KUALA LUMPUR (Feb 22): Analysts remain optimistic about semiconductor services firm Malaysian Pacific Industries Bhd's (MPI) outlook, on the back of a strategic focus on its market operations despite the recent mixed financial performance.

Analysts anticipate MPI to thrive, underpinned by its strategic operation in the supply of content for vehicles, catalysed by growing demand for electric vehicles and autonomous driving.

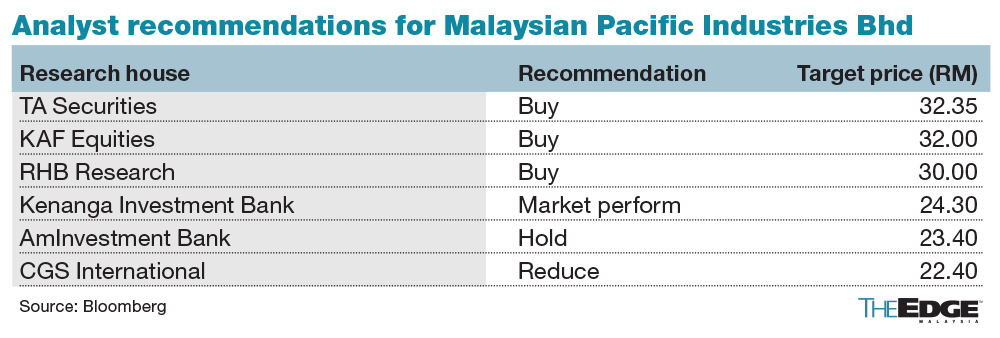

“MPI will continue to focus on expanding the automotive segment, with the target for the automotive segment to contribute over 50% of the group's revenue over the next few years,” said TA Securities, while still maintaining its earnings estimates for the financial year ending June 30, 2024 (FY2024) to FY2026.

The research house maintained its ‘buy’ recommendation on MPI, with an unchanged target price of RM32.35, based on a price-earnings multiple of 28 times the forecast calendar year 2024 earnings per share.

MPI shares closed at its intra-day high of RM28.78 on Thursday, up RM2.60 or 9.93%, after positng a 75% increase in net profit in its latest quarter. At its last close, the group had a market capitalisation of RM6.04 billion.

In a separate note, Kenanga Research said it remains optimistic about MPI's sustained recovery momentum, underpinned by its ability to rein in costs (a labour reduction at the Suzhou plant, China) and optimise supply-chain efficiency, adding that despite MPI's quarter-on-quarter improvement, its recovery momentum has not met expectations.

Acknowledging MPI’s progress in cost management and supply chain optimisation, the research house revised its FY2024 net profit forecast downward by 26%, and reduced its target price by 11% to RM24.30 (from RM27.20), maintaining its 'market perform' rating.

Despite this, the research house still likes MPI, citing its strong presence in the automotive semiconductor segment, its foray into cutting-edge technologies like gallium nitride and silicon carbide, and its expertise in power management chip packaging for data centres.

On Wednesday, MPI reported a 75% increase in net profit for the three months ended Dec 31, 2023 (2QFY2024) to RM32.15 million, thanks to lower expenses, as it also logged other operating income. Revenue for the quarter dipped 0.7% year-on-year to RM522.75 million from RM526.42 million, due to a decline in its Asian and European segments.

For the cumulative six months, MPI’s net profit fell 31.48% to RM48.67 million, from RM71.03 million for the same period a year ago. Revenue for the period fell 5% to RM1.04 billion, from RM1.09 billion a year earlier.Read also:

Malaysian Pacific Industries 2Q net profit surges 75% as other income helps