This article first appeared in The Edge Malaysia Weekly on April 1, 2024 - April 7, 2024

DXN Holdings Bhd’s share price is down 10.7% since relisting last year at an IPO price of 70 sen — an underperformance that the group attributes to investors’ insufficient knowledge of its business operations.

Indeed, founder and non-independent executive chairman Datuk Lim Siow Jin acknowledges there has been scepticism over DXN’s sales performance in overseas markets such as Latin America.

Despite these challenges, the health and wellness-oriented direct selling firm is looking to prove its strength by charting annual sales growth of at least 15% to 20%. DXN is confident that the target can be easily surpassed by expansion into new markets, starting this year with Brazil and Egypt.

Latin America is the group’s key market, contributing more than half of group revenue, while about 14% comes from the Middle East and North Africa.

“We have high hopes for Brazil, which is very similar to Peru and Bolivia. The per capita sales in Peru and Bolivia are very encouraging. In Latin America, we don’t have a presence in many countries, such as Chile and Uruguay. So, we still have a good expansion outlook there,” Lim tells The Edge at the group’s new marketing headquarters in Cyberjaya, Selangor.

Having said that, he notes that a new market typically takes two to three years to mature.

DXN also plans to build new factories in Morocco and Peru this year at a total land cost of RM49 million. The set-up cost, which has yet to be finalised, is typically more than RM100 million for a plant, based on the company’s track record.

Lim believes DXN has a unique proposition in the multi-level marketing (MLM) market, despite facing rising costs from logistics and inflationary pressures in the past two years. “We are not a pure MLM company, we are a manufacturer. More than 90% of DXN products are manufactured in-house. Because of this, we are able to get a net profit margin of 15% to 20% compared with our peers’ 5% to 10%.”

In addition, he says the company is focused on the online concept, operating a smaller number of branches or growing by organic expansion — through people and not branches. Another strength is that DXN has a buffer stock of five to six months to handle supply disruptions, he adds.

During the pandemic, more people were willing to participate in MLM to increase their income base, Lim observes. “We did well during the [Movement Control Order] period, with about 20% growth.”

DXN’s product offerings include health and dietary supplements, food and beverages, and personal care and cosmetics. The raw materials for its products include ganoderma, spirulina, cordyceps and tiger milk mushroom.

Of its 17 million members worldwide, 5.2 million are active ones — defined as those who have bought products in the last two years.

Founded in 1993 by Lim, DXN was first listed on the local bourse in September 2003 but taken private in December 2011 to streamline the corporate management.

At the time, investors were confused about DXN’s many non-core businesses, such as property development and plantations, which led to the delisting of the group, says Lim.

After more than a decade, the company made a comeback on Bursa Malaysia in May 2023, raising more than RM120 million from its IPO. This time around, DXN put up only its health and wellness business — a strategy that Lim says will continue as the group believes in being asset-light and having enough cash to address any shocks. That explains its net cash position over the years.

“Every company should have some kind of contingency funding. Along with the stock buffer, we have more than RM1.2 billion in hand,” he adds. At end-November 2023, it had RM228.3 million in net cash flow and total borrowings of RM183.3 million.

DXN has a dividend policy of distributing at least 55% of its net profit to its shareholders. It paid a dividend of 2.6 sen per share for the first nine months of the financial year ended Feb 29, 2024 (9MFY2024), representing a dividend yield of 4%.

Trading at a 12-month forward price-earnings ratio (PER) of nine times, DXN’s share price had slipped 2.3% year to date to close at 62.5 sen last Wednesday, for a market capitalisation of RM3.1 billion.

Its peers Amway Malaysia Holdings Bhd and Beshom Holdings Bhd are trading at 12-month forward PERs of 10.9 times and 22 times respectively.

While the share price movement has not been encouraging, Lim, who holds a 68.27% stake in DXN through LSJ Global Sdn Bhd, says the group is not keen on aggressive share buybacks.

“My shareholding is very high, already close to 70%, and it may trigger a GO [general offer]. The share price is about market sentiment, and it also suggests that the market does not understand us and our potential,” he observes, seemingly unfazed.

Between Feb 22 and 28 this year, DXN bought back 10.78 million shares for RM6.83 million. The shares were transacted at 63 to 64 sen apiece. Gano Global Supplements Pte Ltd is the second-largest shareholder of DXN, with 13.31% equity interest.

Bloomberg data shows that all four analysts covering DXN have “buy” calls, with a consensus target price of 91 sen, suggesting an upside potential of 45.6%.

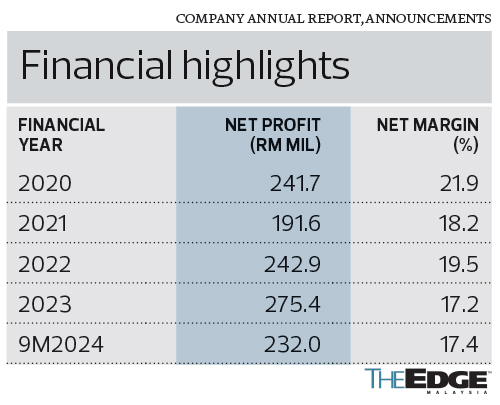

For 9MFY2024, DXN’s net profit expanded 5.3% year on year to RM231.98 million from RM220.23 million, underpinned by sales growth in Latin America and India. Revenue for the period in review was up 11.4% y-o-y to RM1.33 billion from RM1.2 billion.

In FY2023, its net earnings grew 13.4% y-o-y to RM275.4 million, from RM242.92 million, on the back of a 28.8% rise in revenue to RM1.6 billion, from RM1.24 billion.

DXN ventured into Latin America in 2005 when it spread its wings to Mexico. This was followed by its expansion into Peru and Bolivia in 2010 and 2012 respectively.

“You should not have some kind of pre-judgement of a certain market. Nobody imagined Morocco would become a major market. So hopefully, North Africa will follow suit,” says Lim.

DXN has 13 manufacturing facilities across Malaysia, India, China, Mexico, Indonesia and the United Arab Emirates (UAE), with a total built-up area of 477,300 sq m.

Over the past three years, the group has spent more than RM400 million to fund its expansion, which includes the construction of manufacturing facilities in India and China and the purchase of plants and machinery in Malaysia, the UAE, India and China, among others. The group is now developing its ready-to-eat and ready-to-drink segments.

Save by subscribing to us for your print and/or digital copy.

P/S: The Edge is also available on Apple's App Store and Android's Google Play.