This article first appeared in Capital, The Edge Malaysia Weekly on January 15, 2024 - January 21, 2024

AS the big-cap stocks in several industries such as construction, property, utilities and renewable energy (RE) draw interest, a number of counters in the FBM Small Cap Index on Bursa Malaysia have also come on the radar of analysts and fund managers for their mid- to long-term prospects.

On a steady ascent since last July, the FBM Small Cap Index hit a two-year high of 17,078.03 points last Monday, just as the benchmark FBM KLCI continued its recent bullish streak since entering the new year to end at 1,498.93 points the next day. Buying activities were centred on banking, telecommunication and consumer stocks, and profit-taking on utility stocks.

The small-cap index rose 724.65 points, or 4.43%, as the barometer index increased by 45.73 points over the five days.

“Generally, we take small caps and mid caps as proxies for growth or value plays. As the market is anticipating a series of rate cuts in the near future, I expect the upward trend to continue. To some extent, it might [even] overshadow last year’s performance,” Areca Capital CEO Danny Wong tells The Edge.

His positive outlook on the small-cap index is shared by the majority of fund managers and analysts.

TA Investment Management Bhd chief investment officer Choo Swee Kee explains that since small-cap stocks typically see higher double-digit earnings growth compared to the usual single-digit earnings growth of big-cap FBM KLCI stocks, local investors are generally more attracted to the cheaper small caps.

In addition to expecting the FBM KLCI to surpass last year’s performance, Choo believes that selected small caps will continue to outshine big caps.

One impetus would be the launch of the National Energy Transition Roadmap (NETR), which has excited both industry players and market watchers since it was announced last August.

Some analysts say the NETR could lead to a new economic catalyst as they expect a clear policy layout on the energy transition under the road map to drive a sector re-rating on improved growth and environmental, social and corporate governance profile.

Towards this end, MIDF Amanah Investment Bank Bhd head of research Imran Yassin Md Yusof reiterates that he is watching for key beneficiaries in the asset ownership space from both RE capacity expansion and investments in grid upgrade, as well as the RE engineering, procurement, construction and commissioning (EPCC) sub-sector for the massive expansion in order book that it would mean for the players.

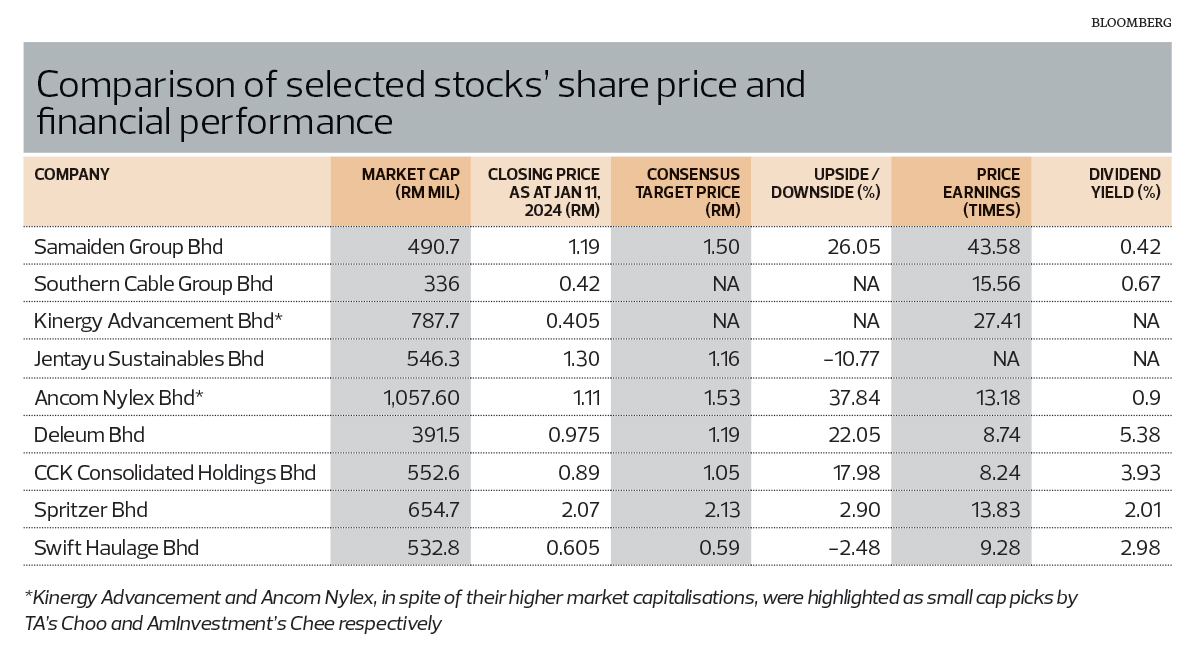

Imran reiterates his “buy” call on RE outfit Samaiden Group Bhd with a target price of RM1.54, having earlier highlighted the counter as his research house’s main stock pick for 2024.

Amid rising demand for cables on the back of Putrajaya’s RE initiatives, Malacca Securities Sdn Bhd head of research Loui Low suggests that Southern Cable Group Bhd could be well positioned in areas such as EPCC and electric grids.

“As it stands, Southern Cable has a strong order book value of circa RM900 million as at the third quarter of 2023. Based on the value, we believe it should sustain the group’s earnings for at least one to two years,” forecasts Low, who puts resistance for the counter — currently trading at around 42 sen — at 45 sen to 46 sen.

