account 2 is less than RM3,000

Account 2 with a balance of RM1,000 or less will have the full balance transferred to Account 3, while those with a balance of more than RM1,000 but less than RM3,000 will have RM1,000 transferred to Account 3; no transfers will be made to Account 1.

Members can choose for the opt-in, which is non-cancellable, from May 11 till Aug 31

“Members can only choose to opt-in for the transfer of the initial amount to the Flexible Account (Account 3) one time, starting from the effective date (May 11) until Aug 31, 2024, after which the opt-in cannot be cancelled,” EPF said.

Members who wish to take advantage of this opt-in can submit their application through the KWSP (EPF) i-Akaun application, or the self-service terminals at any EPF branches nationwide.

Applications for the opt-in and withdrawals can be made online through the KWSP i-Akaun, or at any EPF branch nationwide.

EPF also encouraged members who have yet to register with KWSP i-Akaun to do so, in order for withdrawal transactions from Account 3 to be made.

“The main focus of the EPF account restructuring initiative is to empower members in making decisions to balance future needs for retirement between short-, medium- and long-term financial needs.

“This initiative will also help increase members’ retirement savings, so that they will have sufficient retirement income to sustain their needs after retirement,” EPF chief executive officer Ahmad Zulqarnain Onn said.

Economists foresee minimal impact on EPF's investment strategy and dividend performance

The Account 3 is unlikely to affect the EPF's investment strategy and dividend performance, according to economists.

This is due to the relatively modest withdrawal amount of RM25 billion in the first-year post-rollout, as per EPF forecasts, which is significantly lower than the total withdrawals during the pandemic, amounting to RM145 billion.

"Even during the pandemic, the dividend payout for conventional and shariah savings hovered around 5% to 6%. I believe that EPF can sustain its solid performance following the introduction of Account 3," the executive director of the Socio-Economic Research Centre Lee Heng Guie told The Edge.

Lee also does not foresee any compromise to contributors' retirement income adequacy from the rollout of Account 3, as the account will commence with a zero balance, with contributors having a one-time option to transfer part of their savings from their Account 2 to Account 3.

"In fact, the government has raised the contribution proportion to the Retirement Account [Account 1] to 75%, which may offer additional security to contributors' retirement savings and the EPF's investment strategy," he said.

Furthermore, Lee predicts that the flexibility of withdrawing funds from Account 3 may boost spending power, thereby positively impacting economic growth.

However, he advises members to exercise responsibility when withdrawing funds from EPF accounts to ensure sufficient retirement savings.

Meanwhile, Mohd Afzanizam Abdul Rashid, the chief economist of Bank Muamalat Malaysia Bhd, describes Account 3 as a "delicate balancing act" between meeting retirement savings adequacy and ensuring EPF members' economic well-being.

"While the government must ensure adequate retirement savings, it cannot overlook issues such as the cost of living, slow wage growth, and the prevalence of gig employment, which have significantly impacted Malaysians' livelihoods," he said.

He also agrees that this measure will, to some extent, bolster purchasing power, thereby making the government's expectation of achieving a gross domestic product (GDP) growth rate of 4% to 5% achievable.

Members can fully access the system on May 12. Members can visit any EPF branch nationwide, or refer to the EPF official website at www.kwsp.gov.my, or access the KWSP i-Akaun for more information.

To receive CEO Morning Brief please click here.

Read also:

Tomei books 76% net profit in 1Q, highest since 2QFY2022

Tomei anticipates retail boost from new EPF Account 3