This article first appeared in Capital, The Edge Malaysia Weekly on March 18, 2024 - March 24, 2024

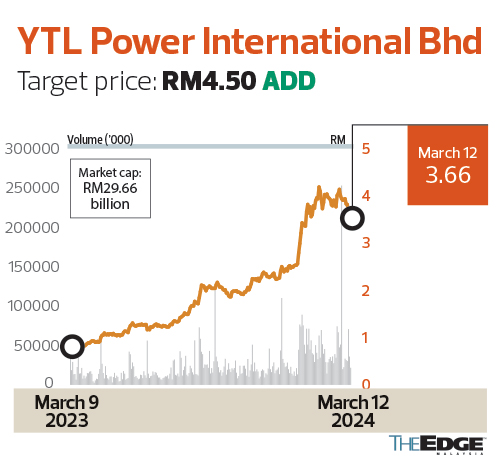

YTL Power International Bhd

Target price: RM4.50 ADD

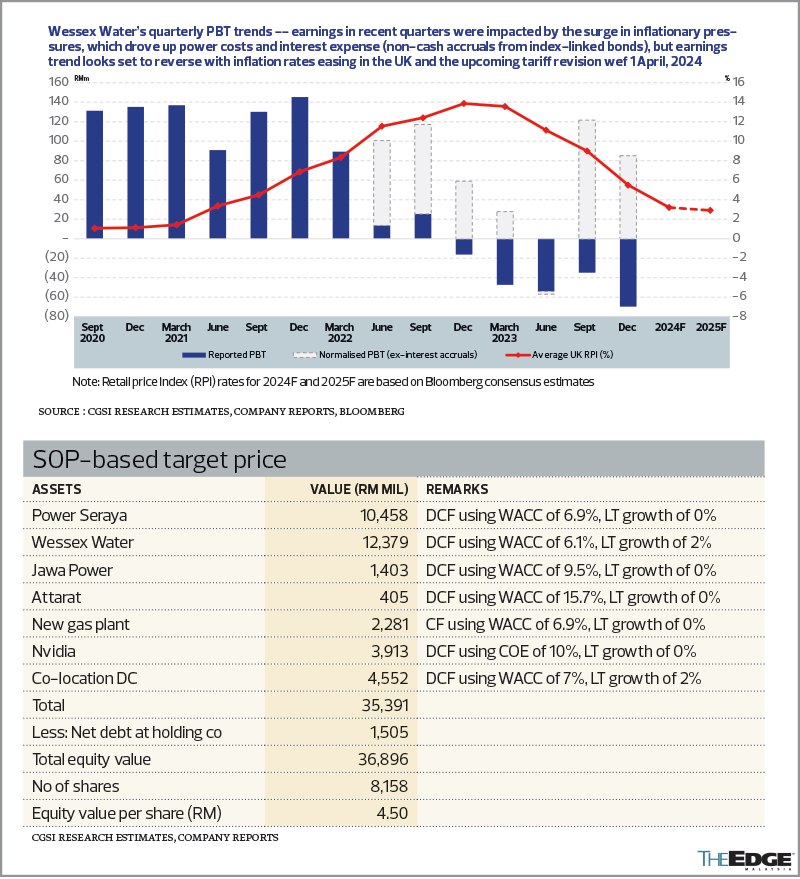

CGS INTERNATIONAL research (MARCH 8): Starting from April 1, 2024, YTL Power International Bhd’s (YTLP) subsidiary Wessex Water (WW) will impose an increase of at least 11% on water bills for its customers as part of its allowed annual water tariff adjustments. This adjustment surpasses the previous year’s November inflation rate, a typical benchmark for annual tariff setting, which stood at 4.2%. WW explained in its announcement that it deliberately kept tariff increases lower than anticipated during last year’s review to alleviate the immediate financial strain on its customers amid the cost-of-living crisis in the UK. Consequently, this year’s adjustment serves, in part, as a recovery for the under-collection between April 2023 and March 2024. We estimate the tariff revision translates into an increase of at least RM95 million in quarterly revenue for WW, all else remaining equal. This, in our view, should translate into improved earnings for WW and could pave the way for its return to profitability by as early as 3QFY24F.