Likewise, the government’s emphasis on energy transition also has TA’s Choo suggesting an earnings upside for Kinergy Advancement Bhd (KAB) and Jentayu Sustainables Bhd, both of which are coming off a low base and likely to exhibit strong growth in that respect in the near future.

KAB, which posted full-year net profits within the range of RM2.9 million to RM5.3 million from FY2020 to FY2022, registered RM26.14 million in cumulative net profit for the three quarters ended Sept 30, 2023 (FY2023) on the back of RM136.5 million in revenue. KAB attributed the boost to the increase in energy tariffs, new revenue streams as well as the gain from completing its acquisition of mini-hydropower plant PT Inpola Mitra Elektrindo in Indonesia in June 2023, which lifted the group’s bottom line.

Meanwhile, Jentayu posted a net loss of RM8.9 million in FY2021, followed by a net profit of RM29.1 million in FY2022, before sinking into a net loss of RM5 million the following year. For the first quarter of the financial year ending June 30, 2024, the company registered a net loss of RM7.1 million on the back of RM7.6 million in revenue, following a profit after tax of RM11.39 million in the same quarter last year due to a gain on disposal of investment property of RM16.22 million in 1QFY2023.

TA’s Choo cautions that small caps have certain drawbacks even though their prospects may be good.

“Although the small-cap index will continue to outperform the FBM KLCI given small-cap stocks’ stronger earnings growth potential, any change in market sentiment due to global factors could affect the performance of small-cap companies as they are generally less liquid compared with big-cap stocks, and their earnings disappointment could also negatively affect share price performances.”

AmInvestment Research analyst Chee Kok Siang expects the trade diversion by multinational corporations from China to continue to benefit agrichemicals player Ancom Nylex Bhd, which also gains from the shift in demand from expensive patented herbicides to cheaper generic versions amid an expected global economic slowdown.

“Other factors going for the company include the commercialisation of two of its Product T within these two months as well as the better oil trajectory since late June last year. This should also support the higher product price for the industrial chemicals segment,” explains Chee, who has a “buy” call and fair value of RM1.44 for the stock.

Companies that have commanded the attention of analysts for the strong pickup in their order books include Deleum Bhd, which has core businesses in power and machinery, oilfield services and integrated corrosion solution (ICS).

“Pending the next management briefing in February, Deleum had earlier shared that the group obtained RM107 million worth of solid control job wins, bringing its outstanding order book for oilfield services [alone] to RM189 million as at Sept 30, 2023,” says AmInvestment Research analyst Muhammad Nuur Ashman, who maintains his “buy” call on the stock and raised the fair value from RM1.22 to RM1.27.

He notes that the group is also experiencing a recovery in its loss-making ICS operations against the backdrop of a stronger tender environment.

He says Deleum earlier guided for order book wins to improve significantly by 1QFY2024 as Petroliam Nasional Bhd, which is its major client, had begun to issue tenders for maintenance, construction and modification works, which could be worth up to RM8 billion.

Net cash, low gearing companies

Although broad expectations are that interest rates in the US will decline this year, the environment of elevated inflation is expected to persist. Under these circumstances, Malacca Securities’ Low believes that investors will opt for companies with net cash, low gearing and a stable dividend track record, and points to consumer stock CCK Consolidated Holdings Bhd as one that checks all the boxes.

He points out that the removal of the price ceiling for chicken amid healthy supply and demand factors — thereby normalising profits for poultry producers — is seen to benefit CCK Group, which is involved in the processing of poultry, seafood and prawns. It is also involved in the trading and retailing of cold storage goods, livestock farming and the provision of transport services and veterinary supplies.

The group’s net income trend shows consistent growth, with 3QFY2023 net profit rising 19.3% q-o-q to RM19.9 million from RM16.76 million, with a stronger retail segment and lower raw material costs.

Low also foresees CCK’s retail segment strengthening in its fourth quarter ending March 31, on the back of higher demand during the festive period.

Similarly, another consumer counter expected to thrive on robust demand is bottled water maker Spritzer Bhd, which has strong earnings prospects with the continuous arrival of international tourists as well as stabilisation of resin cost.

AmInvestment Research’s Tan Jia Hui, who has a “buy” call on the stock, maintains a positive outlook on Spritzer’s prospects. The company saw an increased average selling price of 5% to 10% in FY2023, with a stable increase of 10% in volume and stable net margin of 7% to 8% annually. It also benefits from lower raw material costs, namely plastic resins; robust domestic travel, especially during the festive seasons; and the arrival of international tourists with the easing of travel restrictions, she says, adding that Malaysia Airports Holdings Bhd had reported a passenger throughput increase of 38% y-o-y to 116 million in 2023.

Where robust expansion plans are concerned, container haulage and land transport giant Swift Haulage Bhd completed the expansion of its warehousing capacity and acquired three parcels of industrial land totalling 21,700 sq m in Butterworth, Penang, worth RM30.15 million, last November.

Malacca Securities’ Low sees promise in Swift’s current ranking as the top haulier in Peninsular Malaysia, with the largest market share since its establishment in 2011, as well as the group’s ongoing efforts to go green such as providing green logistics services. The range of resistance for the stock is pegged at 65 sen to 66 sen.

Save by subscribing to us for your print and/or digital copy.

P/S: The Edge is also available on Apple's App Store and Android's Google Play.