Phase 1 of YTLP’s colocation data centre (DC) is progressing well, with the co-locator expected to complete fit-out works for 8MW (of the 32MW firm capacity) by end-1QCY24. In addition, Tengku Datuk Seri Zafrul Abdul Aziz, Minister of Investment, Trade and Industry, reiterated via his social media account on Feb 29 that he had had further discussions with Nvidia and YTLP on the DC investments, with Phase 1 coming through by June 2024. While finer details on the DC projects are still lacking, our initial calculations suggest that these planned DC investments can contribute as much as RM1.2 billion to RM1.4 billion in net profit to YTLP once fully ramped up in FY27F.

While the share price was up strongly over the past 12 months (+356%), we believe the potential value accretion from the DC investments have yet to be fully priced in. As such, we reiterate “add” on YTLP with an unchanged SOP-based target price of RM4.50. The current share price implies an FY24/25F PER of about nine to 10 times, on an earnings base that reflects a normalisation of PowerSeraya earnings by FY26F.

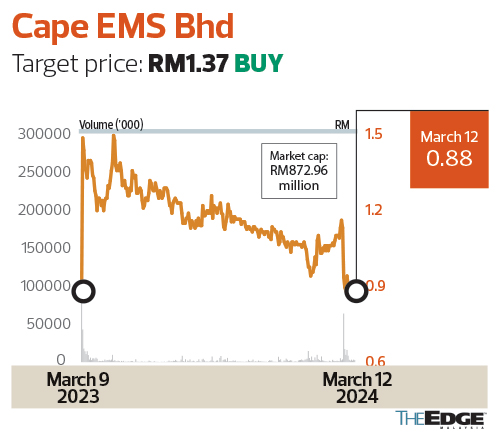

Cape EMS Bhd

Target price: RM1.37 BUY

RAKUTEN TRADE RESEARCH (MARCH 11): We anticipate Cape EMS Bhd (CEB) to report net earnings of RM68.2 million and RM85.8 million for FY24 and FY25 respectively. We have a “buy” call with a target price of RM1.37, based on a PER of 20 times (a discount to the industry’s PER of 25 times due to its smaller market cap) over FY24 EPS. The company’s financial leverage is manageable, with a net gearing of 0.4 times as at Dec 31, 2023, and an interest coverage ratio of more than seven times.

One of CEB’s customers, Mimosa Network, has successfully expanded into new markets and customer segments. This achievement reinforces Mimosa’s ongoing commitment to channelling higher orders to CEB within the wireless communication segment. We estimate that CEB is on track to fulfil our FY24 order forecast assumption, with delivery anticipated over the next six months. The acquisition of iConn Inc by CEB, set to be completed by 1QFY24, is aimed at integrating its design and engineering capabilities, especially in the electric vehicle segment. This strategic move is expected to enhance and diversify the range of services in its electronics manufacturing services segment.

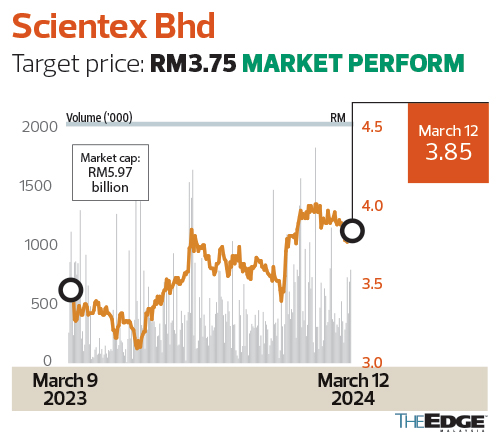

Scientex Bhd

Target price: RM3.75 MARKET PERFORM

KENANGA RESEARCH (MARCH 11): Scientex Bhd is acquiring a parcel of freehold land measuring 826 acres in Mukim Batang Berjuntai, Kuala Selangor, from Metalplex Plantation Sdn Bhd for RM335.7 million cash. The proposed acquisition is expected to be completed in 1HCY25.

It intends to build a mixed-use development on the land located between Ijok and Bestari Jaya. At RM335.7 million, the price tag translates into RM9.33 per sq ft (psf), which is a discount to the asking price of RM12 to RM13 psf for agricultural land in the surrounding areas. We believe the discount could be attributed to the location being a distance away from the Kuala Selangor town area, potentially a low land efficiency (sellable land as a percentage of total land area) owing to land use restrictions and the requirement for additional investment in basic amenities.

The acquisition will increase its net debt and net gearing from RM515 million and 0.15 times at end-October 2023 to RM851 million and 0.24 times respectively, but are still highly manageable.

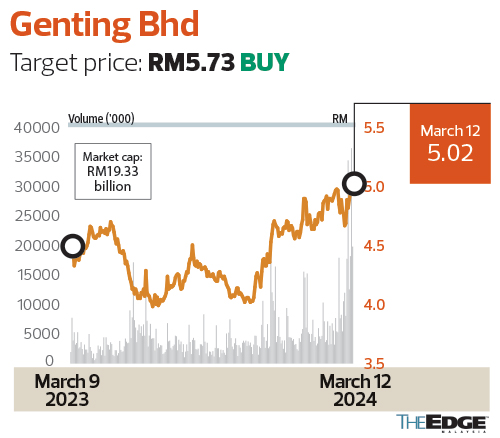

Genting Bhd

Target price: RM5.73 BUY

MAYBANK IB RESEARCH (MARCH 8): Genting Bhd’s 20%-owned TauRx Pharmaceuticals Ltd presented the full results from its Phase 3 LUCIDITY trial of Hydromethylthionine Mesylate (HMTM) that is designed to combat Alzheimer’s disease. It confirmed the positive initial results released in 2022. Under a “blue sky” scenario where HMTM is approved and TauRx is valued at US$15 billion with no discount ascribed to it, our target price for Genting could be raised to RM9.40.

Recall that the trial was actually invalidated because the placebo had benefits when it was not supposed to. Yet, TauRx proved HMTM’s efficacy with brain scans and by comparing it to the placebo data from other trials. It has initiated regulatory engagement with the UK’s Medicines and Healthcare products Regulatory Agency and the US Food and Drug Administration. The latter has an Accelerated Approval Program (AAP) to address life threatening and severely debilitating illnesses like Alzheimer’s.

“Lecanemab”, which was developed by Eisai and Biogen, was approved only in six months on Jan 6, 2023, under the AAP. We ascribe a US$1 billion valuation to TauRx. After ascribing a 60% discount to SOP, TauRx accounts for only nine sen out of our target price of RM5.73 for Genting.

Save by subscribing to us for your print and/or digital copy.

P/S: The Edge is also available on Apple's App Store and Android's Google Play.

- Is Malaysia’s chip sector prepared for the storm?

- Nationwide frenzy: Long queues at Sports Toto outlets as punters hope to win RM100m jackpot

- US trade war threatens demand for Malaysian chips, says Zafrul

- TikTok says to ‘go dark’ in US on Sunday without White House clarity

- PM's UK visit attracts potential investments worth RM11b

- Empowering community and shaping a sustainable environment

- Nationwide frenzy: Long queues at Sports Toto outlets as punters hope to win RM100m jackpot

- Malaysia calls for second LSS5 bid, target 2GW

- US FTC finalises consent order for US$53b Chevron-Hess merger

- Trump plans to intensify immigration enforcement soon after inauguration, Reuters reports